Discussion about RBI restrictions and they will invite RBI for inspection and review

Overview of payment landscape, fintech disruption (they feel that it(fintech) will expand market place)

Discussion about RBI restrictions and they will invite RBI for inspection and review

Overview of payment landscape, fintech disruption (they feel that it(fintech) will expand market place)

Another fine imposed by RBI :

Does this site allows setting up poll? It will be interesting to see how many people think it will take longer than 3 months to fix these issues?

Looking at HDFC bank’s digital properties, corporate culture and hiring practice, I doubt they have talent on par with some of the finance/tech platforms India and globally. Their existing app design and usability indicate they are lagging behind in fundamental areas. On their recent conference call they seemed to indicate that all 3 failure happened due to different reasons and that somehow make it less systematic.

IT projects are notorious for delays with some 70-80% taking twice the time than estimated or at least getting delayed.

All these are noise. HDFC bank digital Platform was always not good as ICICI. Inspite of that market gave hefty valuations owing to book quality. Just because AP left, these things are getting magnified and confirmation bias.

Important metric is NIM, cost of funds and NPA. These are best ratios for hdfc bank till now. Digital etc. are supplementary.

Why SBI is cheap and should remain so and why HDFC is a league above in terms of finances.

PSU lenders dole out most loans to street vendors, pvt banks play safe

https://timesofindia.indiatimes.com/business/india-business/bad-debt-fear-keeps-private-banks-away-from-street-vendor-loans/articleshow/79961345.cms?utm_campaign=andapp&utm_medium=referral&utm_source=native_share_tray

Download the TOI app now:

https://timesofindia.onelink.me/mjFd/toisupershare

Its a truth whose reality is very ugly. Almost all the big giants go for loans to PSU banks because they fully well know the amounts they require to be sanctioned would never be allowed by any private banks. Thus they reach the PSU banks and also use political connections to further get a larger amount . This results in huge NPA’s for PSU banks . Food for thought: How will the nation grow if these large industries didn’t get such loans ?

As a lender, your concern is about getting paid back right? Is the borrower is credit worthy then the lender would be happy to lend.

So when you go to a bank and ask for a loan, the bank is not giving you credit. You already have credit (i.e. you are credit worthy) the bank just gives you the loan.

If you lend money to someone who is not credit worthy you lose money. If you lend someone more than their creditworthiness, you lose money because they won’t be able to pay back.

So the question of nation growing without the large companies not being able to get large loans deserves more thought.

Globally the interest rates are close to 0. So if a large Indian company which is creditworthy can borrow from a foreign lender(cheaper too)

I was paraphrasing Henry Hazlitt above regarding credit. Here is the original

“There is a strange idea abroad, held by all monetary cranks, that credit is something a banker gives to a man. Credit, on the contrary, is something a man already has. He has it, perhaps, because he already has marketable assets of a greater cash value than the loan for which he is asking. Or he has it because his character and past record have earned it. He brings it into the bank with him. That is why the banker makes him the loan. The banker is not giving something for nothing.”

Indeed, but then there would we exchange rate risks and also I suppose some limits and government regulations for both the borrower country and the lending country?

As if that was not true then all leading corporates would never borrow from Indian banks.

Moreover, the sustainable growth of banks would be on retail borrowings and for retail borrowers, the option of foreign borrowings is not there.

“Credit line” is something a man already has, Banks make it into actual “Credit” and the true worthiness of both the Bank and the man would finally depend on the rates at which the man gets it Vs the rate of returns he can generate out of it. The quantum of Credit being another variable. (Man can be an individual or even a corporate)

Nation growing would certainly depend on the ability of Banks to service the Credit Line of borrowers and ability of borrowers to sustain their credit lines - both are equally important for the Nation.

This is behind a paywall.

Can someone with access summarise?

Merger can create/enhance opportunities for HDFC Bank to cross-sell and increase capital efficiency

Lot of synergies and blah blah

Profitability might come down but also a chance to increase foreign holding

Combined Loan book - ₹15 lakh crore and an asset base of ₹21.5 lakh crore

HDFCs cost of funds is 7.2% while it’s 5% for HDFC Bank. So, borrowing cost will come down. Volatility of bond market wouldn’t exist anymore since HDFC Bank sources 90% of its funding from casa and term deposits

Similarly the loan mix would also be “diversified” as priority sector lending is leading to lower yields for HDFC

Note - MC has done some random additions and have provided narratives to support each math

That seems rather generic. No unique insights.

A good chunk of HDFC’s value comes from holdings in other HDFC companies (Bank, AMC, General Insurance, Life Insurance)

Furthermore, HDFC Bank could spinoff the NBFC (HDB Financial Services) and Investment Bank (HDFC Securities)

These are all well-run entities with own mature managements, spinoffs of all these entities into different listed companies would be of very attractive long term benefit to shareholders. So the dissolution of the holding company structure entirely.

Of course, there are intra-group agreements that need to be sorted, for instance using the HDFC brand name etc.

HDB financial gross NPA at almost 6% without the Supreme Court order being in place for NPAs.

Any particular area where their NBFC is facing stress?

Apologies if I missed it in the above discussion.

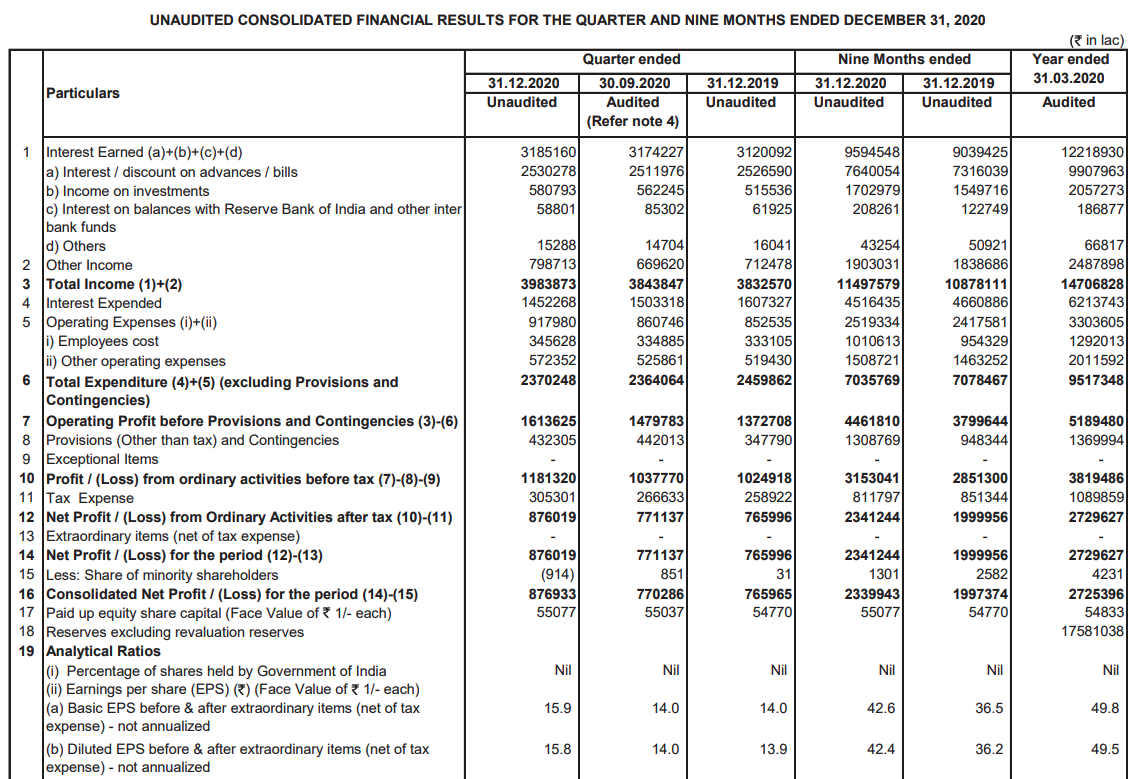

HDFC Bank Q3 highlights -

Net Interest Income at 16,317 cr vs 14,172 cr- up 15.1 pc

Other Income at 7443 cr vs 6669 cr - up 12 pc

Other income as a percentage of total income ( NII + Other income ) at 31.3 pc !!!

Components of other income -

Fees and commissions - 4974 cr

Forex and Derivatives revenues - 562 cr

Gain on sale / Revaluation of Investments -

1109 cr

Misc Income and recoveries - 797 cr

Total Expenses - 8574 cr - up 8.6 pc

Cost to Income ratio at 36.1 pc vs 37.9 pc

Total Provisions at 3414 cr ( includes 2400 cr of proforma provisions made against potential NPAs where the Supreme Court directed that accounts not declared NPAs till 31 Aug will not be declared NPAs till further orders ) vs 3043 cr in Dec 19 Qtr

PAT at 8758 cr - up 18.1 pc

Total Deposits - 1271124 cr, up 19.1 pc

CASA deposits up 29.6 pc !!!

Time deposits up 12.2 pc

CASA ratio - 43 pc

Total advances at 1082324 cr , up 15.4 pc

Domestic retail loans growth - 5.2 pc

Domestic wholesale loans grew - 25.5 pc

Retail : Wholesale loans ratio at 48 : 52

Gross NPAs - 0.81 pc

Net NPAs - 0.09 pc

Restructuring under RBI resolution framework for COVID -19 framework - 0.5 pc of loans

Disc : Holding