How do you find the economic moat of hdfc life in comparison with the other insurance players.

2 Likes

There were some news around tax concession received by HDFC Life on an initial demand notice. I tried to check further but could not get more details on such concession. Anyone aware of the matter?

Also, has anything changed for the business recently? Are they now allowed to sell Health insurance products?

I saw a recent launch of guaranteed benefit product. Guess something like this product came under tax net in recent budget and there was a knee jerk reaction then. Any idea on what this new guaranteed return/benefit product is?

1 Like

I have been analyzing insurance business for some time now.

I am not able to understand low ROE and ROCE for HDFC Life.

Is it due to stagnant PAT in the past few years? I can see that PAT is almost stagnated. Past 5 Year PAT growth is only 4%. This seems to have reduced ROE from 15% to 9%.

Is this a good or bad sign for the Business?

I have been holding this stock due to its high market share, but my confidence is low due to poor PAT and ROE. SBI Life has higher ROE than this.

It would help me to understand if I am missing any thing.

2 Likes

They are investing in agent network and also they acquired an Exide business return on agents is less as compared to SBI life but that doesn’t mean Hdfc’s agents are less capable it takes time before they start bringing business for the company

This is my understanding I can be wrong

1 Like

Hi, where to find metrics like return on agents, number of agents etc.

You can get from annual report, Number of agent, distribution mix , average ticket size

2 Likes

Hi Gaurav,

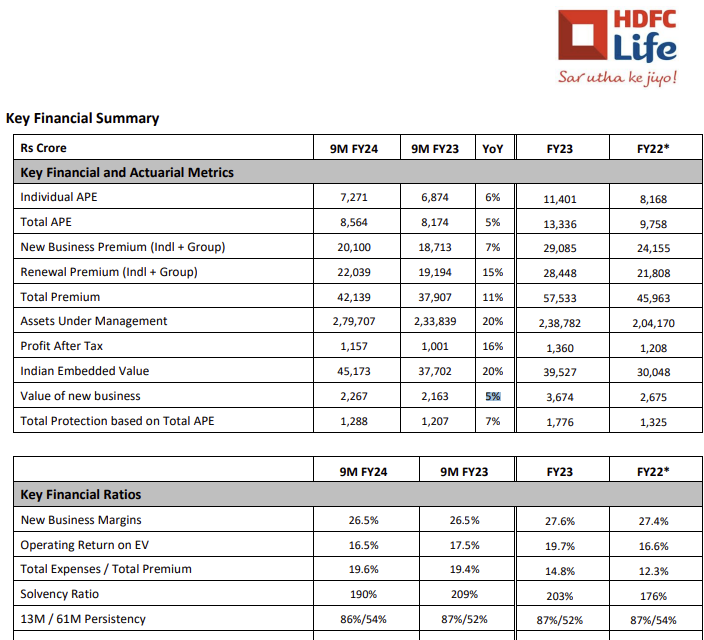

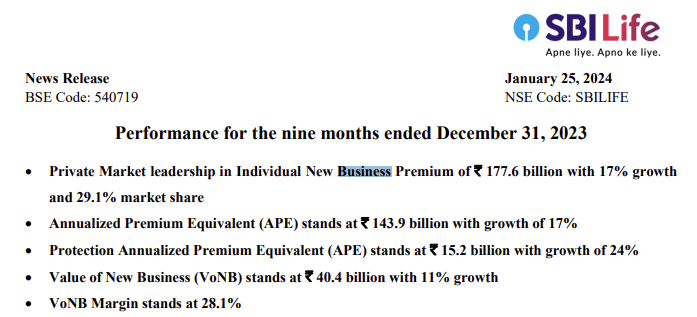

The rate of growth of VNB has further come down to 5% for HDFC Life;

while for SBI Life its at 11%

with higher VNB margin and also higher solvency ratio…

Hi Gunesh, Could you throw some light pls. ROEs and ROCEs are both 50% higher for SBI Life as compared to HDFC life

I have also mentioned the same in my post that, SBI LIFE has higher ROE than HDFC Life.

ROE/ROCE may not be right metric to look at the profitability of an life insurer given there current business phase, As PAT is lumpy due to new business strain. RoEVOP would be the right metric.

2 Likes

SBI life is definetly doing well over last few years, However hdfc life has had many challenges with hdfc bank moving to open architecture (led to loss of counter share), policy changes on high ticket non par and the merger. If you look at there growth over other channels they have very much outdone there peers.

3 Likes

I can see that, HDFC Life has reported increase in Net Profits during past 12 months as compared to previous year.

Sales have grown at 17% CAGR and Net Profits have grown at only 4% CAGR over past 5 years.

This looks like a compounding business which seems to be growing its Sales and PAT in the past 5+ years.

I am unable to understand the correction which has happened in this stock from time to time. It looks like a secular business with moderate growth but still the stock price does not reflect the same.

What could be the reasons for this stagnant stock price, with negative movements from time to time?

I am unable to fully understand the reason for this.

Disc : Invested from lower levels.

4 Likes

As per my analysis, Profit Before Tax has been trending downward in the past 4 years.

It has dropped from 1400 to 1050 Crores in the past 4-5 years.

Net Profit is also under pressure due to this.

As mentioned in this thread, they are expanding their Agents network and the revenue per agent is not yet up to the mark. So overall except growth in premiums, all other profitability parameters are under stress after acquisition of Exide Life.

It seems that, Management may need more time to show increase in profit parameters. Market may not be happy with this scenario of low or nil growth in PAT, hence Stock price is also under constant pressure.

With interest rate cuts predicted in the latter half of the year or next year, embedded value of the company should increase thus bringing valuations a little lower. That could be a trigger for price move.

1 Like

Q3 FY24 Update:

No. of shares = 215 cr (As of 31-12-2023 as per published data)

Embedded value (9MFY24) = 45,173 (growth=20% yoy)

VNB (9MFY24) = 2267 Cr

iev + vnb(9MFY24)/share = 47,440/215 = 220.65

Valuation(08/Feb/24) = 591/220.65 = 2.67x

To me, this looks undervalued as compared to its historic valuations.

I am not sure whether my calculations are correct.

This calculation is based on 9MFY24 data.

If the calculation is correct, then it looks undervalued as of now. Even if we consider 3x, then also share price should be 661.

Disc: Holding.

1 Like

After my post, stock has been declining and it seems that, it may correct further.

One of the reasons could be the changes made by Regulators during budget of 2023, but after that, I do not remember any new negative development.

I would like to know views of other Investors, as to What are those reasons for poor performance of HDFC Life in past one year?

Disc - Invested from low levels.

Here is my observation,

HDFC life products are sold by push marketing. Customer wants health,term or vehicle insurance products. But minuscule % customers buy life insurance products voluntarily.

Ample of content in social media about(against) the substandard returns from life insurance products enlightening large number of their potential customers . Aggressive push and easy use of mutual fund schemes will definitely affect the HDFC life’s product mix.

So i prefer listed general insurance company for long term rather than Life insurance companies.

Disc: Hold. Bought at lower levels.

Compared to historic, usually more than 3x, it definitely looks undervalued at this stage. But then Icici pru is trading at, i think, less than 2.5x.

Still comparitively, HDFC life is tradi g at higer multiples than Icici or Sbi.

Invested and planning to increase.

Yes, I tend to agree with your observation. I have also realized that, probably HDFC Life is more suitable for entry and exit at right prices. Whether it is a long term compounder or not is not yet clear.

One of the major reasons for less interest in life insurance is that many people in India, still view insurance as a form of saving and mostly prefer endowment plans (LIC, for instance). This trend will gradually dwindle with an increase in awareness about the importance of term insurance and disposable income. In my view, life insurance and general insurance are different products not comparable.

1 Like

Embedded value of life insurance firms should increase when the interest rates are slashed which will make valuations more reasonable.

1 Like