Didn’t see rating upgrade news shared earlier in thread, good to see them in good books of rating agencies backed by performance.

Serious money is made when operating performance and rerating( mkt perception on future outlook)both goes hand in hand. While performance with high teen sales CAGR and operating margin expansion is visible, mkt participation may follow soon.

Valuation are lower compared to peers group esp in light of high return ratios, low downside risk here, and mkt generally takes its own time to reward new listings.( Experience being invested in another chemical company Jubilant ingrevia is that there was lot of selling after demerger by fund houses as well as concerns around environmental damages etc - at the end mkt rewarded it well) - Narrative changes with price ![]()

Q1 concall issue was raised on payment default in past - Mr Shetty did explain circumstances and closure status - good enough for now, can keep a watch on any patterns

- Again As an Investor our effort is well spent on Heranba performance and Corp governance and here are some positive as we can see

- Promoter skin in game - 74% holdings post IPO

- Ratings upgrade by Crisil

- Quality of quarterly performance reporting and con calls

- Future Capex through internal accruals

- Efficient capital allocation as of now - guided for 250 Cr Capex with 3.5 type asset turnover in Q1 22 concall

- Additional capacities to come online in next few quarters for Brownfield in technicals

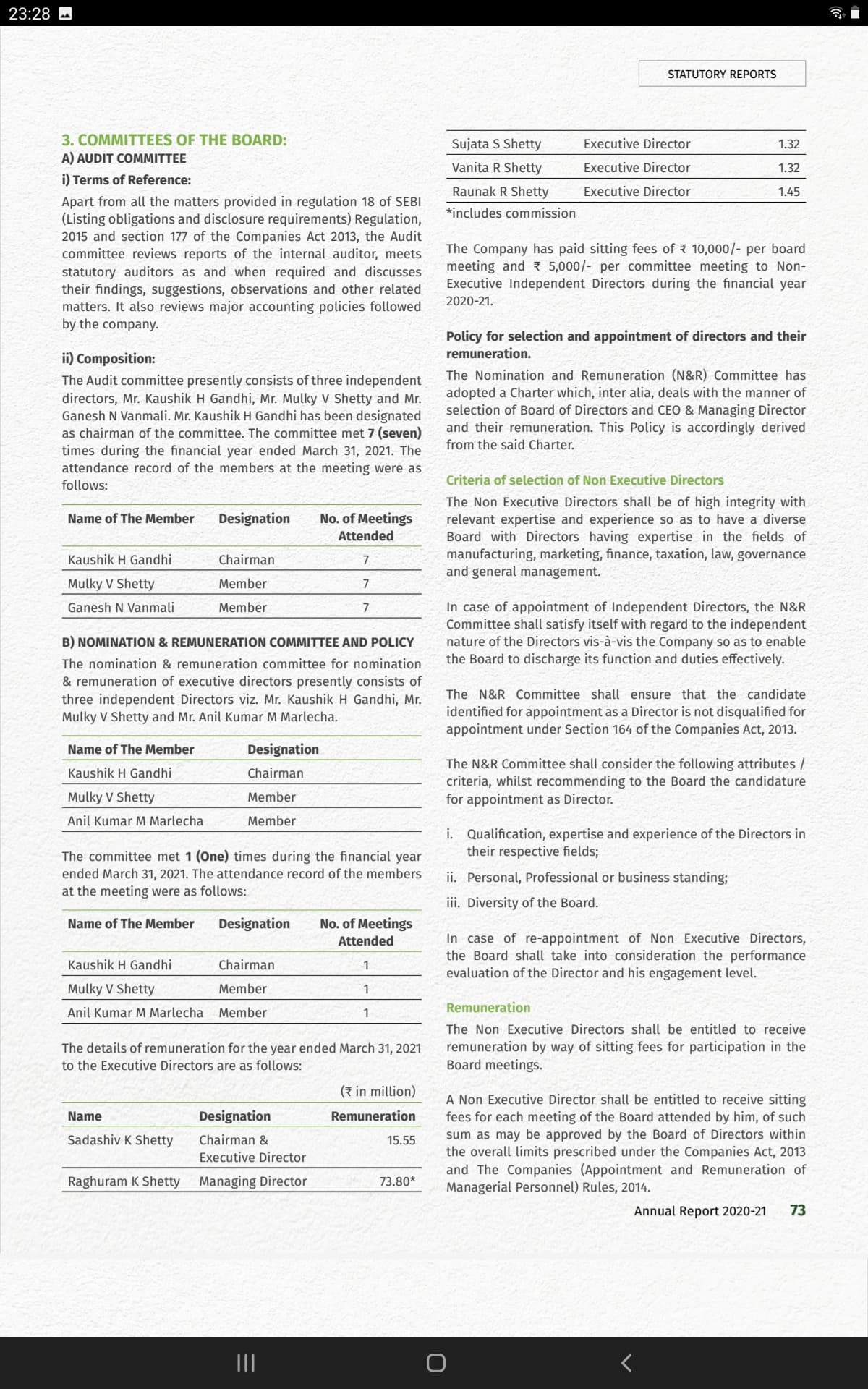

- Promoter remuneration is quite conservative - details below

Annual report is a good read to get a better sense about company performance and outlook

Some highlights from AR

Steady and consistent performance - esp margin profile trajectory

Reputable customer base

**Industry tail winds as their future is linked with Agchem and pyrethoroids - they are dominant player with 20% mkt share in India for pyrethoroids- mgmt discussions has good details on outlook and growth - esp realization call out which will improve going forward volume vs value **

- Above seems to be corroborated with recent quarterly performance where inspite of higher domestic share in mix, margins have done well and go higher as export normalization

Promoter remuneration seems quite conservative and well in line with performance for MD

Valuations

- FY22 they are likely to close at 1500 cr + revenue, 200 cr+ profit and 19% margins - this is not considering new brownfield capacities coming online in Q4 type. Current market cap is 3100 cr.

- Once new Capex of 250 cr ( all from internal accruals) comes online we are looking at 2500 cr rev, 20% margins( new products at higher margins and increasing export mix), it can do profits around 325-350 crs - looking at its peers trading at 3.5X TO 8X sales and 25 to 50 PE ( Sumitomo, Bharat rasayan, Dhanuka etc).

There is sizable rerating potential even at lower band of segment valuations it can have market cap in range of 8000 cr+ over next 2 years from current 3100 cr., RoCE and RoIC for Hernaba is segment leading

*Technically on charts, likely to be stronger once it takes out listing price in 900+ region

Disc : Invested after Q4 results