The market share loss momentum of HDFC Bank has continued for 10 months in a row. The largest private bank’s market share decline in September 2021 vs August 2021 was clearly seen for ICICI Bank, SBI Cards, Axis, Kotak, among others. The biggest beneficiary of HDFC Bank’s loss has been ICICI Bank followed by SBI Cards.

Disclaimer: Invested. My largest and longest position. Optimistic in LT.

I am trying to keep track of PCR ratio of HDFC bank. But unable to trace it beyond last 2 quarters. Can someone help of guide me… All I have is last 2 Quarters PCR of 71% and 68% respectively

Hi - Can anyone share insights on the below? I wasn’t able to find anything in my research.

Company has acknowledged that its investing in technology post actions taken by RBI. However, there is not a substantial increase in fixed assets excluding land and leases. i.e; category B in annual report or in the unaudited last quarter financial statements. How much is the company planning to invest, time period, where is this investment reflected in fin. stmts?

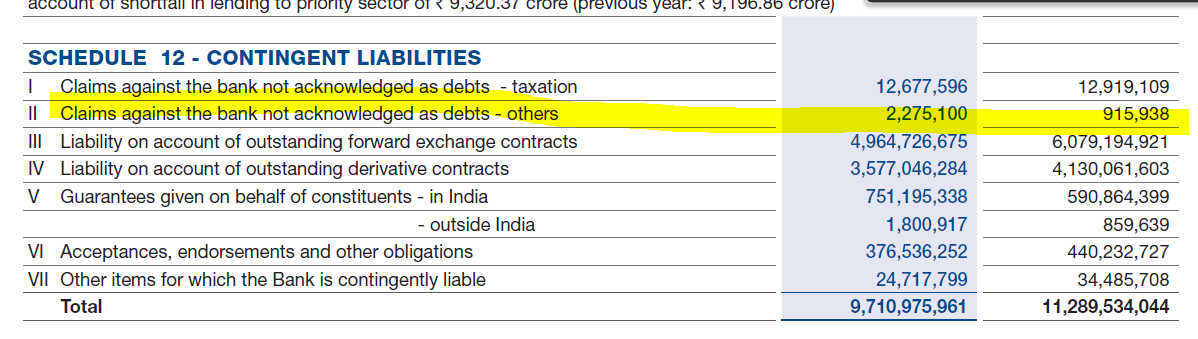

There is a significant increase in contingent liabilities. Any insights on this?

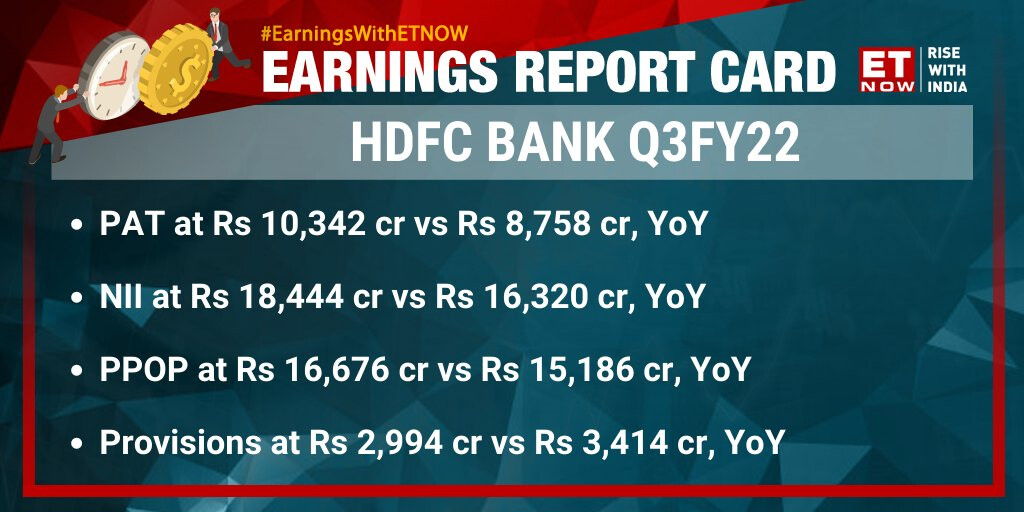

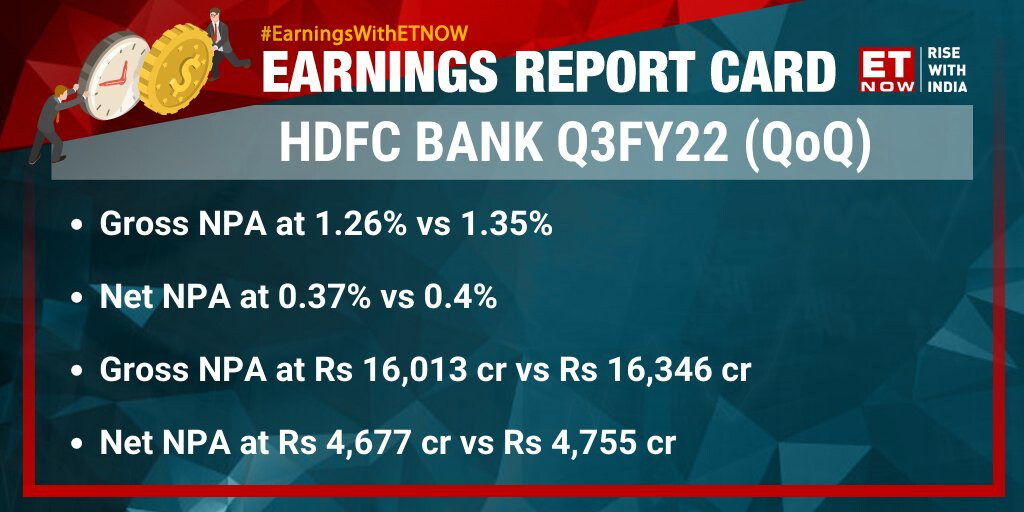

While HDFC Bank’s Gross NPA is the lowest compared to peers (1.36% or ~16K crores), its “restructured loan book” is 1.5x of that figure (while it is much lower than the Gross NPA figure for the rest of the players). Taking that into account, the Gross NPA stands at 3.47% of total loan book (same as that of Kotak Bank, still good but referred to as a “bad practice”)

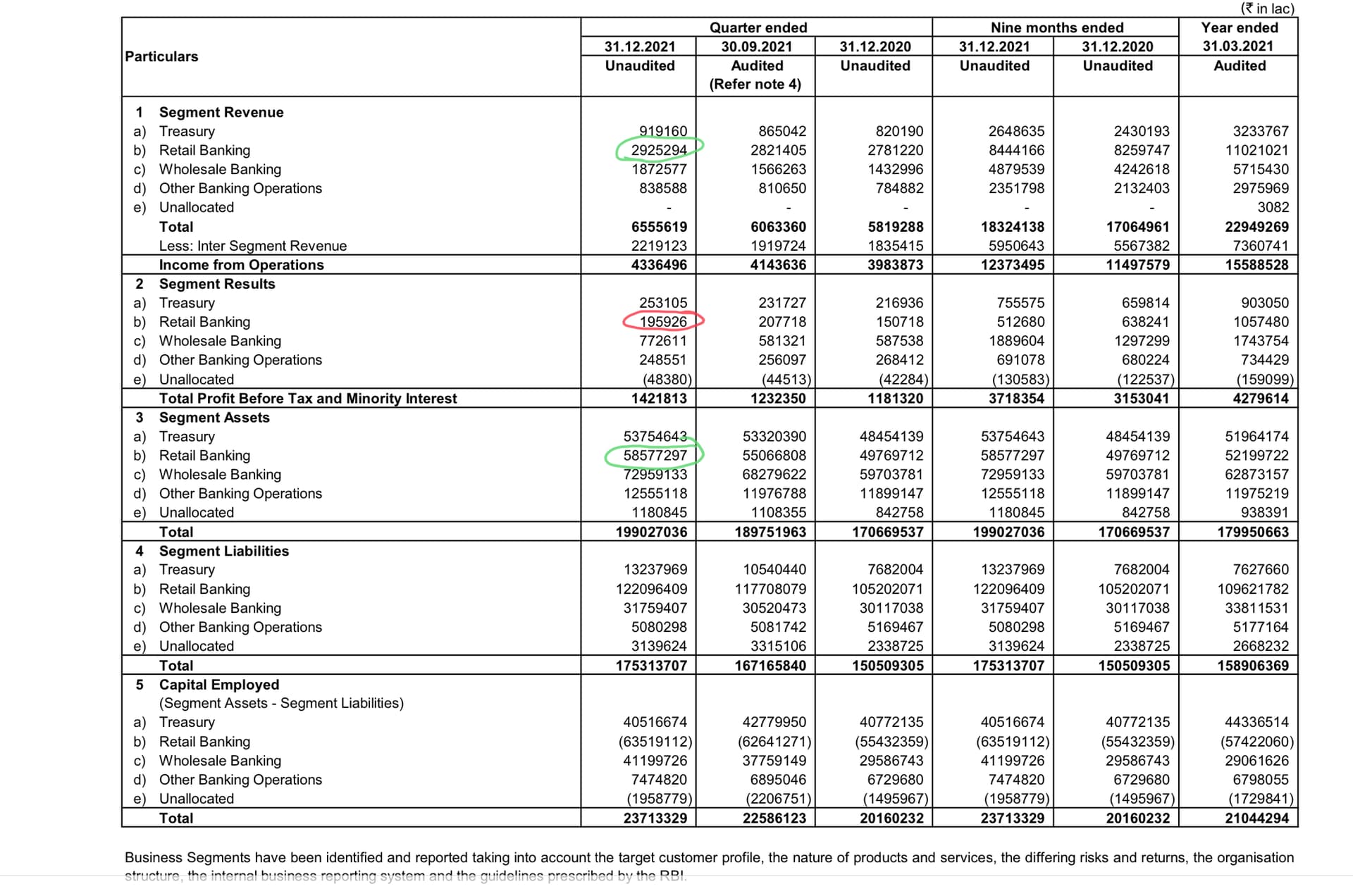

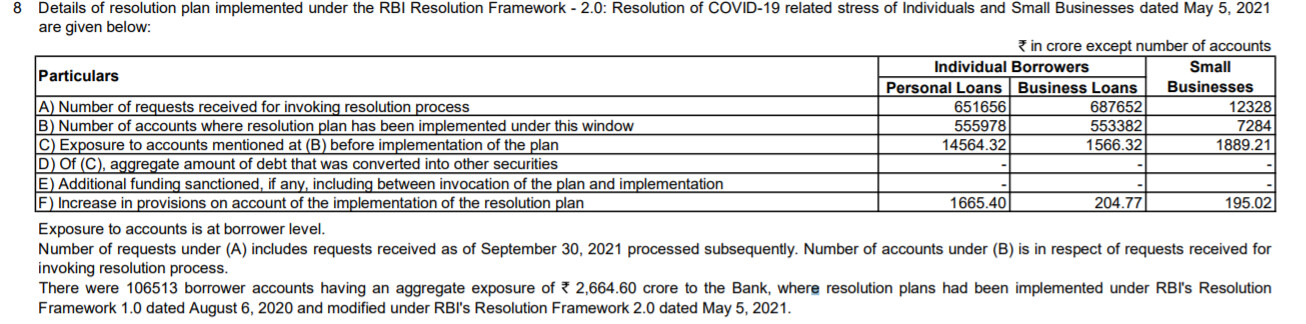

Blames HDFC Bank for purchasing HDFC’s loan book, thereby increasing the former’s retail loan book (for the past three years, HDFC Bank has purchased loans worth ~79K crores, which accounts for ~45% of the bank’s retail loan growth over the past 14 quarters)

Other things including (but not limited to) extorting processing fees from customers and questioning the practices of Junior bankers at the firm who try to hide defaults by offering top-up loans to default borrowers

From Resolution plan it can be seen that personal loan of Rs. 14564 Cr. are restructured and provisions are made approx. 1665 Cr. This amount should be watched for potential NPA/ recovery.

Disclosure: Invested from lower level and no transaction in last 30 days

Company has given explanation on Restructured book - 40% of the restructured book is secured loans, even in the remaining 60% two-thirds belongs to the Salaried individuals and hence less risky. They anticipate no more than 10-20 basis points (0.1-0.2%) impact on the GNPA due to this