Hi all. Very new ( just 4 months into the market) please have a look at my novice portfolio (would like to hold till 2020) gathered from reading and watching expert interviews. Im not good at reading financials of the company. It has become highly diversified now, but most of the companies here are growing companies and dont know which to let go. I have 100 shares of all the stocks listed below. I would like to streamline my portfolio. Please give me an insight to which to sell about 5-8 stocks

(please dont tell me sell all, i would be heart broken).

Defence

Astra microwave (130)

Pipavav Defense (72)

Zen Technologies (88)

Transport

Ashok leyland (95)

Tata Motors DVR (257)

Industry

Balaji Amines (133)

Kanoria chemical (70)

Sudarshan chemical (95)

Elgi equipments (125)

Greenply Ind (182)

Ruchira papers (59)

Jain Irrigation (65)

Ujaas energy (26)

Auto ancillary

Gabriel India (92)

Greaves Cotton (124)

Jamna Auto (145)

Skipper Ltd (160)

Talbros Auto (104)

Infra

Axiscades (250)

Jindal steel (60)

Jyoti structure (16)

Logistics

Snowman Logistics (90)

TCI (240)

Realty

Ashiana (150)

DLF (98)

Anantraj (36)

Im looking into these stocks from reading a lot into Valuepickr. But dont have so much money to deploy. Can you suggest the best 3-5 companies to invest from the below keeping in mind the current market situation (to buy after selling a few from above).

Atul Auto

Amrutanjan Health

SSWL

Mayur Uniq

JB Chem

KSCL

Plastiblends

Tube Investment of India

Harita Seat

Somany ceramics

Reliance Infra

Ipca Lab

Need serious help… much appreciated and would like to thank this forum for their great work!

Sharing my observation- nothing personal here. Nor you should treat this as stock buy/sell recommendation.

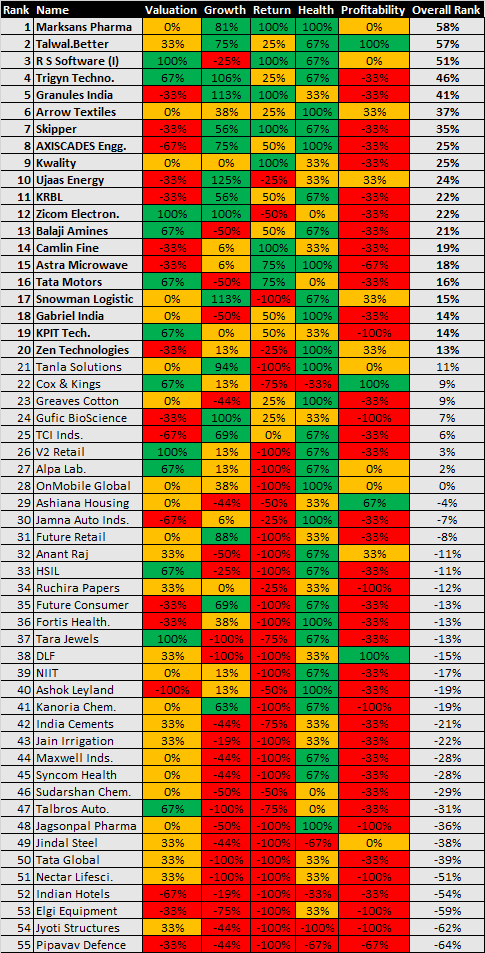

Too many stocks with trading bet approach & not value investing. What is your objective. you said you want to hold till 2020, are you confidant all these will survive or do well in next 5 years. Suggest first screen the stocks basis various parameters like PE, PB, Sales & profit growth, return & profitability, operating margins. Select few who have great past history. Out of that select few whom you think will do great in next 5-10 years. Extensively read VP threads, do some financial number crunching- you may get basic knowledge from internet.

My 2cents :

i) If you are new to investing in equity, first please consider educating yourself by reading a few books on investing like : i) One up on wall street - Peter Lynch, ii) Intelligent Investor - Benjamin Graham, iii) The Warren Buffett Portfolio: Mastering the Power of the Focus Investment Strategy - Robert G. Hagstrom iv) Thoughtful Investor - Basant Maheshwari (helpful in getting an Indian context to investing).

ii) When you are new to investing, you do not want to trouble yourself by collecting a bunch of 55 companies stocks, Why not invest the same in a diversified top performing one or two Equity mutual funds instead ?

ii) Its not necessary to bet on every sector or upcoming company to make money. After all, not every company in your portfolio will all go up together. Over a period of time you will find some going up, some down and some may stay where they are. In the process, you are bound to lose sleep and effort, keeping a tab on their price movements rather than focusing on what the underlying companies & their managements are doing in their business.

iii) Portfolio allocation: As has been often repeated by our senior members here, if your intention is to create wealth for yourself, please consider allocating your capital (money) to a focus group of not more than 10-12 stocks. For an average investor, since the amount of time and money at one’s disposal is limited, any allocation less than 5-8% of the total portfolio is not going to be worth it.

iv) Although it may be heart-breaking, it may be well worth your time and effort to bring down the number from 55 to say, 8-12. Consider allocating serious capital (say, 12-15%) to your top conviction bets spread across 2-3 sectors and allocate less to those lower in the category. Think of money lost in this exercise of portfolio restructuring/rebuilding as ‘tuition fee’ and take it off your mind. All the very best.

Are you still positive about Marksans Pharma? Issues- a) Pending UKMHRA observations. b) failing growth (Dec 16 Q net profit is half of Dec 15 Q). c) Fy 15 net profit 109.4 C, eps 2.64, Expected net profit Fy 16 110-115 C, eps 2.6-2.7. d) current correction more than 55% from high of 115.

Background- US FDA gave clearance in Sep15, UKMHRA review in Nov 15 with some observations. On 18 th Dec 2015 company replied about observations, so far no reply. Management says issues are routine & not serious, no data issue as per the management. 99% export company with major supply to UK & other European countries. Soft Gelatin Capsule making process is supposed to be their major selling point in USA. Pending several ANDAs in USA. Management expects 4-5 ANDA clearance in 2016 calender year. Severe correction after UKMHRA observation. Current Q result came post- market on 12 Feb 2106 which were very poor in spite of rupee devaluation significantly. I am new to forum & not much net savvy. Request for guidance by forum members if it is a HOLD or SELL. Average purchase price Rs.90/-. About 10% of my PF.

Bought just a 100 of each, will buy more as I get a better understanding of the market.

(Dont deal with Banks and finance companies).

Let me know, if any thoughts please.

My humble suggestion is before you form your conviction on a stock ask yourself as to how well this company is equipped to survive the economic downturn or a bad business environment (which is as inevitable as bull run that we are seeing now). By now you would already be looking at profit numbers, sales growth ROE, ROCE, valuation metrics etc to inform your stock picks. You should also pay attention to if they have the right discipline to manage cash to survive the downturn/bad business environment and if they can start generating lots of cash when the market cycle turns.

So if I were you I’d look at things like company’s debt position, working capital management, capital allocation and cash flow situation. There are several ways to do it. One is to read credit rating reports from agencies such Crisil or Care. These reports describe a company’s working capital practices (inventory, cash conversion cycles etc) over the last few years. These reports also mention the company’s lenders. If the lenders are likes of Kotak’s or HDFC’s then I will worry less as these bankers are extremely good at underwriting and they do a very good due diligence on a company’s business before giving them loan. However if company’s bankers consist of 2nd grade PSU banks I will be careful.

Second is I will look at cash conversion metrics such as working capital management. This data is easily available on screener. I might also check company’s return on assets to get an idea whether the next plant they have built or machinery they have bought is generating enough returns.

For example Shilpa Med’s cash conversion cycle is some 270 days. Which means if they sold their goods on 1st January they won’t get see any cash before the Q4 of year. But in the meantime they need to pay salaries and bills. So to do that they will draw on debt which they will hope to repay with the profits at the end of the year. But Shilpa Med hasn’t generated any profits in the last two years which means they need to keep taking on new debt which is what you see in their balance sheet.

But more debt also means more interest payment which will impact profits. Company is also doing some heavy Capex year on year but return on asset is just not there. In the meantime, high depreciation expense, on these assets, along with high interest payment, will continue to eat into their profit margin from both the sides.

So I see a big fuse lit on this company.

Now if their management on a con-call said something like selling off their assets, pruning their debt, tightening their working capital and improving operational efficiencies, this might become an interesting stock.

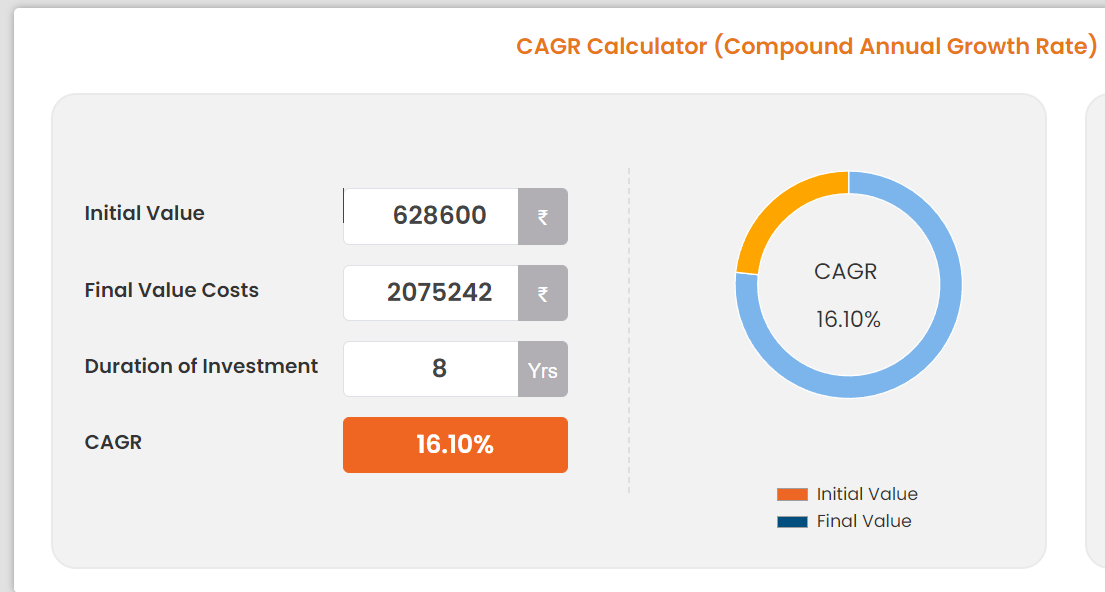

16% CAGR on such a high risk portfolio is very average return (adjusted for high risk premium associated with small/microcaps). Nifty small caps index has given 18% CAGR in 8 years and many large cap mutual funds (with much lower risk premium) have also given returns in the same range.

To generate alpha of 3-5% over a representative index (in this Nifty Small Caps), the target return will be 21-23% which is quite challenging and requires active management of portfolio. If one is not up to it better to go with good small caps mutual funds.

90% of large cap mutual funds doesn’t beat index in India. For a new person who just bought stocks based on tips of experts, I still see 16% as decent return.

Many large caps index may not beat index but on an absolute basis they are still returning 14-15% return.

You are comparing returns of highly risky and volatile small/microcaps caps that see large drawdowns against more stable and less risky large caps. You are essentially saying that you see equal risk (of losing your capital) between investing in say a 500 crore microcap company, based on tip, versus say a Titan or L&T.

If one factored in risk premium, 16% return on large caps is much better than 20% return on small caps for the same capital deployed. On the other hand, 12% return on large caps will be seen worse than returns offered by 8% in FD (zero risk).

Before you set your return target you need to determine risk premium that you are carrying in your portfolio and and then calculate opportunity cost (foregoing a better return opportunity). So if you are targeting 16% return on small caps, you incur an opportunity cost compared to Small Caps index return as well as small caps mutual funds whose returns are in the range of 18-25%.