The reason insurers were using mostly bank as sales channel because they could. Now if there is a curtailment there, they will find other ways. As such this is a hare-brained law designed by people who have never run businesses. It’s like telling Trent to not make more than 50% of their sales from their private owned brand.

I think investors are reading too much into such news. Let the next quarterly numbers come in and it will be a lot easier to determine how much impact it will cause.

I would tend to agree with this view.

How does it really matter whether it is 50% or 60% from Banks and Remaining from other channels? At the end of the day, population should buy suitable insurance products based on their own requirements.

Insurance penetration in our country is very low, and large population should be covered by insurance. It is as simple as that!!

Basically the bank is free to sell insurance (at the end of the day it is the most convenient channel), but if they only sell their own policies then it’s wrong for the others

Banks and Insurance companies need not be same, if let’s say a bank like HDFC having the biggest user base gives up all its partnerships and makes sure people will only buy HDFC Life Insurance then it’s a significant chunk of the market that HDFC controls essentially

It’s like an Anti-Competition law to prevent Banks to take advantage of their position, otherwise it’s as good as saying goodbye to non-banking insurance companies like Tata AIA, Aditya Birla Sun Life, Bajaj Allianz, Etc.

Take the US for example, the biggest banks need not be insurance providers at all

This is an interesting point. In US, banks like Chase or Citibank or any leading retail bank etc. do they have an insurance arm? If not then why? Is it because they find it less competetive as they have a restriction to sell them from their branches? Did they never launch insurance products or did at some point and wind up later?

Health insurance in India also is majorly non bank with Star, Care, Niva etc leading the market share and growth pack (just like in US with United, Cigna etc)…why is that so? Why banks are not leading the race in Health in India if there is currently no restriction to sell.

What is the major reason that in US currently none of the major retail banks have leading arm in insurance? (Pls correct me if wrong). I am sure just a law on restricting selling policies via their own bank branches would not be the major reason.

So let me understand this. HDFC Bank, being a bank, cannot sell insurance policies of only HDFC Life but Bajaj Finserve being an NBFC are allowed to sell only Bajaj Allianz policies. Where is the level playing field then?

There is a level playing field, what clientele does Bajaj Allianz have?

Is it at all comparable with the customer access that HDFC Bank has? HDFC banks operates as a bank so there are easy cross selling opportunities. HDFC Life is free to be sold via HDFC Life Branches without any other policy. HDFC Bank and HDFC Life are two different entities.

End of the day, HDFC Bank banking network will trump network of any other insurance provider with ease. That is why banassurance channel exists for the bank and is the biggest contributor for all insurance sales in India. Giving that undue advantage to banks (HDFC Bank) to sell only their subsidy (i.e. HDFC Life) makes an unfair competition between the two.

So do you think that the government will impose a limit on how many insurance policies a bank can sell? Or will be the bank just divert the business to its insurance arm and won’t sell through their channel?

HDFC bank owns HDFC life insurance and they are not doing anything wrong in promoting their own companies’ products. It’s not called taking advantage but common sense business practice.

Plus this situation doesn’t warrant anti-competition law. It will only be applicable if HDFC bank was the only one providing insurance products to everyone in India which is not the case here. Again if a retailer like Trent fully packs their stores with their own products does that call for an anti-competitive ruling? No, unless there was no option for other brands to sell their products?

Other insurance providers have their own channels including banks and if someone doesn’t want HDFC life insurance they don’t need to go to HDFC bank. Tata AIA or Bajaj Allianz have very well developed distribution network and they don’t need HDFC bank to sell their products. If they do then they can have a commercial tie-up with them like many airlines do.

I tend to agree with your thoughts but want to mention here that while the example or retail vs insurance is absolutely correct, they are not comparable because of the industry & regulatory enviornment they operate it. This is the difference of investing in a highly government regulated sector vs slightly lesser regulated, for now.

Banking operates by way of government license and hence bank owned insurance companies do have an edge by virtue of their parents licence. One might argue that non banks could also have applied for licence and used this advantage but they chose not to or were nit selected.

Whatever said, the question raised came because of misselling by bank personnals and not because of only selling. When extra penetrayion is needed, these bank channels are the answer but regulator has final lever to control what they want amd when they want. There is no law currently and balanced law is expected as it will be in dicussion with best in the industry.

Problem is misselling, as always, and somehow regulator believes that by capping the selling by own banks can reduce misseling.

Disc. Retail and Insurance both one of the too and core holdings. Although will keep

evaluating insurance as being eligible for core holding or not.

Agree with your view on misseling practices by banks but then why not have those practices in all parts of the businesses like a promoter giving wrong picture of the business to their investors, an fmcg business making false claims about their latest beauty products, AMC companies misleading the mutual fund buyers with cherry picked claims, a real estate builder not giving the amenities they promised during their marketing? (And the list goes on.)

If government was really serious about protecting so called ignorant customers who can be easily taken for a ride by some banks, they should start putting regulations in every other sector where the same so called ignorant customers buy hundreds of day to day products and services.

It’s not as if people put their life savings in insurance and one wrong decision by them will be catastrophic. I have personally been duped into buying a wrong policy by LIC agent many years ago because i didn’t do my homework. I discontinued my policy next year.

I am yet to see any government regulations against the life insurance agents. Why not issue a law against them for capping the high premium policies the direct agents can sell because all the agents have incentive to maximize sale of high premium policies regardless of whether or not they are good for their customers?

And if you ask me biggest misselling in insurance sector happens in the direct channel. In fact wherever selling is involved, there will be mis-selling. So this idea of regulating selling in a tiny sliver of an industry which in turn is a small part of our economy is just ill informed.

What prevents a bank from pushing their own subsidiary’s insurance product more than others? Namesake and for regulatory reasons they can keep others products but can push only their product as the best. How does govt check that this kind of selling is not happening?

On the prima facia, this looks bad for insurance companies with existing bank networks, but may be

If top banks like HDFC Bank, ICICI Bank, and SBI align to sell each other’s insurance products, it could completely neutralize the impact of the 50% cap. For HDFC Life, this means continued dominance through a broader network, while still complying with the regulation.

If this has been done without stating it explicitly they can maintain market dominance,(just like how Facebook, Google, Microsoft never admit they are monopolies in public)

Even if the private players raises this issue to the government and they can only cap the percentage of still it ll favour the top player’s, the market is gonna consolidate with few players

No matter what they do, in the long term

On the contrary it gives oppertunity for the long term investors to accumulate

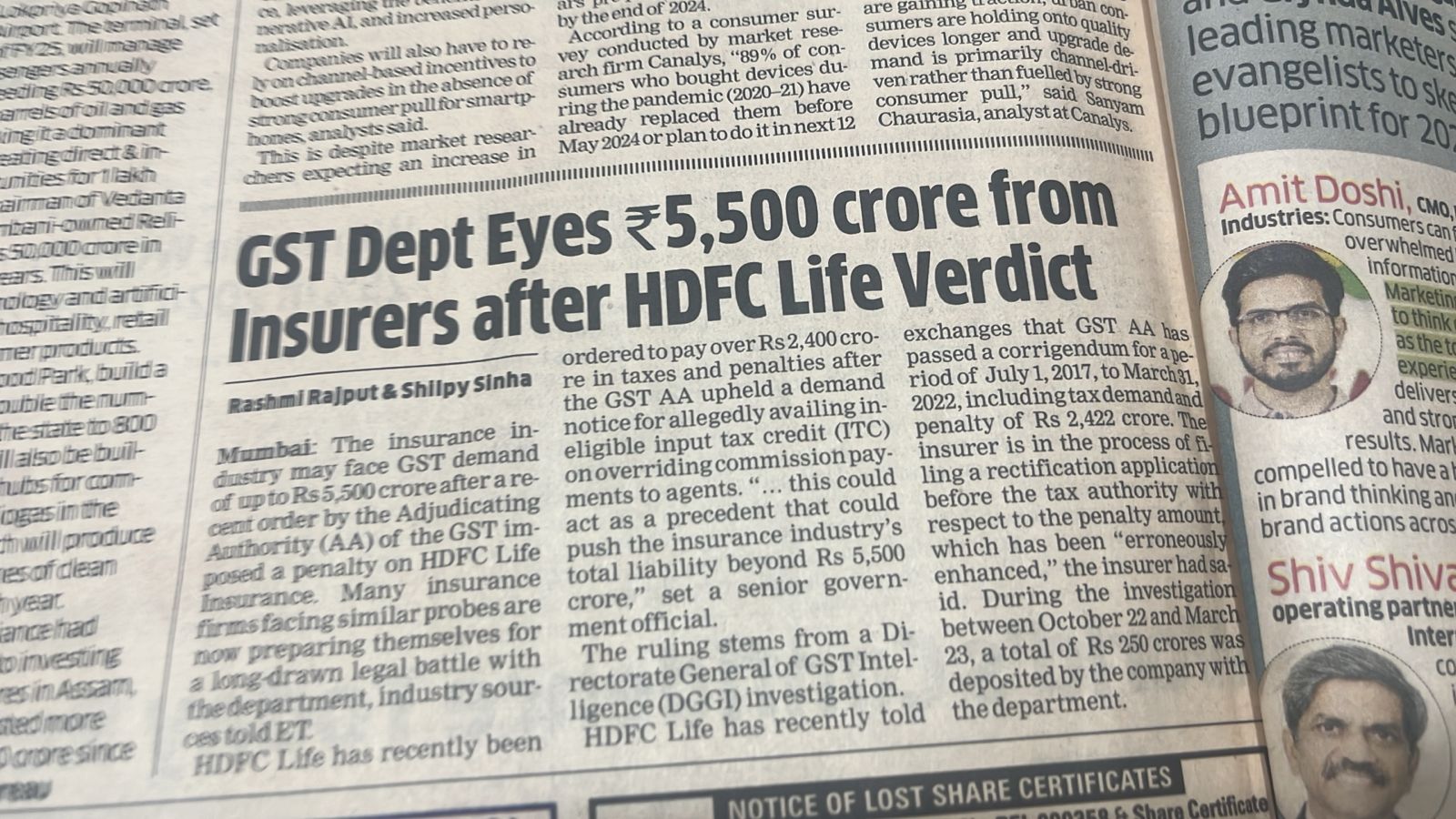

Is it really concerning? Because the investment income has come down drastically from 11910cr to 902cr which in turn is due to the 12% correction in equity markets. This has led to overall revenue going down from by 40%.

Net Premium income has still increased 10% YoY. For the 9 months of FY25, VNB and EV has grown by 14% and 18% respectively which are not bad (Not when P/EV was 5 in the past but today when P/EV=2.4)

Valuation(As of 30 Jan 2025) = 630 / 259.68 = 2.42x

It has dropped from 2.84x to 2.42x during Q2 FY25 and Q3 FY25.

If my calculations are correct, then the share price looks close to Fair Value to me or marginally undervalued.

Business seems to be performing better than FY24.

The Embedded Value grew from ₹ 30,048 crore in FY 2021-22 to ₹ 47,468 crore in FY 2023-24, reflecting a compounded annual growth rate (CAGR) of approximately 26%. As of today, it is 53,246 Crores.

Currently not holding any shares. Calculations based on latest Quarterly update.

ULIP above 2.5L were already Taxable. Now taxation has reduced to capital gain tax. Earlier this was as per personal tax slab. Basically its a rationalization.- highest marginal tax rate it was taxed on - it could have been taxed at as high as 30% rate - so it is for sure better for policyholder @ maturity - they will pay lesser tax.

^ Vibha MD hdfclife saying above too on Zee business today.