Sometimes I think that we think too much about all this. In hindi they say Baal ki khaal nikalana…Let them give some time for synergy to play out.

10 Likes

It may not be obvious unless you are from the sector.

The Management is of course aware of this. Once the base is reset we can expect growth, but not to the extent that justifies the Premium valuation that existed in the Past. We should anticipate lower PB going forward that historical levels and treat this stock as a steady compounder.

Congratulations on your journey for holding this business for more than a decade.

How do you plan to redeploy the money if you can share some context on it please.

There are other ways to lower your CDR ,they can simply sell there loan books and raise cash and reduce CDR ratio.

This might hit eps in the short term or hamper growth but it is definitely going to imporve net intrest margins and help them reach a more comfortable CDR.

I have recently invested in hdfc bank rather than keeping money in bank fds as sooner or later intrest rates are going to fall and we might see other smallcaps or midcaps prices valuation elevate more than they already are.So hdfc seems like a decent bet to me in this overbought market getting a bank which is known to have the best quality loan book amongst it’s peer and that to at a historically low valuation is what got me intrested in the stock.

I have invested as a swing trade bet and will change it into a long term holding depending on how things play out.

2 Likes

Exactly. They say buy good businesses at reasonable valuations but when they come to reasonable valuations people are busy finding reasons why not to buy.

10 Likes

People are acting like HDFC is going to become the next Yes Bank, if you believe that it might happen then please share data and save retail investors like me.

As far as I understand, nothing is wrong with the company. Even after the bad merger or maybe due to changes in RBI guidelines, the company is still giving descent or flat results.

Disc: It’s always my top holding through MFs. I recently bought it as an individual stock, doing daily SIP for this stock. I might sell individual stock units later once this stock bounces back to do the rebalancing of the portfolio. I did the same last year and got a 7-8% gain from this stock in a few months. I believe that it’s a value buy when its PB < 3

2 Likes

Premium valuations were not just for growth. It is also for pristine asset quality and prudent lending. This factor has not changed. People have forgotten credit risk and credit costs as economy is in upswing. Once few sectors face stress people with start appreciating HDFC’s quality of asset franchise.

7 Likes

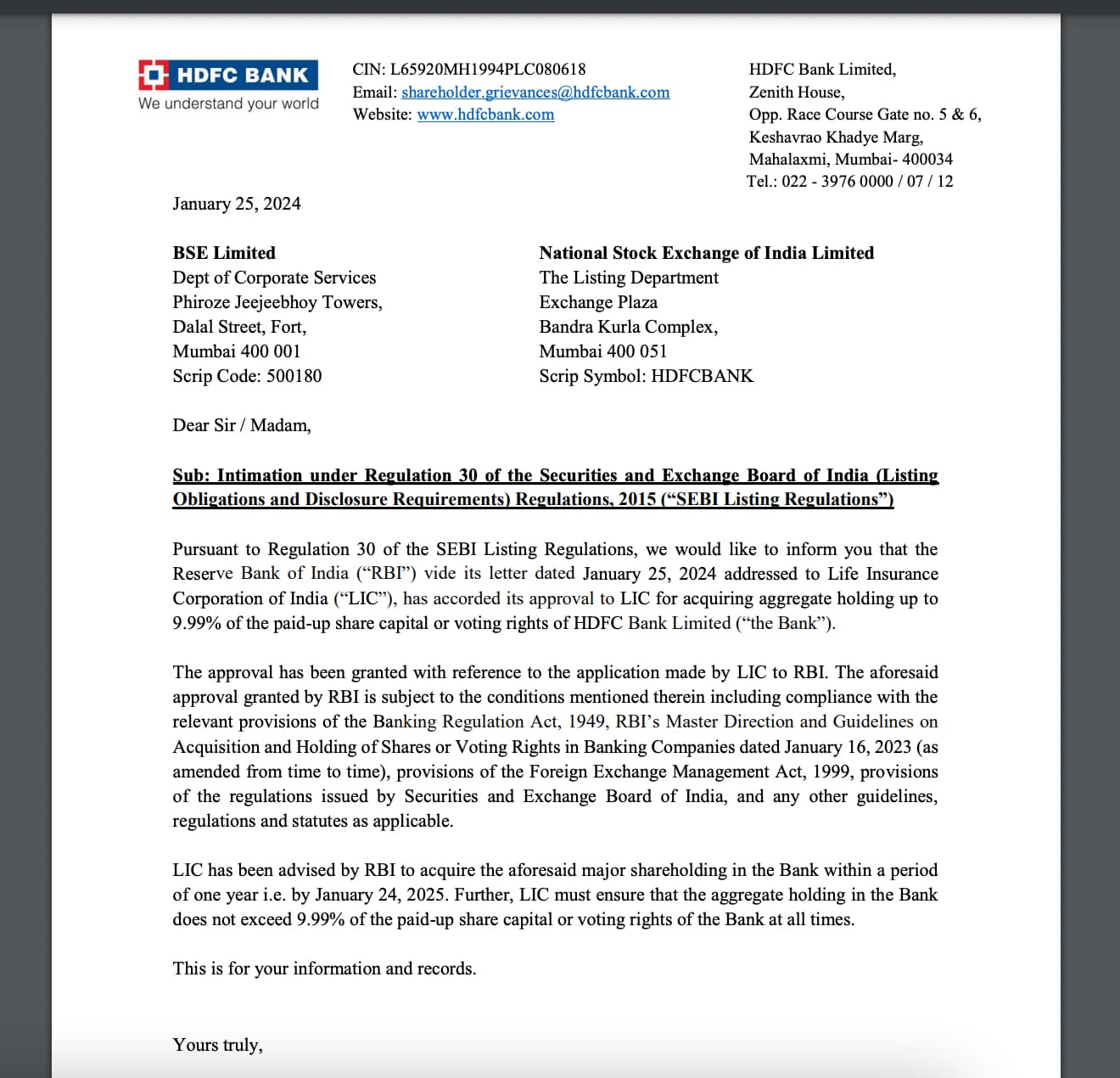

A timed move well planned by our government to support Indian markets till elections. The time horizon for LIC’s investments is beyond 5 years.

For the next 1 year, we won’t be seeing improvements in HDFC Bank financials.

2 Likes

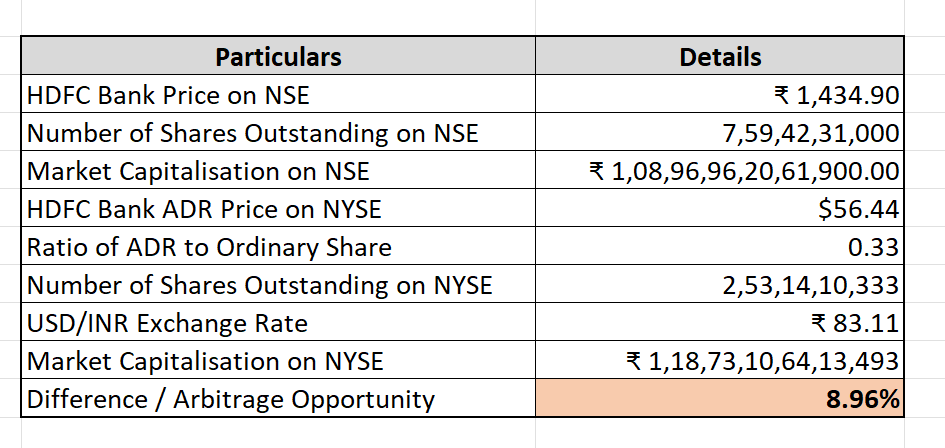

Why is it taken as a good news ? HDFC ADR is up.

Because of the above news (LIC buy)

One of the big reasons why HDFC Bank’s ADR always traded at a significant premium was because of the foreign investors limit (74% for an Indian private bank) which was are already hit.

As the large foreign fund managers (pension funds, sovereign wealth funds, municipal corporations etc) need to invest big money in a high quality franchise like HDFC Bank, the limit was acting as a big hurdle, they were never getting the required volumes and availability itself was an issue, hence the ADR always traded at 15-30% premium for HDFC Bank. The merger has obviously played a spoil sport to this and the fact that ICICI, Axis are back to good days, constant FII/FPI selling has sent HDFC Bank’s foreign investor limit well below 74%, so there is enough room for foreign investors to allocate fresh money in HDFC Bank.

As per the Dec 2023 shareholding pattern, foreign investors still have 21% legroom to get to the limit of 74% in HDFC Bank. 21% legroom left at a ~$100bn base is $20bn. So, paying up 15-30% premium for the ADR makes little sense.

For that matter, from the random google searches I did on other Indian companies, ADRs generally trade at discount for other companies

12 Likes

I assume you are seeing the shareholding pattern on screener. If that’s the case, the numbers we are seeing is for the merged entity (HDFC Bank + HDFC Ltd)

If you can go to bse/nse and see HDFC Bank’s shareholding pre 2022, you will see that the promoters of HDFC Bank: HDFC Ltd and HDFC investments Ltd held ~26% of the shares, both were marked as foreign promoters. These shares are effectively cancelled after the merger. New shareholding pattern is adjusted for this.

The foreign shareholding is 60% as of Dec’23 (against the limit of 74%) and the float is now effectively 100% since the erstwhile foreign promoter’s shares are cancelled.

There a few technical issues like fii/fpi shareholding, msci weight, crr, slr, merger costs etc that will have a weight in the near term. If they overcome these challenges (which should happen sooner given the reputation of the management), people can finally focus on what’s relevant (NIMs, ROE etc). A long term shareholder like LIC is entering HDFC Bank knowing all these challenges should be done away looking being 5+years. Ofc, the NIMs will not be in 4.3% in the future but it’ll most certainly not be 3.4% in the long term. Patient long-term investors can make decent returns given the multiples have come off sharply

2 Likes

Tell me what use is holding HDFC Bank if it is not giving out any dividends?

No dividends policy is for the company which are currently in huge growth stage and can re-invest.

HDFC Bank, TCS are matured companies, and they have no short of cash. They are in the stage where they need to return money to the shareholder through dividends and buybacks.

All the smallcaps we are investing in is speculation and hope that one day once they have 10x their earnings, then they will give us small dividend % like 2-3% which would be 20-30% for us since we bought the stock when share price was 1/10.

I see absolutely no point in owning a large matured company which does not give me dividends, as otherwise my holding is just a record in demat form.

2 Likes

A company that’s growing profit at 19% labeled as Matured, CEO claims they can add another HDFCB every 4 years. I would very much call it a growth machine.

6 Likes

If India’s GDP has to grow at 6%, add 7% to 10% real inflation on top , and then management efforts like increasing branches, its really difficult even for large banks to not grow at 15%, they have to be really lousy at their job to not be able to grow at minimum 15% for next 10 years to come. Can’t say the same about IT service based giants though with all these AI threats looming.

In Rural and Semi urabn areas, people still use to visit branch, they are not tech savvy and at the same time they do have fear of online fraud,so they don’t prefer technology.Apart from that old age people also don’t use technology to a great extent.

HDFC bank minimum balance charges and high service charges will act as a hinderance in mobilising new accounts in rural and semi urban areas…

Zero balance account and minimum service charges had impacted profitability of PSU Banks and because of which PSU Banks over a period of time have done underperformance , however now all these expenses are well adjusted in their cost structure and they are now comfortably place in terms of deposit mobilisation.

Mobilising deposit from rural areas will be challenge for HDFC Bank and may be their will be an under performacne due to additional expenses for a couple of years.

1 Like