Fact of the matter is There are seemingly better choices being offered by other AMCs (Mirae, PPFAS, Quant, canara). Given so many choices only ill-informed investors could be SOLD with sub-par quality. As in case of car buyer who looks at mileage for before buying a car, most investors go on star rating and annual gains. Once I realised this I sold my entire holding few years back. Still tracking Asset Management sector as it is relatively easy to track and may be few opportunities might come in future (IPO)

1 Like

The first thing many mutual fund sip investors look at is returns, specifically sip returns. I have quite a few friends who do that, they don’t have much knowledge about fund standard deviation, Sharpe ratio, alpha etc. So the primary factor is returns. If one goes to value research and check out the sip returns for most categories of active equity funds for the last 5 years, HDFC funds don’t feature in top 5.

Disc:- Invested.

2 Likes

Apart from organic growth, I personally feel they should seriously look for acquisitions. The challenge with AUM growth is there for most of the firms. And it will get even tougher with new players coming in and increased focus on passive funds where no one company can gain advantage over others purely based on performance (SBI & Edelweiss were lucky enough to get funds from EPFO on a regular basis due to the selection process. SBI was preferred as it’s a PSU).

When such challenges are there with growth, the logical option for (m)any AMCs would be to look for acquisitions or look to exit like L&T did. I feel HDFC is hesitant to look for acquisitions mainly due to the fact that it will dilute their profit margins as most other MFs are having lower margins and when common schemes are merged, the expense ratio may go down further. I guess they should put growth as first focus, get to a very large size and that will be followed up with good profits (in absolute numbers and not margins). They lost two positions in leadership in 1.5 years. If some the companies in the 4 - 10 positions merge that becomes a risk for HDFC then. They should let go of their concern on margin dilution and work something out with the likes of Kotak or Axis and aim for double / triple their AUM in short few years.

1 Like

Not as simple as that. The share of regular funds is still large, but AMFI stopped disclosing this I think. So distributors play a big role in garnering AUM for any fund. The NFO’s success to the majority extent comes from this, the channels that exist which bring in the AUM, along with the tech savvy, DIY generation. Of course, the later part of the success of any fund depends on the category it belongs to, along with the obvious state of the market, management’s decisions etc.

Quantum’s equity fund a few years ago tested the patience of investors, who stayed with it might have got rewarded now. It is hard for a retail investor to not feel left out when all other funds are performing because almost all of the retail investors choose MFs for a reason. I don’t think they can afford the loss of a few years of time staying invested with their fund not performing. Even if you trust the ability of the fund management, it is hard to guess how long would it take for the fund to perform, else one has to understand the PF and then take a decision of continuing with the fund or not, which defeats the very purpose of investing in MF in the first place.

So there are different angles to this business, but ultimately, the fund has to perform, otherwise I don’t know how long an AMC can push funds through channels, how effective will be the push or the pull because of the brand name, or how long investors can stay put for any reason, individual or because of their distributors.

Not invested.

Completely agree with @Investor_No_1 on this.

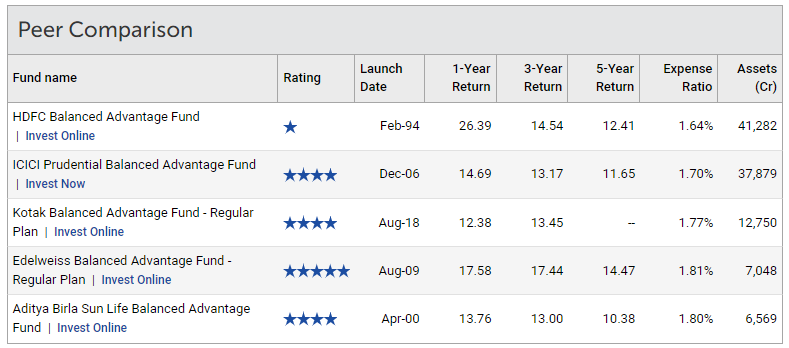

HDFC Balanced Advantage Fund follows value investing style. It usually is the case that market takes sometime to recognise the fallen angels’s worth. Prashant Jain in his recent interview(most probably with ET Now) has mentioned, market takes long time to recognise the actual worth of the stock and some times the pain period is more but then based on his experience, the longer the pain period, bigger are the gains.

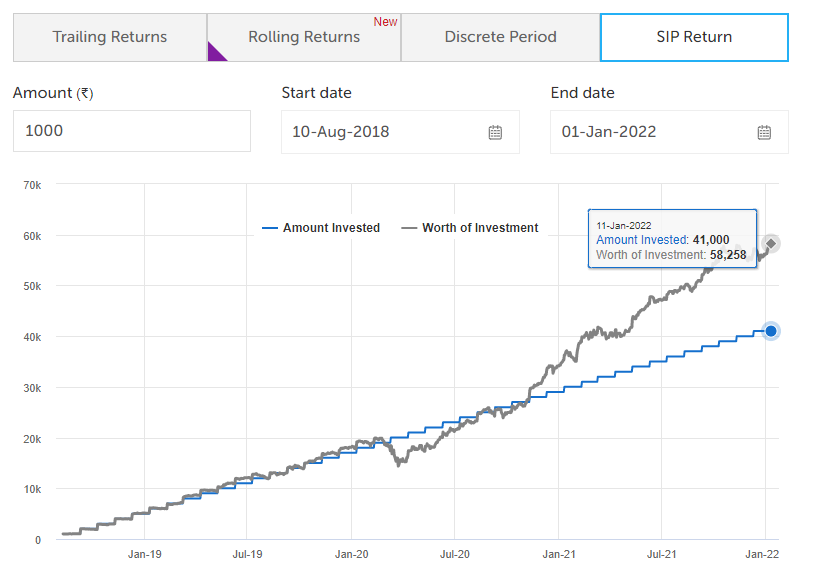

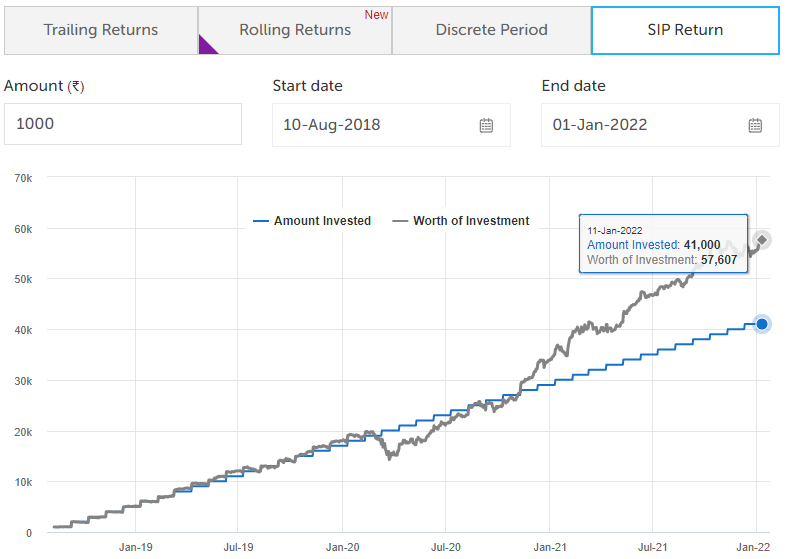

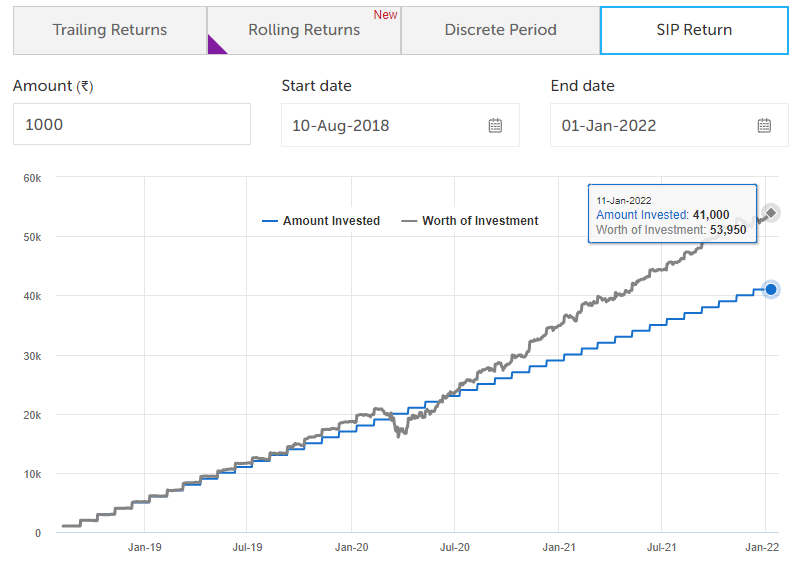

I will explain this with an example. Assuming majority of rational long term investors invests via SIP mode, here are the returns generated by HDFC Balanced Advantage Fund and Kotak Balanced Advantage Fund

HDFC Balanced Advantage Fund - Direct

HDFC Balanced Advantage Fund - Regular

Kotak Balanced Advantage Fund - Direct since its inception

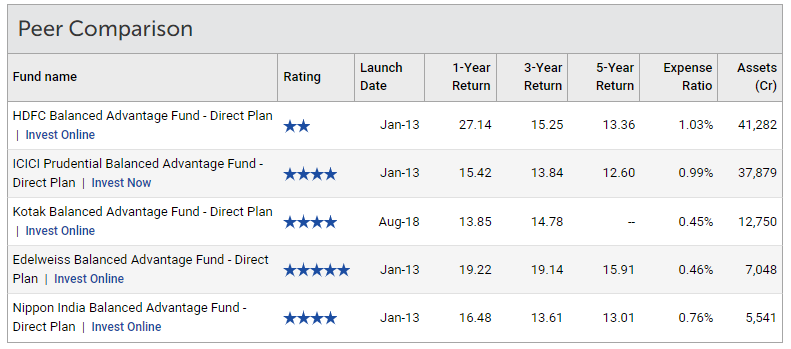

ICICI Balanced Advantage Fund - Direct

Edelweiss Balanced Advantage Fund - Direct

The star rating given by valueresearchonline is shown below.

Now, if you compare the returns, HDFC Balanced Advantage Regular and Direct SIP returns are closer to the 5-Star Rated Edelweiss Balanced Advantage Fund. However, it is given one star for Regular and 2 stars for direct as per the metrics from Valueresearchonline. I am not against the metric system followed by valueresearchonline but then in the end HDFC Balanced Advantage delivered the returns even though the AUM size is biggest among all.

This all connects to Navneet Munot’s message in the latest concall - KYC to UYC. Now, HDFC AMC is in business for more than 2 decades and also they are performing its just that their investing style is different. It worked for some funds but not all. He also has clarity about how the investment needs of millennial based out of Metro like Mumbai is different from a millennial from a small town in Bihar which he mentioned in this video. It all comes down to how you package your different products according to the needs of investors.

Also, at the same time, some of the HDFC funds did not perform up to the mark and certainly the management needs to increase their focus on this.

Yes - This is a valid concern and as you rightly pointed out, Axis did better and so HDFC needs to work on their sales engine.

SBI MF has overtaken as market leader due to their access to EPF money and also some good work done by its investment management team. And Navneet Munot was its Chief Investment Officer and currently MD & CEO of HDFC AMC.

Have a look at the below holdings of SBI Focused 30 fund - There is Google(Alphabet), Netflix and Nvidia) constituting ~14% of AUM

The Scheme may seek to invest upto 20% of its net assets in foreign securities.

In my view, Navneet Munot’s performance is on track. He is filling in the white spaces quickly.

Disc - Invested & biased

7 Likes

For a business in this segment, following are important to stay on top of the game

-

Product development roadmap - Easiest to do once the thought process is clear. HDFC AMC management was resting on past glory and not in touch with the needs of the current market, with the new CEO this roadmap has seen a clear improvement

-

Shaking up sales teams - Once again, this is culture driven and can be changed in 2-3 Q’s. Once products are launched and AUM mop up is not as good as competition, you make channel sales teams introspect and push them to spend more time in the field. This should be happening since the management now has clear data at hand to show the sales engine is not as vibrant as it should be.

-

Making the brand relevant and contemporary - In today’s times you need communication and a digital way of engaging with urban customers. You also need relationships to be built with the new age digital advisors who will emerge as large intermediaries in 4-5 years time. Legacy distribution channels like bank, IFA and wealth managers need attention and incentives. New CEO is making investments here, this should start showing results in 3-4 Q’s.

-

Performance - The biggest problem plaguing HDFC AMC was the over reliance on a single individual and his style. This was their biggest asset till 2015 but not so anymore. This is usually the last factor to change and the toughest to control for an AMC.

These are the things we need to track, the first 3 are lead indicators and any improvement there will start showing up in quarterly AUM numbers. As always, track the business moves first and numbers later.

Disclosure: I am a SEBI registered IA and a boutique asset manager, invested for self and customers. Transactions in the past 30 days

14 Likes

How do you see point 2 for SBI MF?

They raised about 14000 crores in August for their Balanced advantage fund NFO and have grown it to 23000 crores by Dec 31 (almost 9000 crores incremental aum growth, in 4 months post NFO).

The same fund in HDFC stable is one of the long term star performer but their AUM has been around 41000 crores for a long time now. I can understand some interest generated when a NFO is launched. But wondering what they are doing right to increase the fund size post NFO as well, which at this moment, not many AMCs are able to do.

1 Like

Exactly this. The pie is so big in AMC space is that it can easily accomodate multiple winners.

SBI MF until 2012 was in an even bigger limbo on the sales team energy front. What really got things moving was the fact that SBI started focusing on wealth management as a serious offering - hired senior folks from the industry at market salaries and even went to the extent of structuring their compensation differently from their workforce on the banking side. These senior folks spent an year or so building a connect with internal stakeholders from corporate banking and SME lending teams, once these teams started facilitating meetings for the wealth managers with their customer base AUM just took off. Naturally a good chunk of it started to come into SBI AMC schemes.

Then Navneet Munot figured out that SBI AMC was best placed to tap into the steady long term equity flows AUM of the EPFO, EPS constructs, given that Govt organizations prefer to work with fellow Govt organizations. This was the game changer from an AUM point of view, though at much lower margins on their index fund, ETF and passive offerings.

Smart managements figure out pockets that can work for them where they have limited competition. Whereas the outgoing management of HDFC AMC was slightly disconnected from the playbook of the post 2015 era, they kept doing the same things that worked in the earlier period without trying out too many new things.

We investors only see the final outcome of business decisions, by the time numbers change it means management has already been doing the right/wrong things for 2-3 years.

Given the increase in SIP inflows for the industry and the way newer players are able to garner respectable AUM, a large AMC with a well motivated sales team should be able to increase AUM relatively easily. This remains a growing market where most players will be sub scale, even if they are relevant and deliver good return to their unitholders. While digital platforms will make it a level playing field over a period of time, plain old IFA and bank network still rule the roost in the majority of the industry. A leading player has enough resources to invest into digital marketing as well, and most of the leading players are already doing this across AMC, broking, life and general insurance.

20 Likes

Just some information I came across. I have a subscription to value research mutual fund insight magazine. In the latest edition they calculated which funds attracted the highest sums of inflows and outflows in 2021. As per the article there is no straight forward way to identify inflows/outflows from any fund as there are no direct disclosures available. So, they estimated them based on the daily AUM and NAV disclosures.

As per their calculation there were 3 HDFC funds in the bottom 10 funds by net flow. HDFC FlexiCap Fund and HDFC MidCap Opp Fund saw an outflow of 2700 cr each and HDFC Top 100 Fund saw outflows of 2200 crores.

Top 3 funds with highest inflows were SBI ETF Sensex with 12400 cr, SBI ETF Nifty 50 with 10400 cr and Parag Parikh Flexi Cap Fund 9200 cr. As per the article SBI ETFs are seeing huge inflows from EPFO alone.

I would have attached the screenshot to the article but thought that might violate the copyright, so just posting the gist of it.

11 Likes

Hello, i am a newcomer to this forum. Have been investor in market since 2008.

My funda is simple to keep a track of demand and supply, look for yearly sales growth, roe and roce.

Invested in hdfc amc since begining. I personally feel hdfc group has become a big fat elephant and needs an overhaul to stay relevant in market. Its peers are way aggresive and are agile to respond to ever changing market

Gone are the days where you invest just by the name. I personally think it will take more time to see changes in hdfc amc

Any other views are welcome

1 Like

LIC has been steadily increasing stake from (nil / <1%) in Mar 2020 to over 6% in the Dec 2021 quarter.

Hope they see something in HDFC AMC that we don’t see (yet)

Perhaps a slightly off-topic question:

LIC has more than 36 lakh crores as AUM. I guess most of them would be invested in government securities. But who would be managing their assets (including equity investments). Do they have their own asset management team OR have some AMCs do it for them? (Same question for all insurance companies and their assets)

2 Likes

Lic or for that matter govt will put money which has very limited risk. They know hdfc group is not going anywhere. They are fine with slow movers and risk free returns

1 Like

I agree with views expressed by Mandar to some extent.

LIC seems to be increasing the stake in some stable or high dividend stocks, as per screener data. Some examples are Coal India, HDFC AMC, ONGC, ITC (Not increased but stable at about 16%), Tech Mahindra (have increased from 1.31% to 4.98%).

At times, they do invest in non PSU companies as we can see.

I am not sure how they select such companies, since business model of Tech Mahindra is risky than other IT companies due to continuous acquisitions. So sometimes, it seems that, they look for stability and future growth as well.

I may be wrong in assessment, but have observed LIC holding Tech Mahindra to above 5% before merger/during merger with Satyam as well.

3 Likes

HDFC AMC - 3000

Nippon AMC - 475

4 Likes

How much worrisome the loss of market share could be for HDFC AMC? Do you believe it’s going to increase in the future considering HDFC Group as parent company won’t sit idle?

Also, if anyone tracks much, does the current valuation satisfy the earnings, or is it overvalued still?

Disc: Not Invested

3 Likes

Aren’t all these connected? Performance brings more investors who increase AUM which gives bigger market share?

Why would individual investors invest in any particular fund or fund house unless they are performing? Or is this contribution result of sales force? How could profitability remain the same despite the odds, if not for the cross selling? If yes, how long can this continue? Unless we know how much regular funds are contributing to the AUM, we can only speculate, because if direct fund investors are increasing, who not necessarily are DIY folk, they have umpteen choices today.

For a lot of investors, MF means equity MF, because they know about many fixed income products, may even have decent allocation to debt already. For who don’t have such debt allocation, brand pull can exist in the case of big names, as debt more or less fetches the same returns, so better to go with big ones, whose AUM is anyways large, so they don’t take big risks and have a very diversified PF, unless stated otherwise, as in the case of credit risk funds.

I don’t know if market has grown in proportion to the participation, so there are many pockets to generate alpha, or the participation is much higher compared to the equities of all forms combined, so it is becoming increasingly difficult for one and all, along with the impatience of new age investors, which in a sense is correct, along with SEBI’s rules which has cut the wings and restricted the space a fund can operate in, increased competition, have made moat lose its existence.

Not invested, but interested in the MF space.

3 Likes

Company seems to hand out lot of esops. Today’s announcement says 182900 esops are allotted. Hope this is enough to incentivize the employees.

2 Likes

Agreed they are all linked to fund performance. In the end every investor will try optimize their return and move to a better performing fund. As mentioned in one of my earlier posts if a new investor with limited experience and who hasn’t seen complete market cycle goes to value research and check out the sip returns for most categories of active equity funds for the last 5 years, HDFC funds don’t feature in top 5.

So for me HDFC funds’ performance improvement remains the key monitorable.

2 Likes