Excellent information.

Extrapolating it to a year, what we get as PAT/AAUM% is…

Hdfc amc and icici at 0.43

SBI at 0.24

And this will be a small proportion of TER.

TER is regulated (reduced) with increase in AUM for a fund.

So a fund house has to increase the AAUM so much that the reduced TER doesn’t hurt the PAT.

In a grand scheme of things the PAT looks wafer thin. Is AMC really a good business to invest in? And not to forget it could be cyclical.

Do we have the avg TER info too? This can give more info about the fund houses product mix.

The margins may look thin for AMC business but still very good absolute numbers and their cost structure need not proportionately increase with the rise in AUM. And look at the quantum of free cash they generate with no debt or capex.

The industry AUM is expected to grow to much higher numbers and I feel the management fees won’t come down drastically from here. Navneet Munot was also mentioning in a con-call that the expense ratios for ETFs in western countries have bottomed and may start inching up. So the sector is good but have to watch out for individual company performance.

In my calculation from my earlier post, I have already extrapolated the PAT/AAUM% for full year. So it will remain around 0.32% for HDFC & ICICI and 0.18% for SBI for FY22

The below article compares the mkt cap to AUM % among the listed AMCs.

Hdfc - 14

Nippon - 10

Absl - 7

Uti - 6

It also makes a note that

Higher the share of equity assets, better are the profits of an AMC as higher fees can be charged on equity schemes. At the same time, AMCs are required to charge lower fees on ETFs.

SBI MFs AUM has grown a lot due to fund performance or better sales/marketing team or EPFO money inflow?

EPFO money is supposed to be invested 85% in debt and the rest in equity ETF both carries very less management fees and hence low profit margin. From the above low PAT figures it looks like AUM growth is fuelled by EPFO flow than the other reasons.

So asset mix is more mportant for profitability than the absolute AUM and it’s growth.

Some stock that may look very good now but can turn so bad and grusum business very soon.

I personally have seen Navi and what they are doing it can be very lethal in my opinion and also zerodha amc licence also a big worry.

But I recently read this article and this can be the time when tech will make these old school amc be looking like old age.

This article state that cred might just buy Smallcase and if you understand there cross-sell and high net worth client reach as most people that have cred are most quite well off and have good disposable income and come in around top 1% that are major clients of amc and the bigger target overall.

Just see all three they have few things in common

Great backing and very knowledgeable top management

Huge cash burn possibilities

Tech background and more tech friendly nature.

This is all long term headwinds in my opinion as if we look at last two zerodha and cred there distribution and marketting cost could just be next to nothing if we just take there amc and also how tech friendly they are it might make other expend to also go down.

Personally see cred as the biggest thereat because of there own user base is actually the target audience of all amc.

Interesting piece…if true, perhaps explains the surge in NFO collections. In 2021, NFO was looking like an IPO in terms of so much interest and fund raise.

The AAUM details of all AMCs (monthly quarterly, fund wise etc) is available in AMFI website - Association of Mutual Fund companies and all AMCs update the data every month

By looking at data even i was little bit shock to see that why PAT/AAUM is so low of sbi when compared to HDFC and ICICI.

There I did some basic aum wise research like why their funds can charge more than sbi and by the observation that I got after that.

If we see just by Aum of each fund and do some basic analysis then we see that the biggest ticket size in all is liquid but when we see sbi their debt category aum is very high and major investment in hybrid or in debt categories that is traditionally have lower expense ratio.

In sbi major big aum are in their large-cap space that mostly charges less than mid and small-cap funds while in the case of hdfc there pure equity category biggest fund is their mid-cap opportunity fund while in case of sbi it is their blue-chip fund.

Also we can see that the concentration of ETF in sbi is quite high as compared to both.

If we just see by conclusion this is what most people need to worry about is the pat pressure as all these are trends in my opinion like etf concentration will increase, the equity side will be more favored toward the large-cap side and also concentration will also increase that will make them forced to decrease there aum.

Sbi is a clear case of why these are trends because when we see sbi major money is government based money only and also large money tends to favor sbi as trust is more especially in elderly people and all pension programs use sbi to manage their money and that make a clear trend how large and concentrated money may act.

Note:- the last figure might be less also due to sbi being a less efficient system when compared to the other two.

Just additional data for comparison of other AMCs with HDFC.

Multi cap fund NFO recently:

HDFC has raised 4300 crores

AXIS has raised 5000 crores

SBI has raised 7500 crores (very recent NFO concluded on Feb 28)

Just about 6 months ago, SBI raised almost 15000 crores with their Balanced Advantage fund NFO. So I was hoping them to raise a very substantial amount with multi cap. Though not as impressive, 7500 is still a good number. Perhaps SBI (parent) is pushing AMC business to get good valuation while listing.

Will the proposed merger of HDFC into HDFC bank be beneficial for HDFC AMC as the bank will become the direct promoter of AMC and hence could use their distribution network further to improve their share of AUM contribution? Hdfc Bank contribution to AMC business is currently at 5%. But that can grow much higher thereby increasing overall AUM. Would be interesting to see contribution from SBI & ICICI on their respective AMCs

Supply Side

From concalls, I gather that competition in Indian Asset Management space is intense which puts pressure on margin yeilds. This suggests that there are ample suppliers.

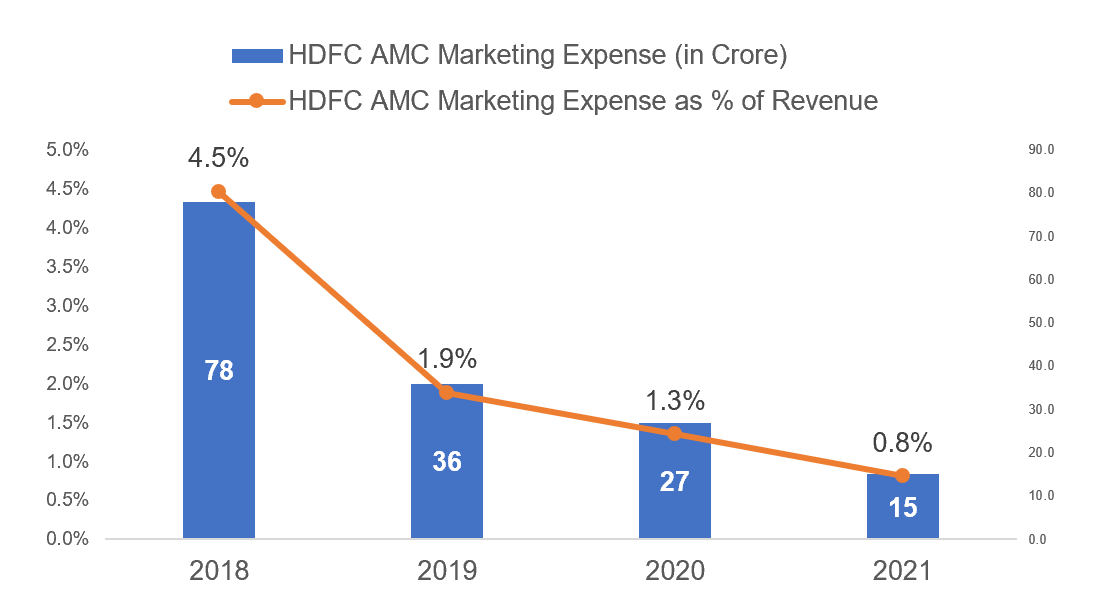

As a result, it becomes necessary to differentiate from competition. One way to do that is improve awareness by spending on advertising\marketing. Here is a trend of advertising expense incurred by HDFC AMC over a few years. Surprisingly, the spend is decreasing consistently (in both absolute terms and as a % of revenue)! On a lighter note, in 2021l “Office Cleaning and Security” expense (16.7 crore) is more than advertising expense.

Do let me know what you think could be management’s thought process behind reducing advertisement expense over years.

Nice observation. My first thoughts on this - I would also see how is the graph of advertising expenses for other AMCs evolving.

Also, would be important to know that what really helps sell in this industry. Does advertising really results in meaningful uptick? It could be that management may have realized that advertising is not that beneficial in this industry than maybe distribution, partnerships, salesforce and actual NAV performance…

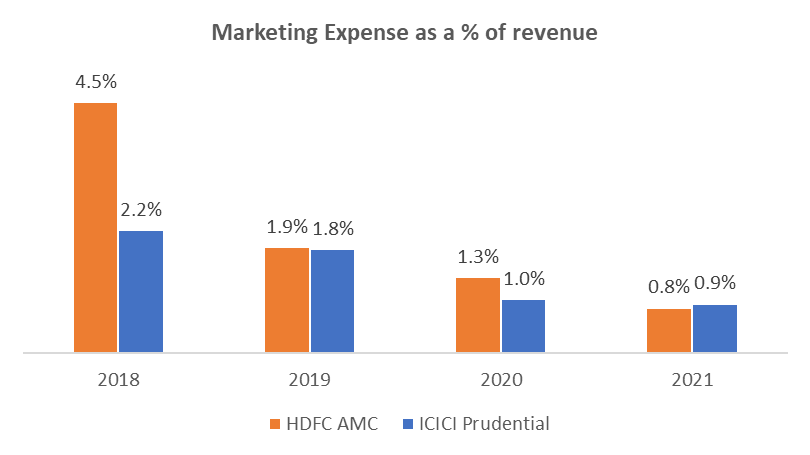

Hi @Investor_No_1, very interesting thought. I did compare the expense with ICICI prudential who is also a big player. Interestingly they’ve also reduced marketing expense by more than 50% (snapshot attached).

How do I find out if managements believe that advertising may not contribute meaningfully OR if this because of some other reason?

This probably has more to do with 2019 regulation changes where such expenses are now supposed to be booked directly under the scheme expense ratio. Only during NFOs, AMCs can promote from their balance sheet. This results in lower net realisations from the schemes (thus lower revenues on AMC level) and higher margins.

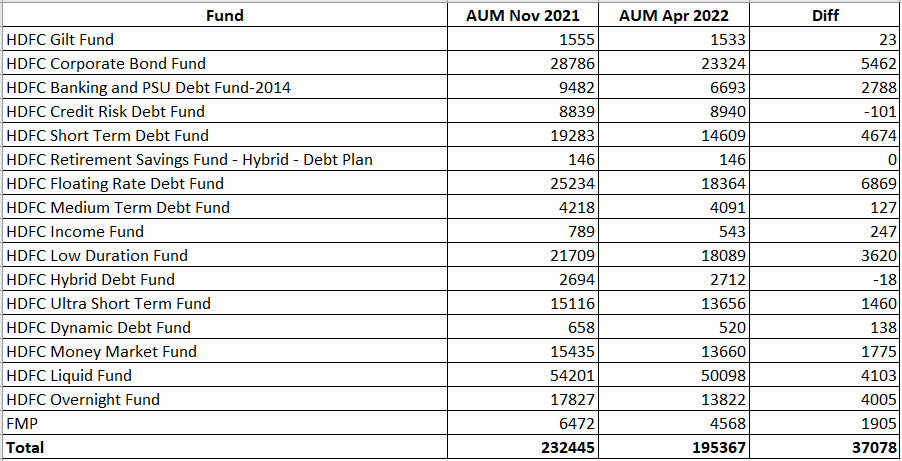

HDFC debt funds AUM used to be very stable. But it came down quite a bit in March. Below is a comparison between AUM in Nov 2021 & April 2022 (as Nov 2021 is the peak so far).

Any ideas on the challenges HDFC is facing? Other AMCs have not seen such a quick fall in debt funds

I could think of 2 reasons. One reason could be that who had redeemed may have anticipated a hike in interest rates, and in order to not lose anything redeemed. The other reason could be, people may have redeemed from debt and moved to equity, timing the market.

The above table looks that way, as high redemption happened in such categories like corporate, floating rate, along with UST, MM, liquid and overnight.

I think HDFC has very high AUM in liquid fund category, could be the same with all short term categories, if that is the case, then all other AMCs funds must have got reduced in proportion to their AUM.