https://www.google.com/amp/s/finance.yahoo.com/amphtml/news/edited-transcript-hdfcbank-nse-earnings-230434725.html

Transcript of concall

Some important point as per my perception

- Bank is in investment mode and not worried about few basis point deep in NIM%, sign of long-term thinking

Management says : So on the employee front, as Srini did mention, the bank on a year-on-year basis, have added about 489 branches, okay? So you would need people for that because we believe that distribution is one of our strongest point. Probably in our earlier calls, we did sort of even give an indication that we would be opening somewhere around the 600 to 700 further distribution points in our network. So that is where you will see the kind of employees getting more added. But in addition to that, let’s face it, we are not sort of diluting our technology investments or we are not removing our focus on digitizing our processes and product offerings. The fact of the matter is, despite what you do, there is still in India, there will be an ex percentage of people who would need to have – would not be as savvy digitally as you and I are. So there would be people who need to go and source, especially on the sales side, where you need a lot of investment, a lot of people to go and get business as well as an asset or a liability of the cards business. There is a finite capacity of how much each one can do. When it sort of reaches the kind of a capacity, you’ll need to add more people. So while – as Srini was mentioning, we are growing our total advances by about 19.5%. It’s not a small amount, you’re adding almost about A BANK WITHIN A BANK . So we will see people being invested in the branch banking area. We will see in the retail asset area. We will see in the agri distribution because agri is far more intensive. We will see people in this sustainable livelihood because that’s something where we are very proud of. We give back to society, it also sort of helps us in – it’s a good, great business model. So combination of all this is where we have seen a 17% growth. So you will see people moving. But as Srini was mentioning, the jaws will continue to be – the gap will be there. If the revenue is growing at 21%, we’ll try and maintain the jaws between the 17% and 18% of expenses growth. Or if the revenues were to come down, so would the cost will. So that’s kind of play we will always have, and that’s the kind of a strategy that we are going with. So I’ve explained to you on the people side. The second one is on the MARGINS where you are saying that the margins have come up from 4.3% to 4.2% from June quarter to the September quarter. That’s principally, as you also alluded to it, I think we have consciously right from the last 2 years, I’ve been focusing on mobilizing granular retail deposits. Now whether you like it or not, time deposits is necessary, especially when you have a kind of a appetite to grow on the credit side on the asset side. So this is a – we are very clear that the sales machinery will not be – we will not – we don’t want a yo-yo the – in giving directions to the huge distribution that we had to say that, okay, this quarter, you’ll focus on fixed deposits, next quarter, you don’t focus, that will sort of really destabilize kind of a sales machinery that we have created. So we are happy to have excesses. We are happy to have excess liquidity up to a certain point in time, which is what is reflected in the current margins. As Srini was mentioning, our margins would have been higher by about 15 basis points if we had sort of slowed down the deposits, but from a medium- to long-term, this is the right way to do it. So even if it sort of shaves off a bit of a margin, we are happy, and that is what it is.

2 Tax Rate and Deferred tax assets

Management: First, the deferred tax rate, right, how it is created? That’s the difference between the book profit from the tax profit. The book profits, example – one particular example we can give you is take the provisions. Provisions are made according to accounting standards and according to RBI guidelines. Tax allowance provisions in a different formula. One, it has to be fully written off, and two, there is some formula-based deductions. So they’re always – the tax allows for this credit provisions at a scale, which is lower than what the book takes. So because of that, we have to create deferred – according to the accounting standards, we have to create deferred tax asset. So that is how the tax – deferred taxes created from the books. And we have to evaluate these deferred tax on an annual basis, considering what the prevalent tax rates are and your ability to consume going forward. So to the extent that we pursue profitability and the tax rate remains stable, the deferred tax continues to be on books without any change. There will be in and out. You consume and then you put back, that goes on. In terms of this quarter, the tax rate changed. So we are up with the new tax rate from the previous tax rate of 34.7% to 25.17% – 25.2%. That would mean we have to evaluate the carrying value of the deferred tax asset and revalue to the current tax rate, right? And that impacted INR 1,650 crores we said earlier in the call, that was a onetime charge that was taken. Getting to the third aspect of the question, which is if the tax rate is 25.2%, why is the effective tax rate 32% or thereabouts? Because what happens is that you have to take this charge of INR 1,200 crores. So the tax rate year-to-date comes to 25.2%. But since you reevaluate the deferred tax and take a charge on that, that takes it to 25.2% goes to 32%. And then when you go into next quarter, you will see it is back to 25.2% because that onetime adjustment is already factored in and then it goes as this is as usual.

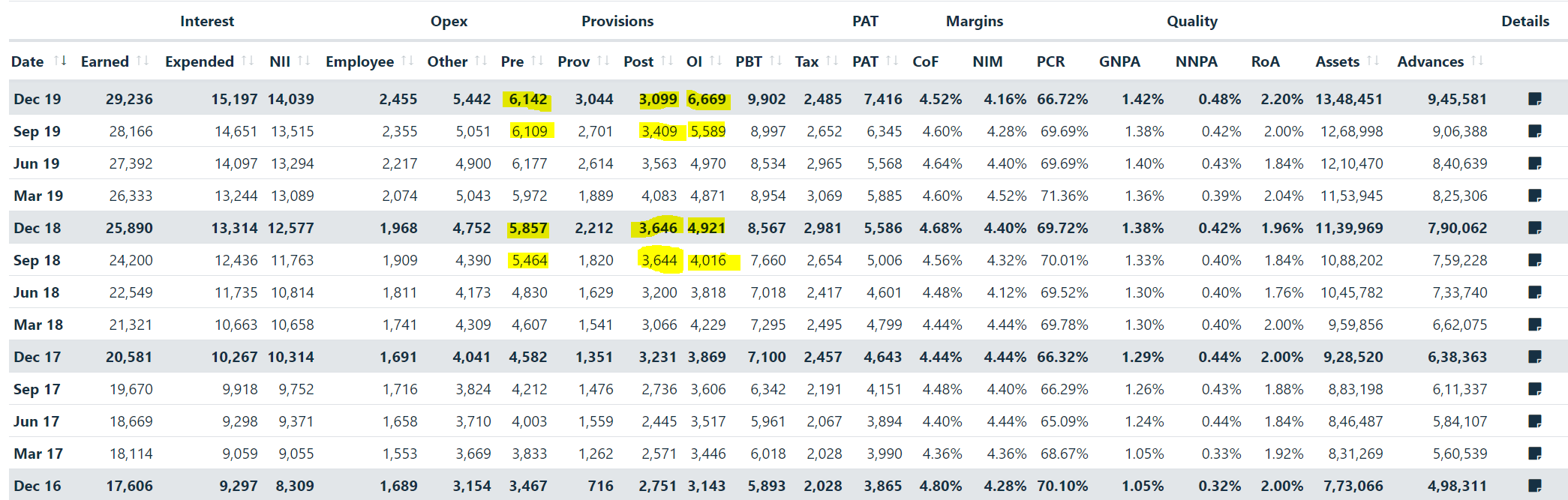

I think now as NPA are stable so worries for relative undrperfomuns don’t remain even though other banks have not declared there results

Thanks

Ashit