Monthly inflows data for the AMC INDUSTRY.

industry as a whole inflows in oct 20 was 28 lakh cr…

For oct 21 it is 31 lakh cr… Yoy growth 10%.

But MoM It degrew by -19%…

Hdfc amc

Oct 20 3.75 lk cr vs oct 21 4.48lk cr… Yoy growth 19%.

Mom growth of 1%…( sept 21 4.42 lk cr)…

Sounds interesting amdist all the talks of hdfc amc loosing market share,.

Disc: invested

4 Likes

HDFC AMC was at no.1 position couple of years ago. Now they are at position no. 3 and the gap with no 1 & 2 players is slowly increasing. Regarding the MoM AAUM growth, please see details below. SBI & ICICI has grown higher than HDFC (particularly SBI which has grown on a much higher base). These numbers are inclusive of Domestic FoFs

Source: https://www.amfiindia.com/research-information/aum-data/classified-average-aum

6 Likes

Here are my notes based on Q1 & Q2 con calls.

Industry Analysis

- In the current fiscal year, out of 937 billion overall industry flows, 459 billion or 49% is from NFOs

- Recent higher growth in AUMs of ICICI and SBI is also due to their big NFOs

- There are good inflows in “Others” category for overall industry – 778 Billion

- 354 Billion in ETFs

- 345 Billion in Arbitrage funds

- 79 Billion in International FoFs

HDFC AMC Analysis

- NFOs are offered at materially lower margins and HDFC AMC wants to go for NFO only if it fits its guiding principles

- Build scale, build quality, build profitability without compromising on any of these

- Navneet acknowledged that there is interest coming in thematic funds coming from MFDs, Advisors, Investors

- BFSI thematic fund is launched during this quarter and there are some more in pipeline

- HDFC Multi-cap NFO in equity-oriented category is expected to be announced in near future

- Navneet mentioned about allocations becoming broader based in the market

- First international(from HDFC AMC) passive fund MSCI World Index is launched in the recent past

- Overall equity oriented funds industry is 15 to 16 lakh crores

- HDFC AMC has 2 lakh crores in equity oriented AUM

- Navneet acknowledged about Fintech driving equity growth in terms of adding individual folios

- Fintech channel contribution to the industry is 35k to 36k in AUM

- HDFC AMC wants to have more engagement with them in next couple of quarters

- Not seriously looking at inorganic growth(acquisitions) at this moment

- I personally think this is not the time to look at inorganic growth as valuations will be at peak

- Also, due to SEBI’s reorg guidelines, they cannot have more than one fund for the category and with merger, it can pose problems

- Focus on increasing active managed funds share but also remain a leading player in Passive income by filling the white spaces

- HDFC Developed World Indexes Fund of Funds is concluded

- HDFC NIFTY50 Equal Weight Index Fund(passive smart beta fund)

- NIFTY Next 50 fund (passive fund to be launched based on Nifty Next 50)

- Nine new ETFs are in pipeline

Navneet has broadly worked on all the things mentioned above. There are launches in thematic funds, international funds, new recruits and also into ETFs.

In my view, here are the things which Navneet is doing good qualitatively

- Adapt to the new normal of digital

- There is a clear progress here just looking at the website.

- New CTO(Ex- HDFC life) is recruited in August 2021

- KYC(Know Your Customer) to UYC(Understand Your Customer) Approach

- There was a disconnect from marketing teams’ usual way of working due to Covid and this marketing is much needed

- Change management

- He is always acknowledging the existing team’s achievements and well prepared to all the difficult questions to the con-calls of Q1 & Q2

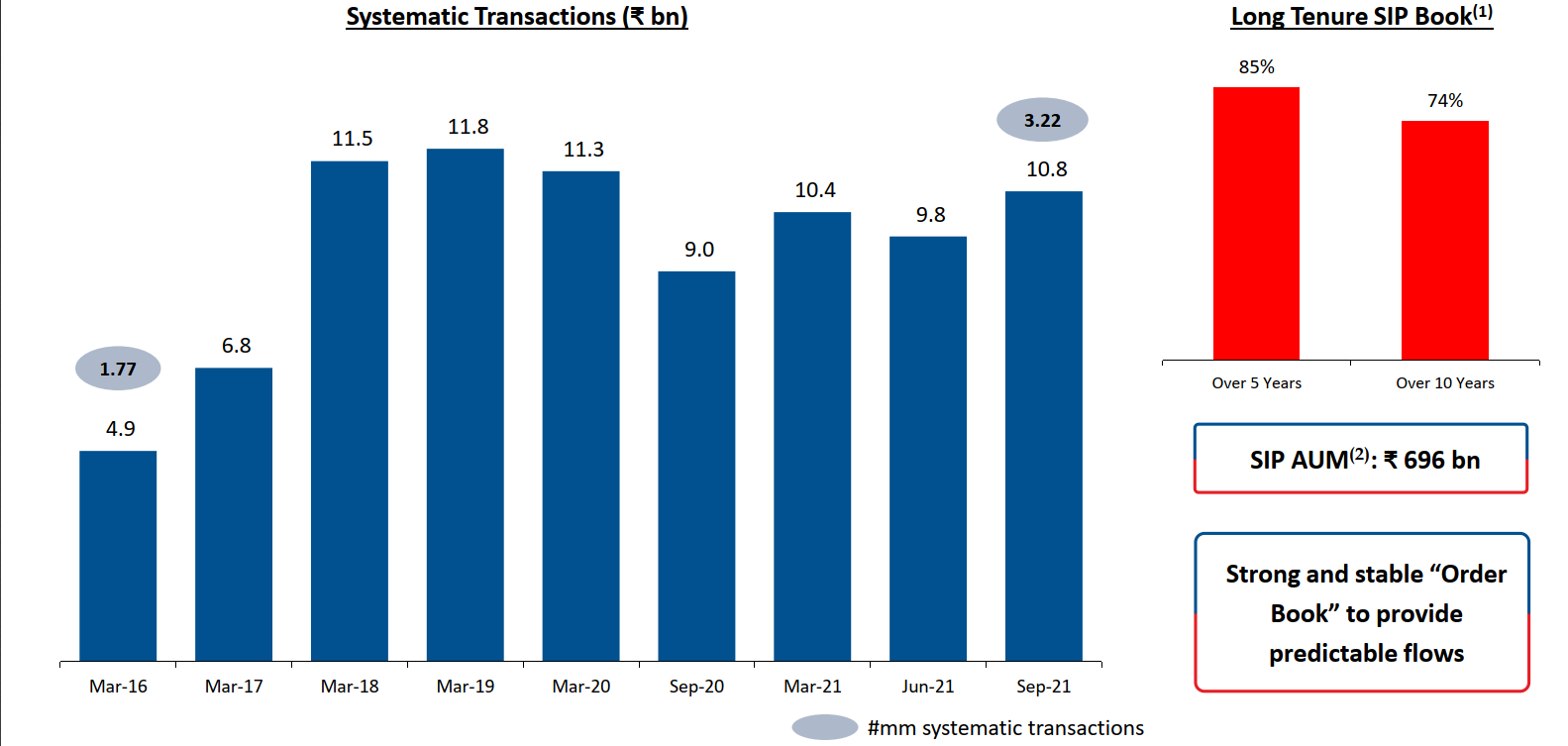

- This quality differentiates a leader from the rest. Especially, 85% of AUM is still with incumbent team and their morale should not be shaken

Valuation

- HDFC AMC has ~5000 crores as investments and all the free cashflow is accumulating nicely

Screen-shot from Screener.in

Considering a 4% after tax on investments gives us ~200 crores as returns per year. In the concall, it has been mentioned that employee expenses are now stable at 7.5% of their revenue. So, if we consider March 2021 revenue for our calculation - 2194 crores. The employee expenses will be ~164 crores. The expenses excl employee cost will be around ~250 crores. At the operating margin of 80% and no other surprises in a steady free cash flow business like this, one day, the investments income covers the expenses. What remains then is the perennial cash flow business in case they are not looking at inorganic growth(with SEBI’s reorg exercise, I think they may not unless it is very much compelling).

I always felt surprised looking at their business model.

How can HDFC AMC show losses?Heads I win, Tails I still win but may be less.

This is a high quality business backed by HDFC Group which helps in perennial sales.

If someone is looking to buy stocks for their retirement, this is a perfect choice by the nature of its business.

Add to this, due to SEBI’s guidelines, employees will have more skin in the game.

Most probably, Navneet will also focus on scaling the PMS business of HDFC AMC, that’s additional trigger in waiting,

Discl - Invested. Transactions in last week. HDFC AMC used to be my top allocation as this is stock for which I did maximum research. Now, Dmart has taken over with sheer strength. May be one day HDFC AMC wins the race .The other competitors being BSE limited, Laurus Labs, Deepak Nitrite ![]()

27 Likes

Hi All,

After reading this thread right from the start, I have re-established my thoughts that, there is huge runway ahead for Equity investing in India, with just 8-10% population or even less investing in equity at the moment.

That means, Mutual Fund industry in general has a huge opportunity ahead. Though HDFC AMC may not remain no. 1 player as evident from recent past, there will be still long tailwind for the listed players.

In such a case, I am pondering over some thoughts and questions:

- If most of the population is still not invested in equity, how generally they manage inflation? What are the other inflation beating avenues in India?

- We have seen in the past that, many MF houses have closed their business in India, including Fidelity. What could be the reason for their closure? (It could be that they were not able to remain profitable, but apart from that, are there major road blocks?)

- Why Personal Finance is neglected subject in most of the curriculum? I personally see that, now young college going generation is also taking interest in Direct or Indirect Equity, then having some education in personal finance could be helpful. Are there any universities in India moving in that direction, at first or second year of degree curriculum?

- What could be the other roadblocks for such a huge population staying away from Equity MF(s)?

I have started thinking on these lines recently, after realizing that, in many nations, Equity investing is much higher.

This is just to know the thought process of others, on this topic. Though the participation in equity is going up in past 2 decades, due to efforts by SEBI, BSE, NSE, NSDL, CDSL, and others, it still looks like that, it will take some time to reach 50% population.

Disc : Invested in HDFC AMC.

4 Likes

Agree, but that’s true for every AMC business. I think the point all critical investors here want to make is that yes the business is excellent but the execution of HDFC AMC has not been on same lines in last few years - with the likes of SBI/ICICI AMCs etc leading the show. As far as that happens, underperformance would be guaranteed, as majority of the huge runway and market ahead would be taken over by competitors…

Disc: Invested as small position. Have respect for HDFC group thats only reason for remaining invested even during underperformance

3 Likes

Interesting questions, some thoughts to ponder below on your 4 questions -

- I think still in many small towns, and even big, people prefer real estate - land, apartment etc. over equity as first choice. Even Gold, FD, insurance have a preference. Most people never try to compete with inflation and depend on increase in salary/income to fight it rather than investments.

- This is not just case in AMC, many foreign players have not been that successful in Insurance/Banking (directly/indirectly as per regulations) as well.

- Personal finance is not just about equity, its about Money. And discussing money in family etc. is still not that welcome yet. One reason could be that we need more engineers, doctors etc. to build a nation. We do not need pure investors…as anyhow these engineers/doctors would later on become investors (if they do well or not that’s upto them but market will get their money). So Personal finance is, as its name suggests, a “personal” choice and hence is mostly self/family driven.

- As long as equity remains volatile - which it will - all of them will remain away from much equity exposure - unless they reach a basic financial and/or knowledge level - so it will be a slow process - One catalyst can be these new age digital brokers/fintech firms which will bring exposure to masses very quickly.

Disc: Above thoughts personal and for academic purposes. I can be wrong in all my assessments

6 Likes

Thanks for your reply.

For point 3, my intention was that, at least fundamental concepts of personal finance should be introduced in the college, to avoid mis-selling of products to the young generation. I have seen many people investing in wrong products due to lack of education, which is hampering their progress and eventually nation’s progress.

For point 2, I am still finding it hard to understand why mutual fund house could be unsuccessful if so many people are now investing directly in stocks and CDSL stock price is the best indicator of that.

Anyways, this is just few thoughts and I may be wrong.

This is a large issue, one that could be addressed from different angles and endlessly.

It is said that, Indians for years have been investing in assured return products, along with the safety of principal, like FDs and government schemes like PPF etc. So unlike the lottery schemes that exist in foreign countries, we Indians do not blindly chase financial products, but want assured returns. Also, in these decades, interest rates have been high because India was not open to the world.

We are a large country and a diverse country, diverse not just w.r.t cultures but the opportunities that we have, admit it or not, all Indians did not have the same opportunities in the past, we do not have the same opportunities even now. This applies to financial assets too. For someone who has a couple of buildings in the heart of city, for someone whose land appreciates disproportionately, for someone whose entire family for generations has been in government service, investing in equities seem inferior. Gold is another asset, we all so like and buy regularly, which also comes handy when need a loan. So, investing in equities in not necessary for many, it is one among many choices.

Things have changed in the last 25-30 years. Interest rates have come down, there are more educated people, less government jobs, real estate is out of reach for many reasons, so the need of extra return to realize goals and dreams, hence the increase in the interest of financial assets. But here, the lack of transparency, the false promises when sold (documents are transparent), the inability to understand and accept the volatile nature of the markets, the hurt both financial and psychological impact the future of participation. So fund houses which closed their business may have anticipated a similar growth like in the West or somewhere else, perhaps did not have a holistic view of how Indians invest, how Indians look at money and assets. Sales, products, performance may have been worse too.

The current younger generation investing in direct stocks, evident from CDSL rise is because of many reasons, as we know, but the participation should be measured in sideways or bear markets. Would people still buy when the price does not move or goes down?

There are stages of learning, so as the learning curve decreases, as one becomes knowledgeable, one moves on to next level, as evident from the increase in index investing, the number of index funds and ETFs launched covering many indices. This participation can be considered as an increase in investors knowledge. People who invested in active funds in the past, now think that they will not get such returns and shifted to index investing, or people who are certain that markets have matured to certain extent and active funds will not deliver as they did in the past are investing in indices. Sign of investor awareness I guess, or it could be a fad, this will fizzle out when active funds perform again, due to information asymmetry or with better selection of stocks etc.

The participation is increasing, as shown by numbers. So the journey has begun, but will this journey be a secular story, one that continues for a couple of decades, with intermittent falls, I don’t know but looks like it.

5 Likes

NFO’s launched since September -

HDFC Developed World Index FOF (mopped up ~1,300 Cr)

HDFC NIFTY NEXT 50 Index Fund

HDFC Multicap Fund

Clearly the product team is wide awake after the new CEO has taken over. If the AUM mopped up is below expectations for the Multicap fund, one should expect him to “re-energize” the channel sales teams and give distribution the much needed push.

While performance of the actively managed equity funds will matter more over the medium to long term, the short term AUM will depend more on how product launches and how much the distribution engine can push. Generating incremental equity AUM of 10,000 - 12,000 Cr in Q3 purely through NFO’s should be possible for a market leading AMC.

6 Likes

HDFC Nifty Next 50 Index fund generated around 300 crores.

2 Likes

Till September, ICICI’s fund has the highest AUM among all the NN50 index funds, of 1588 crores, but as per Valueresearch, it was launched in 2013 January. SBI’s fund which was launched in May, this year, has AUM of 345 crores. So 300 crore AUM for a NFO is good, indicates the push, I think.

The higher the AUM, the more the profit, even if they are index funds or ETFs, then the profits are directly linked to the sales, but I think you can only push so much because the market or that particular index has to perform, in order for the sales team to show the return and sign up new investors. I mean, there is no differentiation in index investing. UTI is a strong competitor here, all the big names are present in the indices, even Navi is present.

No investment in HDFC AMC.

Yes, this is where acquisition would probably help. Even if the target AMC has similar funds, it still helps in growing AUM (hopefully with less redemption). In this business, size really matters.

UTI IDX fund is the biggest player in this index fund space; how does launching new NFOs help, apart from non savvy investors getting in at Rs 10. After the launch, it’s no longer a NFO, apart from the large corpus how will it catch up to UTI or any of the other existing thematic funds in play by others?

1 Like

Well, my point was that there are already many funds which were started long before, and have good AUMs more than HDFC. HDFC can catch up or even lead in the future, but the advantage of being backed by a bank exists for other bank backed AMCs which have a good presence in index funds, particularly SBI and ICICI. In the ETF space too the situation is the same with more competition.

So despite the index space is getting bigger, it is also crowded in a sense. But with index funds, the increase in AUM will not be a problem, which exists with active funds, so no closing of inflows, no limits on lump sum etc. will happen. Also I guess investors will redeem like they do in active funds when the market falls. At least the people who invest in indices on their own, know about the performance of indices, and are patient, and would invest more if the market falls. But if much of the AUM here is pushed instead of pulled, I guess, then the situation could be the same as with active funds. And I think I remember, the share of direct and regular funds is not reported separately, but reported collectively.

No investment in HDFC AMC.

Right, I wasn’t getting the drift of NFO launches. Any AMC can launch NFOs and if the point was that AUMs overall grow, that’s fine but how does that specifically help HDFC AMC beat others, I don’t get it. IF my initial MF investment example in my 20s is any marker, I switched randomly because new NFOs came out regularly. I fully expect, that cash rotation out of these NFOs to happen apart from the lucky streak MFs that hit a theme which takes off.

I’m invested in most AMCs in equity and I’m just banking on AUMs they manage as a measure of safetly. I don’t recollect seeing any metrics on folio churn, avg SIP size, stickiness etc numbers from these AMCs

I don’t know but one reason for more number of NFO launches is because of the bull market. Another recent reason could be the educated and tech savvy investors who are also interested in indices, themes and international equities. And here, I don’t know but sales teams could be a differentiating factor, perhaps these are more nuanced and are not known to all. They have the customers’ data, their spending patters, their deposits, their balances, their prior investments, so all this data is analyzed and correspondingly NFOs are any other products are sold. If this nuanced process gets better and yields returns both to the AMC and the investors, the AUM will increase.

Active funds are different as we know, each fund manager has a different style of investing. Here, they could bring a lot of difference. But I think I am not sure if just the name of a fund manager will garner AUM and returns, instead of a process, be it Prashant Jain or Sankaran Naren, anyone else. It was their touch that made them Midas, they were not Midas.

Of course, I have little experience in investing in both MF and stocks, so my interpretation could be wrong and HDFC AMC could very well become the most profitable AMC in the coming years.

Not invested in HDFC AMC.

1 Like

more number of NFO launches is because of the bull market

Exactly my thought. MF investors are being lured into thinking that NFOs are akin to equity IPOs which are seeing stellar listing gains. But an informed MF investor will know the difference and will look for the fund scheme that’s already present with good history, performance and has high AUM.

1 Like

NFOs do not get launched necessarily in a bull market, but a bull market does make things easy. I think the tendency to invest in an NFO is more, compared to investing in a stock. There always exists the possibility of not investing in a stock, if one does not understanding anything about that company. Fear also exists along with FOMO. Also, it is psychologically and financially easy to invest in a fund than in a stock. And sometimes the USP in NFOs could just be a single line. I have got an email with the subject “Grow with Taiwan!” for a Taiwan equity fund.

All these lures, gimmicks are necessary for the market to become bigger and wider. The market cannot depend and sustain on only a couple of sectors. So, NFOs and IPOs have to be launched, the market should widen, economy should mature. One who is informed will benefit in such a scenario, one breaks even, one gets disappointed and one will lose. Sometimes you are this side of the fence, sometimes on the other side. Money lost, experience gained, made money later.

One important question is, can Indian market sustain on its own without the external pumping? To some extent, it has been acting as a cushion in the intermittent periods of falls. For now, I think we cannot. The might of dollars and pounds is huge. Withdrawal of foreign assets, market falls, back to gold and real estate. Just saying, no data to backup, not predicting.

Let’s look into HDFC AMC journey from 2020.

In terms of debt market segment, HDFC MF is still going strong based on the trust it enjoys among institutions.

For equity, the management acknowledged the problem last year itself - Q1FY21 Concall.

Then new CEO who was earlier chief investment officer of SBI is brought in.

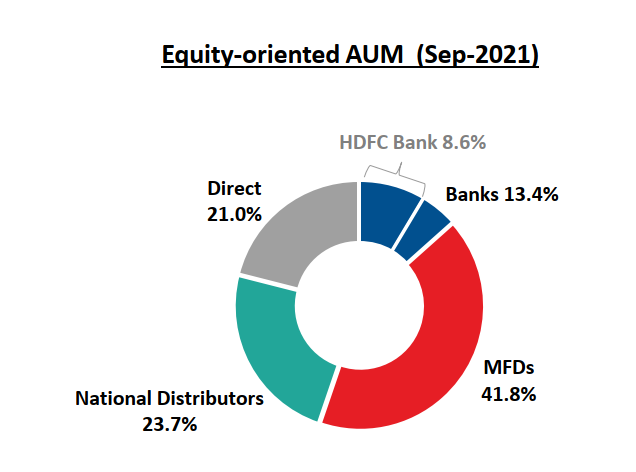

In fact, the financial advisors/planners enroll the new investors into balanced funds in the initial days as it contains ~35% debt component and so lesser drawdowns. HDFC Balanced Advantage Fund is still one of the best in its category. Its AUM constitutes around 20% of overall AUM of HDFC AMC Equity Segment.

Source - Valueresearchonline.com

Regarding others, HDFC Funds are not the best performers from a long time but please check the trend of SIP order book. The trend is whenever there is good equity performance, HDFC AMC with its MFDs and National Distributors just rides the success of overall equity market success.

Now, if the concern is about existing AUM loss. Except, Direct route, rest all work on incentive model and as I explained earlier, the commission rate is tagged to transaction and all the transactions in the past gives them higher incentive. Even NJ Invest which is the biggest national distributor of MF industry will not advise to withdrawal of HDFC funds. They can also convince clients that it is tax inefficient.

For direct route, you mentioned the rationale about investing in HDFC MF Midcap scheme. I believe, I will also take the same route in coming years. In the end, I can sacrifice 1 to 2% alpha for safety and long-term performance.

To conclude, the chance of HDFC AMC losing majority its existing AUM is minimal.

I was watching one video of SOIC about portfolio construction approach and he mentioned the below points.Thanks @Worldlywiseinvestors

- Investing is probabilistic at the end of the day - Nothing is cast in stone

- Business is like a living organism and you need to have a probabilistic mindset assessing how much risk and reward it carries

At this point of time, I am of the view that my risk is less in HDFC AMC due to below reasons.

- It seems to be ticking all the boxes I was looking for

- As I understand this business, I will still be able to average when there is more pessimism

If HDFC Funds turnaround, the reward can be good to great.

@zygo23554 - I was checking the PMS returns in SEBI website and amazed at the AUMs of many PMS funds. As you are closely tracking HDFC AMC, want to understand from you, what are the roadblocks/issues which are stopping big AMCs like HDFC going big on PMS funds?

Discl - Invested and biased

14 Likes

PMS AUM has grow leaps and bounds over the past decade or so. I remember my first meeting with folks at ASK PMS in 2011, their AUM was ~2,800 Cr across all their strategies then. Today they manage more than 40,000 Cr. AIF as a category was almost non existent till 2015 in the public markets domain, today that segment grows at a break neck space.

Traditionally the most successful houses in the PMS space have been boutiques and independent asset managers who do not have presence in mutual funds. All leading AMCs have PMS but it is a secondary priority at best for them. The best fund managers are always sitting on the mutual fund side of the business there.

A few reasons are -

-

Operations in PMS are relatively complicated compared to MF. Every customer needs to have a demat account and a demarcated portfolio, a mutual fund is a pooled investment scheme where units are allotted.

-

Distribution is more demanding in the PMS segment. HNI segment is serviced by large private wealth management teams which are more demanding in terms of service, face time of fund managers and tougher to deal with in general. IFA’s and small distributors are much easier to work with and give more bang for buck for an AMC.

-

Commercials are much better in mutual funds for an AMC, the trail commission is in the range of 70 - 100 bps per annum whereas even the biggest PMS outfit in the country needs to pay out a trail of 1.5% p.a. to their distributors. The Yield to AUM is much better in equity MF than in PMS for this reason. Large HNI customers can negotiate fees in a PMS but they cannot in a mutual fund, it is prohibited to give differential pricing even if one comes in with 100 Cr.

-

Retail money coming to financial savings still has a long way to go in India whereas almost every single HNI already has exposure to the equity market today. As an operating manager, it makes more business sense to focus on a growing segment than on a segment that is already well penetrated and well serviced.

30 Likes