Mr. Prashant Jain reveals his views on the overall outlook.

Few points mentioned by him answered my queries as to why this stock has not participated in the catch up yet.

Mr. Prashant Jain reveals his views on the overall outlook.

Few points mentioned by him answered my queries as to why this stock has not participated in the catch up yet.

Navneet Munot is the Chief Investment Officer of SBI MF from 2008. He is fund manager with similar experience like Prashant Jain who is the Chief Investment Officer of HDFC MF. Navneet will now replace Milind Barve who is the current MD & CEO of HDFC MF. So, Navneet will now move to the business side from fund management. India’s top two MFs CIOs will be in one company - similar to having Dhoni & Rohit Sharma in Chennai Super kings(IPL) team(Just an analogy and not apple to apple comparison).There can be friction due to distinctive investment styles but only time will tell. Here are the things that come to my mind.

What Mr. Navneet can bring to HDFC MF

Disclosure - HDFC AMC is the top holding in my portfolio and I have a SIP running for SBI Small Cap scheme.

Received this email earlier today -

"Greetings from Kotak Mutual Fund!

Please note that the base Total Expense Ratio of Kotak Mahindra Mutual Fund will be changed with effect from 21st Jan, 2021 for Kotak Bond Short Term- Regular Plan from Existing Base TER 1.10% to Revised Base TER 1.12%"

The implications for the pricing power a leading AMC can command are self explanatory.

Discl - invested.

I fail to understand why they need to hoard 4300cr of cash on the books.

They are looking for acquisitions constantly…so the cash helps

Is this something they’ve talked about or taken some tangible action on?

A quick Google search shows the last acquisition they did was 7 years ago.

Hdfc Amc bidded for L&T finance MF business the base bid price was around 4000cr latter on I think L&T has dropped the idea of selling.

I believe in future small MF house like mirae, quanta, will be taken over by big houses.

Disc: Invested

Why do you think that’s likely?

I just listened to the Dec Quarter call where this question was raised by an analyst. The management said that they will be looking at it whenever they decide on the next dividend. I don’t want to be speculative but we may see a special dividend in near future.

Once the AUM SIZE in India will grow there will be reduction in MF fee or expense ratio currently it’s is 1.25% on equity scheme for first 100cr AUM. India charge highest Expense ratio compare to other countries. In future definitely Sebi will bring down the expense ratio to pass on and attract more investors. Due to which it will be difficult for small MF house to manage small AUM base with less management fees…

Yes MF industry is asset light model industry look at there operating expenses and operating margin it’s tremendous. Huge cash reserve on book will attract special dividend and bonus in future

Farewell Milind Barve: The mutual fund veteran who took HDFC AMC to the pinnacle

Another article about Milind Barve.

The acquisition of Zurich Asset Management in 2003 would be the first highlight. Before that, we were known as a good fixed-income fund house. We also had a good equity business. But what we wanted was a high-quality, high-performing equity business.

They have around 4000 to 4500 Cr Cash. As there is no need for capex, they will still be on the hunt for high growth opportunity if any.

The more you read about employees from HDFC group stable, you get the feeling that they are always inclined to process driven approach than being individual superstars. This part gives comfort for long term shareholders to give it a pass for temporary blips. Mr. Deepak Parekh should be credited for inculcating this culture.

Now coming to the change of management, I think Milind Barve’s business chemistry is guardian. He always ensured that expenses and profit margins are under control, did not go overboard about expansion/growth. This explains why HDFC AMC never ventured into thematic funds like pharma or international exposure like investing in FAANG stocks etc. He secured the numbers without taking risk. Come Mr, Navneet Munot, who basically operated in a subsidiary of a public sector bank(SBI). His business chemistry seems to be pioneer and I think he will venture into new areas like international shares exposure and thematic funds etc

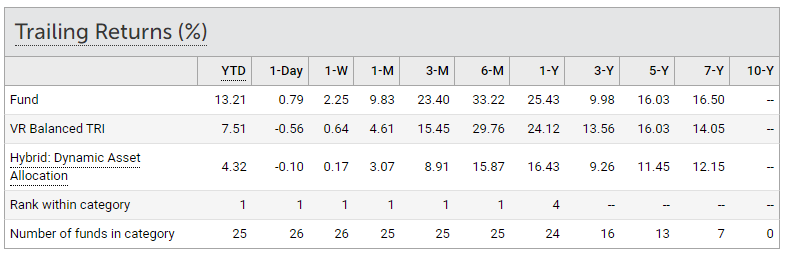

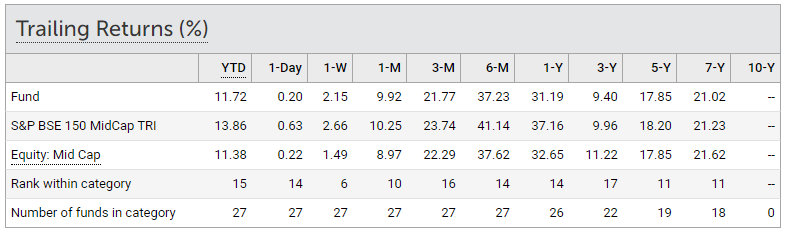

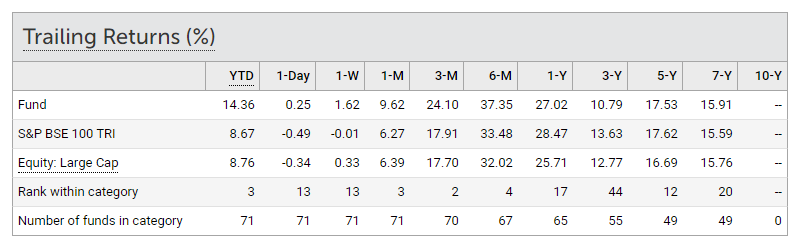

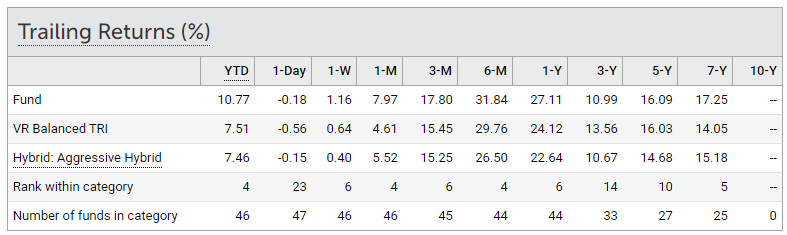

With recent bullish trend in stock market, HDFC MF schemes are going through a turnaround.

Look at 5-Year and 7-Year returns and also rank within the category.

HDFC Balanced Advantage Fund - AUM ~ 38,000 Cr

HDFC Mid-Cap Opportunities Fund - AUM ~ 24,000 Cr

HDFC Top 100 Fund AUM ~ 18,000 Cr

HDFC Hybrid Equity Fund - AUM ~ 16,000 Cr

For most part of 2020, MF industry has seen high levels of withdrawls. Partly due to uncertainty, dismal returns and many people got time(work from home) to enjoy the thrill of trading first hand. The tide will reverse in some time as the success in trading is very less( ~ 1%) and managing an all weather portfolio is not everyone’s cup of tea. I expect green shoots in MF industry and like Morgan Stanley mentioned in their research report, HDFC AMC is well placed to reap the benefits.

When FD is giving around 5%, the above mentioned schemes delivered above 15% in 5-Year and 7-Year duration. For next few years, distributors will showcase returns in nice colorful charts. HDFC schemes are certainly not the top performers but then they delivered the returns to stay invested. Navneet Munot is a lucky guy. Little less pressure in his new job for now.

Aside, recent below action from HDFC AMC to increase participation in ETFs.

Discl - Invested.

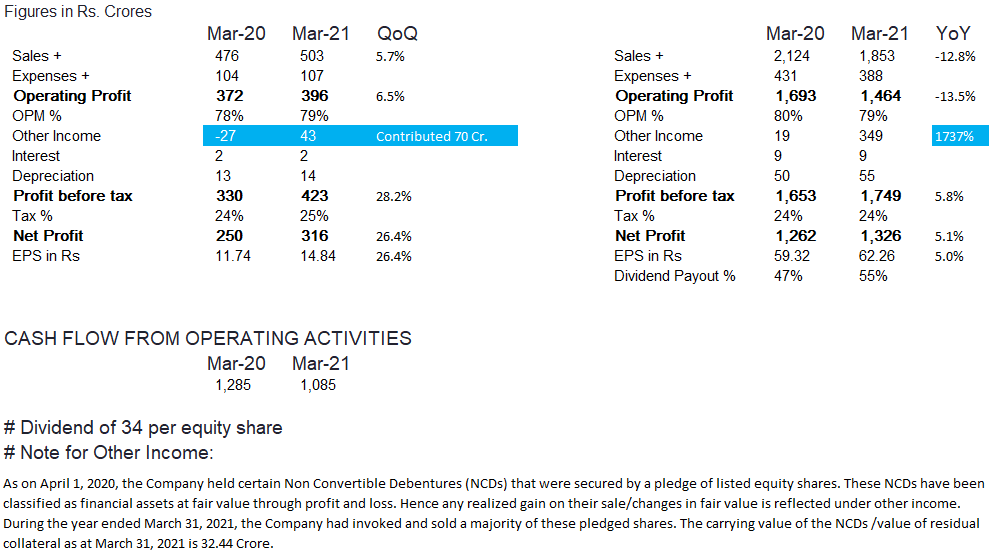

Latest Results (Details at Link)

Overall Summary:

Investor Presentation Link:

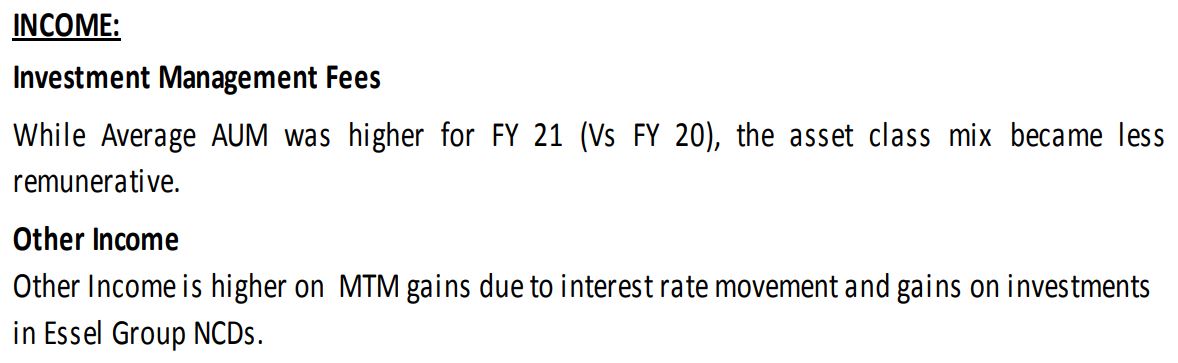

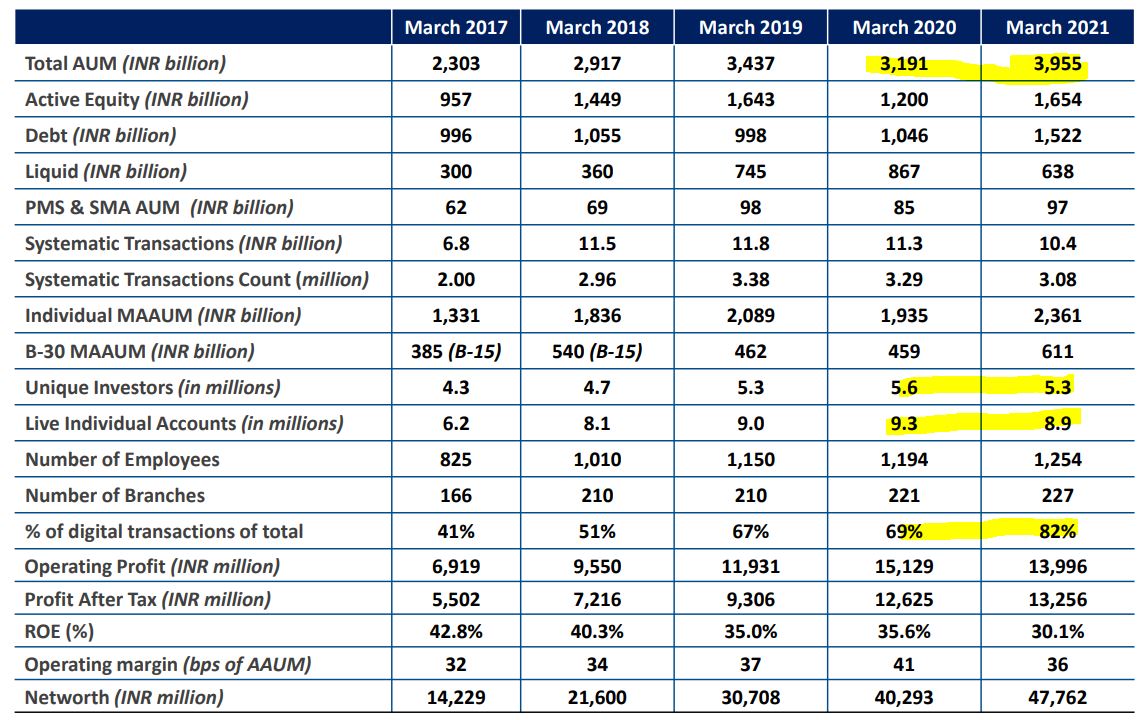

In the deck, below are worth observing -

As they say the returns lies in future growth, attempting a hypothesis- mix of quantitative and qualitative attributes -

Mid to late 30’s would be a upper band likely a ceiling for med term going forward in the era of ETFs, REiT, Direct equity and so on. That is assuming current mix of active equity managed vs rest - passive/debt/liquid etc( which is 40:60 for FY 21), skew of this ratio towards non actively managed fund portion looks more likely than not.

Valuations - 1300 cr in FY 21 PAT - 65K cr mkt cap, can a 50 PE be sustainable or other way can they do 20%+ profit growth for a long time to come? Consistently? They have done this over last 5 years but had some help( corporate tax reduction etc.).

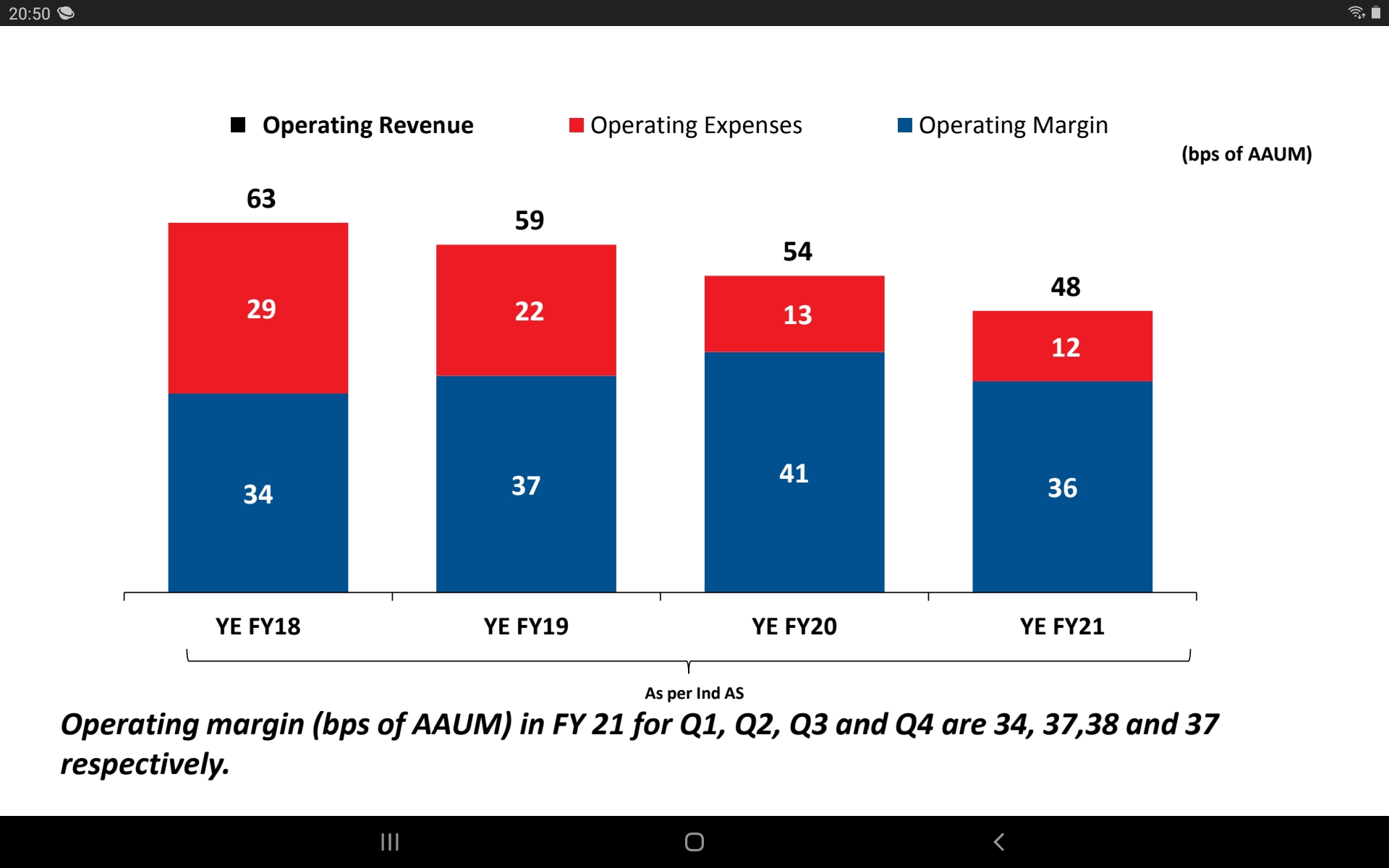

While AAUM growth and yield ( op mgn as AAUM bps) is core areas to look at, can there not be any op efficiency improvements to reduces costs given most of business is now moving to digital?

While digital transactions makup for 82% from 41% in 2017, employee and offices have increased as well by 1.5X - clearly room for demonstrating operating leverage of digital ops. Optically operating exp have come down as bps basis for AAUM.

Competition with innovative offerings will keep coming, HDFC brand helps( more in debt/liquid space and Mr Munot has his task cut out to maintain n grow(?) mkt share.

Invested

They also should plan inorganic growth to boost equity AUM. Did Mr. Munot talk about his vision for the company in the conference call?

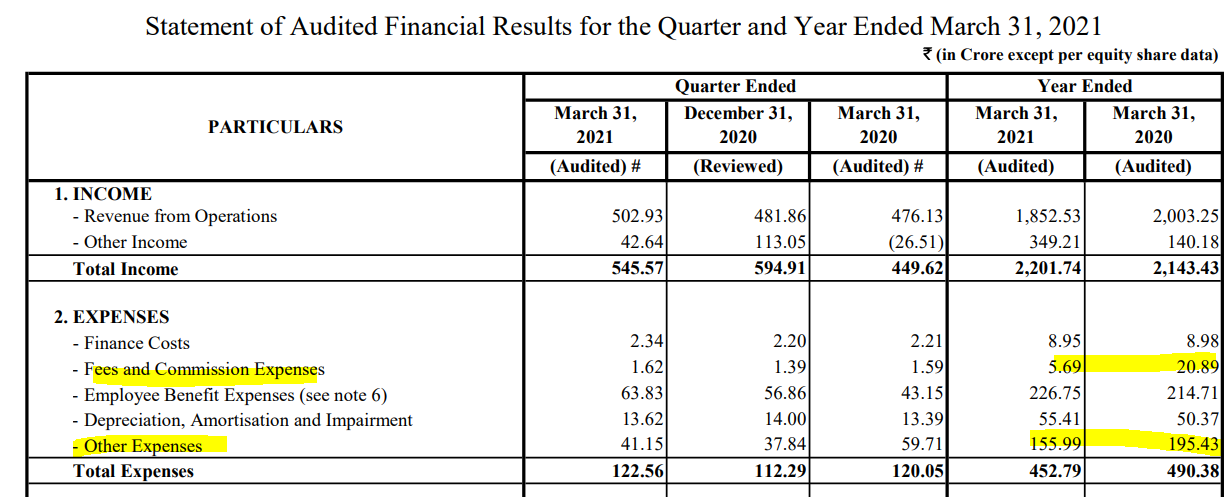

@Dev_S - All the contributing factors to expenses are already lean.

| Other Expenses | FY 20 | |

|---|---|---|

| Item | Cr. | % |

| Advertisement | 27 | 14% |

| Repair & maint. | 26 | 13% |

| Electricity | 5.5 | 3% |

| Comm. | 6.5 | 3% |

| priniting | 12.5 | 6% |

| Legal | 14 | 7% |

| Outsourced Service Costs | 25 | 13% |

| CSR | 21 | 11% |

| Misc. | 24 | 12% |

| Travel | 7 | 4% |

| Subs & memb | 8 | 4% |

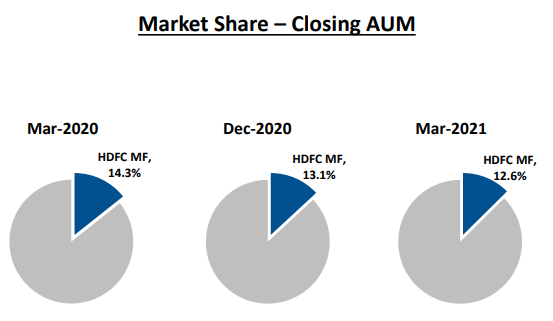

Revenue has to do the heavy lifting. However, reduced commissions has definitely pulled down their market share as shown below: