Disc: Zero investment. Trying my learning experience.

Request you to comment and guide my mistakes.

Its my first try here. I have very less knowledge on investment. Investment (value) experience of less than 3 years. Pardon my mistakes and huge valuations mistakes.

Part - 1: Comparing internationals top Insurance companies(MetLife, Standard Life) with Indian HDFC Life Insurance.

For some reason, some of the biggest insurance companies( MetLife and Standard Life ) have not being able to create the shareholder value in long term. Any rationale?

Warren Buffet in Geico Insurance investment: The scenario was slightly different, Warren Buffet’s Berkshire Hathaway brilliantly used the Premiums they received from Geico, which they term it as ‘Float’ and invested them for a great returns (19%) in long term. (For more details on it: Here’s How Much Money Warren Buffett Has Made in GEICO | The Motley Fool)

Valuing Insurance Stocks, value expert suggests us to look into 2 things,

- Price to Book Value: <1 - Brilliant, 1-2 - Decent bets, 3> - Overvalued.

- Equity Growth - 10% - Good, 10-15% - Great.

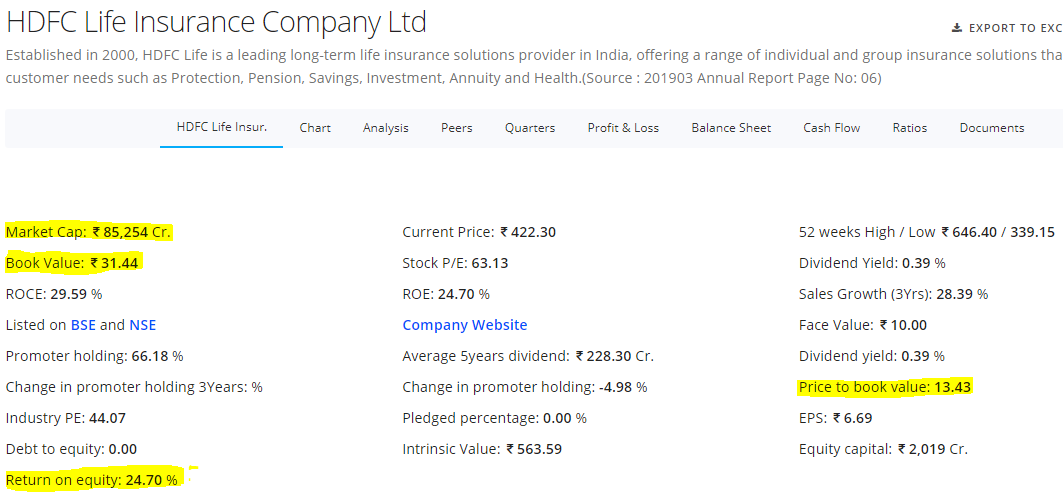

Part - 2 : HDFC Life current Valuations:

- ROE growth - 24% (Super Amazing)

- Price to Book - 13 times! ( Too expensive , good below max. 3)

- Market cap: 80,000 cr - $10 billion. ( MetLife Mk cap : $25.9 billion, x2.5 times )

- Sales: 43,247cr - $6 billion. ( MetLife Sales - $70 billion, x12 times)

Question I am trying to ask myself is: If HDFC Life reaches $70 billion(12 times) in say 15 years, will it have the $130 billion(13 times) the valuation it holds today?

Part - 3: Valuing/Comparison of the HDFC brand name. And deriving HDFCLife Future Valuation.

HDFC Bank: Book value growth.

From the above two pictures, it is exactly what I fear!

HDFC bank in its early days has enjoyed P/E of 40s (2006) and BV of 8-9 (2005). And Now the stock is able to enjoy P/E ratio of 25-30 and BV of 3-5 (Which is still very good compared to competitors)

Therefore: Valuations of HDFC Life in 15 years.

First assumption : HDFC Life is able to keep their ROE at 25% for next 15 years, Their book value will become close to Rs. 950.

Second assumption : Let’s assume it will enjoy premium price to Book value, say 4 (exceptional actually), the price of the stock would be Rs. 3800.

Result : If we are able to buy the stock at say Rs. 350. CAGR returns would be 17%.

Risks : 17% CAGR is with higher estimates of 25% ROE for 15 years and premium BV (at *4x) after 15 years!