August didn’t turn out to be the standout month that many EV manufacturers had hoped for,Sales in August dropped by approximately 25.05% compared to July, largely due to the middle-month effect caused by the Electric Mobility Promotion Scheme 2024 (EMPS), which runs from July 1 to September 30, 2024.

I think math is bit different here.

3KW battery consumes 3 units. So let’s consider Rs10/unit. So to charge battery, it takes Rs30. And range is around 100. So per kilometer cost is just Rs 30 paisa.

Let’s consider 40 paisa for margin of safety.

Where as Petrol scooter gives mileage of around 45. So per km cost is around 2.25.

Battery life is told to be 70000km. But if we consider 60000 to be on conservative side then to run 60k, EV will incur Rs 24000. While Petrol scooter will incur 135000.

So effective saving is 135000-24000=111000

This does not include maintenence cost which is more for petrol scooter.

So clearly you can purchase either new vehicle or just replace battery and continue.

Very nicely put.

One of the main reason EVs are not pushed in India and rest of the world, is due to dependence on China for battery and their control over Lithium mines.

I think this would be a market wide hit.

There will be a big battery revelation. This big new battery compound will solve many issues(obv, bringing with it a new set of challenges).

But the only question is when will this revelation happen. Will it already be too late. Or will it be after the whole 1st gen of all EV gets to become useless.

Only time will tell.

Luckily I’m not in the market for any 2 wheeler.

I don’t think it’s an accurate statement that EVs are not being pushed in India or globally. India has a very ambitious target for EV as you can see from below article.

Same goes for the rest of the world. People often ignore hybrids that also run on battery so we need to combine both EV and hybrid to get a true picture of their growth trajctory. See the article below.

The biggest challenge for EV adoption in India would be charging infrastructure and technology itself. Once they slowly gets resolved, adoption will improve.

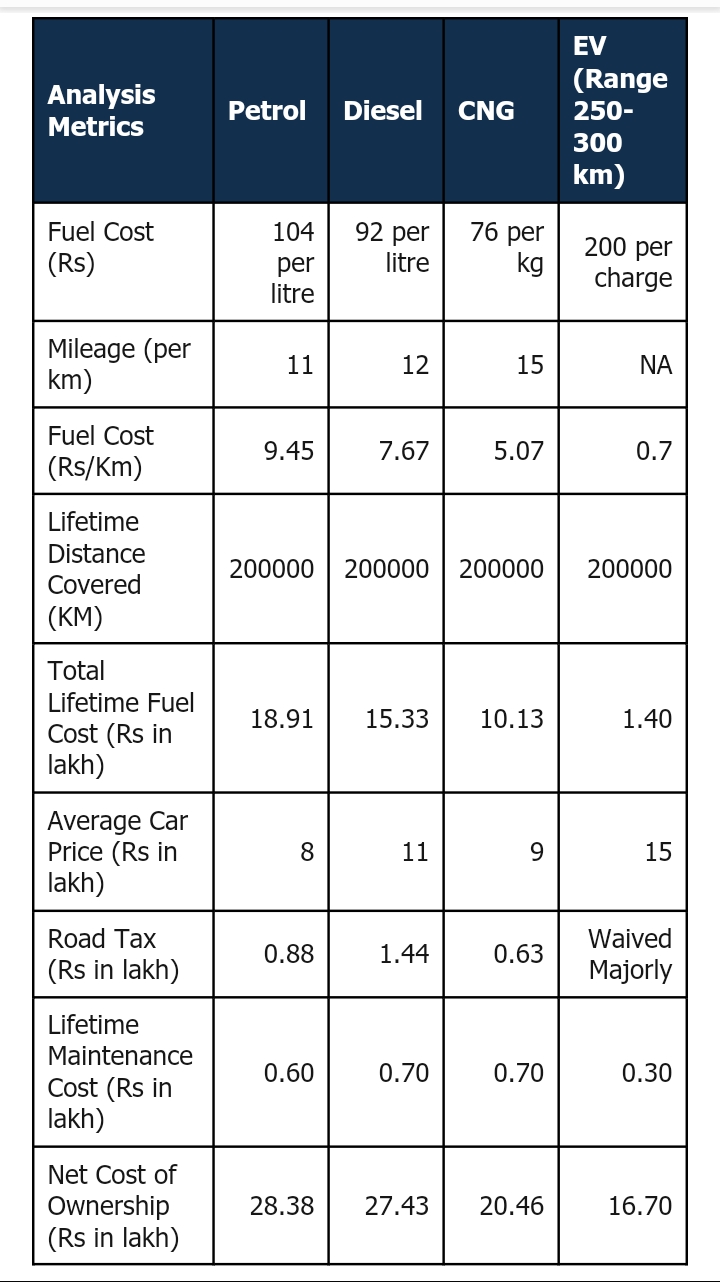

Total Vehicle Cost Analysis

[1711106202_Alternative Fuel

Source Care edge report dated 22march 2024 link below

1711106202_Alternative Fuel Vehicles_CareEdge Ratings.pdf (317.1 KB)

Currently On one side, we have Union Heavy Industries Minister H.D. Kumaraswamy saying that FAME III is on the way. He recently mentioned that the government could finalize the third phase of the FAME scheme in the next month or two. An inter-ministerial group is apparently working on it, addressing issues from the earlier phases.

On the other side, we have Union Road Transport Minister Nitin Gadkari, who suggests that EV subsidies might be coming to an end. He believes that with increasing demand and production, costs are dropping, which could reduce the need for government support.

Gadkari also highlighted that the GST on electric vehicles is just 5%, compared to 28% for petrol and diesel vehicles, which he sees as a major advantage for EVs.

It seems like there’s an ongoing debate about the future of India’s EV policy. While Kumaraswamy’s comments suggest that government support is still needed, Gadkari believes the industry is ready to stand on its own.

This uncertainty is causing some worry in the EV industry, especially with the festive season around the corner. October is a huge month for vehicle sales in India, with Navratri and Diwali both taking place. EV manufacturers are concerned that if EMPS ends and FAME III isn’t ready, there might be a gap in subsidies.

Some industry players are calling for either an extension of EMPS or a quick rollout of FAME III to keep the momentum going.

However, Gadkari remains optimistic. He’s confident that India can become a global hub for EV manufacturing, with support from initiatives like the Production Linked Incentive (PLI) scheme, which aims to boost local production.

The government’s next move will be crucial in shaping the industry’s future.

Also, common man should factor in higher GST on EV going forward.

Once No. of EV cars sold out per quarter starts going up, there is high possibility that, all current concessions such as Low GST, Low Road Tax would be removed or rationalized to higher levels.

By the time, most of us are willing to buy EV car, most of these tax waivers would have been reduced, so actual practical calculations would be quite different.

Having said this, it is clear that, even after higher taxes, EV would be better and less costly option in the long term, provided basic charging infrastructure is in place and Electricity charges are not hiked by the Authorities.

There is tendency in certain nations to increase taxes on those things which start becoming popular, so one must factor such things in all future calculations !!!

Not sure if the lifetime maintenance cost shown here depicts reality. It could be much higher. Also, is the cost of battery replacement considered? apologies, I havent read the report.

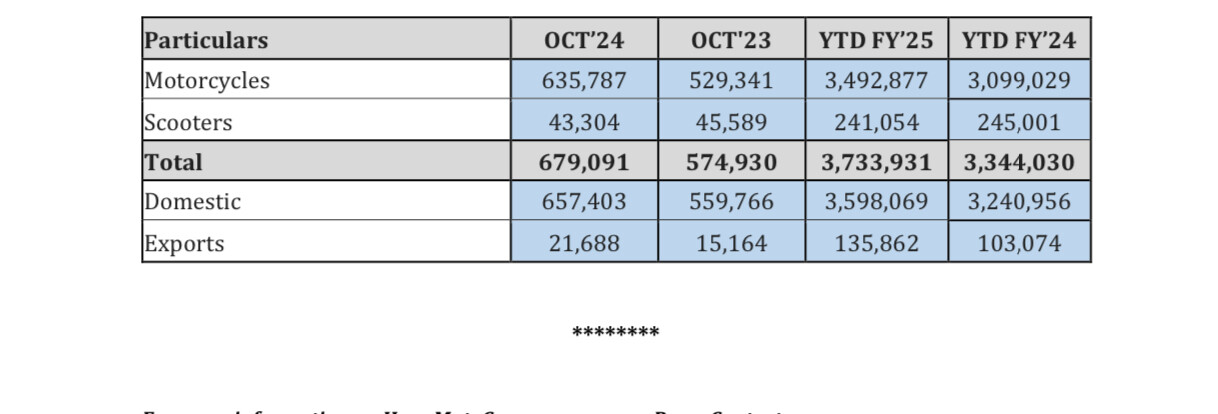

Good month for Hero and all the other 2-wheelers OEMs (Bajaj, TVS etc), all of them beating street estimates by a big margin.

We are still not in festive season yet, so hard to say if this performance is one off or a harbinger of structural boom in 2-wheeler sales in the country.

To me article is like comparing driving while drunk or using mobile and arguing which is a better option ![]()

Automobile to start with is a cyclical industry. And then there are established and very strong players like Bajaj, TVS and Hero with their eyes and pockets firmly set on EV space. Each one of these companies have track record of building world class quality businesses gaining and sustaining market dominance. And for that reason I fail to envision a scenario where start ups like Ola or Ather will be able to do well and make money for their investors.

Hero owns 40 pc stake in Ather Electric. That’s a key positive. In all probability, they are likely to take it up beyond 50 pc. That’s one ( Clearly - they ll end up having deep pockets with Hero’s parentage )

Secondly - Ather - has a far better product perception vs Ola which is currently undergoing a very rough patch wrt piling customer complaints and product breakdowns. Till last year, Ola looked like a clear winner. The tables have now started to turn. Ather docent face these issues

Bajaj Chetak sells around 22-23k EVs / month. They said that they ll start to break even ( at EBITDA levels ) when they start to sell > 25k / month

Ather is currently doing about 12-13k EVs / month

Ola used to do > 40k EVs / month which have now fallen to around 25 k EVs / month due increased customer complaints and bad publicity thereof

Just wanted to highlight these points - not that I recommend or I intend to apply for the IPO

No mention about EV scooters share.

Last Year Festive period was split between October and November, this year it is all in October except for Gujarati New Year (dispatch for which would have happened in October anyway).

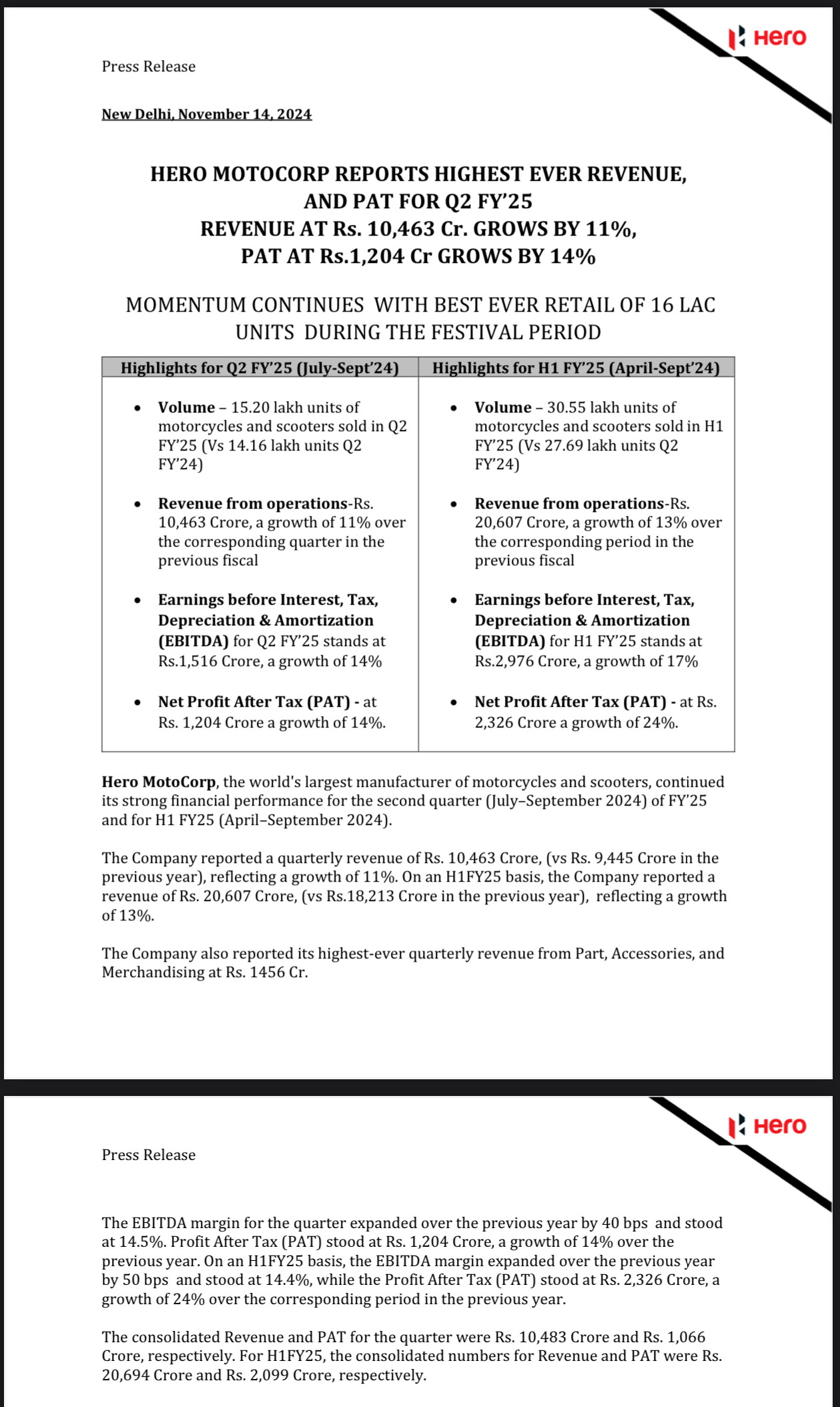

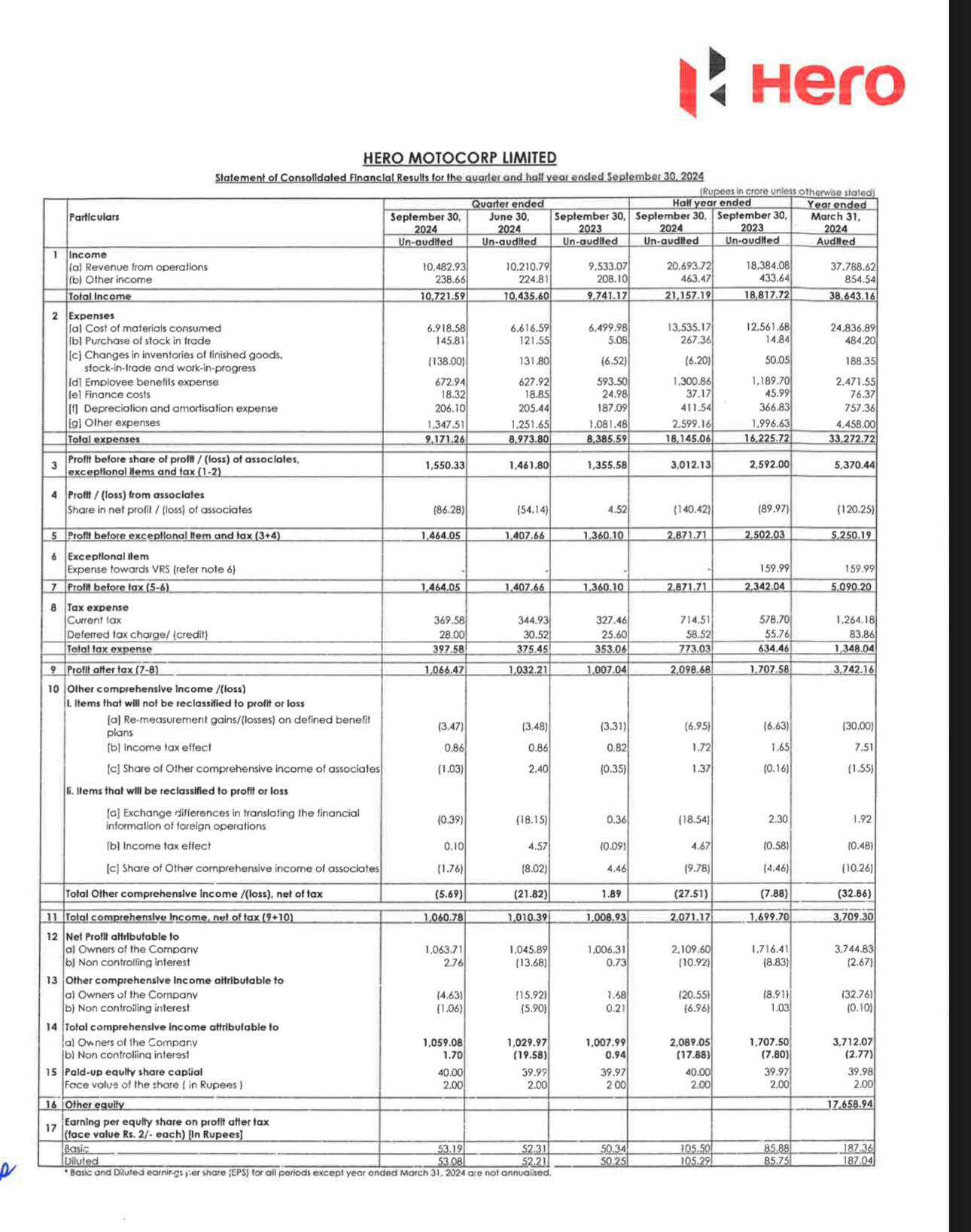

Hero MotoCorp Q2 FY25 RESULTS AND Earnings Call Key Takeaways

Results Source

- Financial Performance

• Record Revenue:

Hero MotoCorp achieved its highest-ever quarterly revenue of Rs. 10,463 crores, an 11% YoY increase. For H1 FY25, revenue totaled Rs. 20,607 crores, a 13% YoY growth.

• Profitability Metrics:

EBITDA grew 14% YoY to Rs. 1,516 crores, with margins improving by 40 basis points to 14.5%. PAT rose 14% YoY to Rs. 1,204 crores in Q2 and 24% YoY in H1 to Rs. 2,326 crores.

• Parts & Accessories Revenue:

A record Rs. 1,456 crores in revenue from the parts, accessories, and merchandise business, marking a 7.5% YoY growth.

• Cash Flow:

Cash from operations in H1 FY25 jumped 160% YoY to Rs. 2,817 crores, showcasing Hero’s strong financial position.

- Operational Performance

• Festival Sales Record:

During the festive period, Hero sold 1.6 million units, leading to a 16% revenue growth over 32 days. Market share in Vahan improved to 31.6% during this period.

• EV Growth:

EV volumes doubled to 5,000 units/month during Q2 and surged to 11,600 units in the festive season. Hero gained a 20% market share in five cities and 10% in ten cities for EVs.

• Premium Segment Focus:

58 Hero Premia stores are operational, targeting 100+ stores by FY25-end. Hero plans to expand its premium product portfolio to solidify its position.

• Global Expansion:

The global business grew by 30% YoY in H1 FY25, supported by new market entries, including the Philippines.

- Future Outlook

• Premium and ICE Scooters:

Hero will launch three premium motorcycles (Xpulse 210, Xtreme 250R, Karizma XMR 250) and three new ICE scooters by March 2025.

• VIDA EV Expansion:

Plans to expand its VIDA electric scooter lineup to cater to various price segments and achieve cost leadership.

• Optimism for Growth:

Hero expects continued growth driven by rural market participation, new product launches, and strong consumer demand.

• Hedging for Delinquency:

Measures are underway to address rising delinquencies in financing and improve collections.

- Key Highlights

• Rural Demand:

Rural markets significantly contributed to sales, with a higher share of inquiries than in previous years.

• Brand Building:

Increased investment in brand awareness campaigns and scaling accessories and merchandising to boost profitability.

• Consumer Sentiment:

Strong buying patterns during the festive season are expected to sustain in the coming quarters.

• Long-Term Confidence:

Hero anticipates sustained growth fueled by government initiatives, favorable macroeconomic conditions, and continued rural participation.

- Concerns

• Financing Issues:

A rise in delinquencies and slower collections in H1 FY25. Hero is focused on addressing this challenge.

• Competition:

The growing competition in the EV and premium segments demands aggressive innovation and marketing.

Hero MotoCorp’s consistent performance, strong market presence, and strategic focus on growth sectors position it well for future expansion in both domestic and international markets.

Disc :- invested

Hero Moto -

Q2 FY 25 results and concall highlights -

Revenues - 10483 vs 9533 cr

EBITDA - 1450 vs 1360 cr ( margins @ 14 vs 14 pc )

PAT - 1066 vs 1007 cr

Company will invest aggressively behind the ICE - scooters, Premium ICE bikes and Electric scooters

Sales from parts and Merchandise @ 1453 cr, up 7 pc in Q2 - highest ever

EBITDA margins for the ICE business was @ 16.5 pc

Company was able to sell an avg of 5k EV scooters/month in Q2. In the festive season they sold 11.6k EV scooters ( VIDA )

Company sold 16 lakh bikes in the Festive season ( of 32 days ) with a revenue growth of 13 pc YoY. The Upswing in sales came from both Urban and Rural geographies ( both grew in double digits - rural more than urban )

Strong festive sales have enabled the company to greatly reduce its inventories

Company is starting to see demand coming back from the bottom of pyramid segment. They believe - as the results of strong Govt Capex show up, the demand from this bottom of pyramid segment should grow strongly

No of bikes sold in the festive season via financing route was @ 66 pc. Around 17 pc were sold though company’s captive financing arm - Hero Fincorp ( these figures are in line with last year’s data )

Company has crossed 500 Hero 2.0 stores ( these are upgraded versions of their existing stores. Company has decided to upgrade a fixed no of its erstwhile stores to 2.0 standards ). These are upgraded stores giving a better customer experience

Have also crossed 40 Premia stores - should take them to 100 stores before end of FY 25. Premia stores have been opened to sell premium vehicles like - Harley X440, Harley Maverick, Karizma XMR, X Pulse 200 and Vida EVs

Company is seeing greater traction for their EVs and premium bikes in areas where they have set up their Premia and Hero 2.0 stores

Company’s 125 cc brands - Super Splendor, Xtreme, Glamour continue to do well

Within next 6 months - company will aggressively expand its product portfolio in the EV-scooters mkt. Have lined up multiple launches in this space

The Premia dealerships are doing brisk business. It’s the company’s existing dealers that are opening these Premia stores. Premia and Hero 2.0 stores are a great help for the company while selling their Premium and EV products

Company’s exports grew at a healthy 30 pc in H1. Countries like Mexico and Columbia did really well

Company sold 30k bikes to institutional buyers like - Zomato, Swiggy etc in the festive season

Xtreme 125 has been a huge success in both the Urban and Rural mkts. Its production is now up @ 40k units / month

Disc: holding, contrarian bet, biased, not SEBI registered, not a buy/sell recommendation