This stock is a clear example of how calibrated and how accurate the market is when it comes to estimating near term earnings. The stock was trading at elevated PE multiple for almost a year since the near term earnings trend was very attractive at 40% YoY growth but once the low base started normalizing the multiple is back to the more reasonable range of sub 42.

Over the past 2 years I have come to the view that I cannot be better than the market when it comes to estimating near term earnings. The only way I can generate alpha is to either have an edge on insights (this can happen only if I understand the business very well) or through a temperamental edge (this is more behavioral). Or to load up good business when there is a sudden dip in the markets overall (no better example than March 2020, but this becomes obvious only in hindsight).

No easy money in the Indian market any more, information edge no longer works. Within 10 mins of a conference call ending you have messages being forwarded about management commentary and how the near term outlook is likely to be.

Unless the fund managers at mutual funds pull up their socks it is going to get more and more difficult to keep pace with what the index delivers. Over the next 5 years or so MF will get positioned as a retail product with the HNI segment moving into a combination of ETF + AIF/PMS as opposed to MF being the mainstay.

This stock continues to be one of the lowest risk way of playing the financialization theme in India, a 15-18% earnings growth story at 30%+ return ratios and free cash flows combined with a low cost of capital makes for an interesting combination. As is the case with such businesses, the most important thing is to participate without overpaying for the stock.

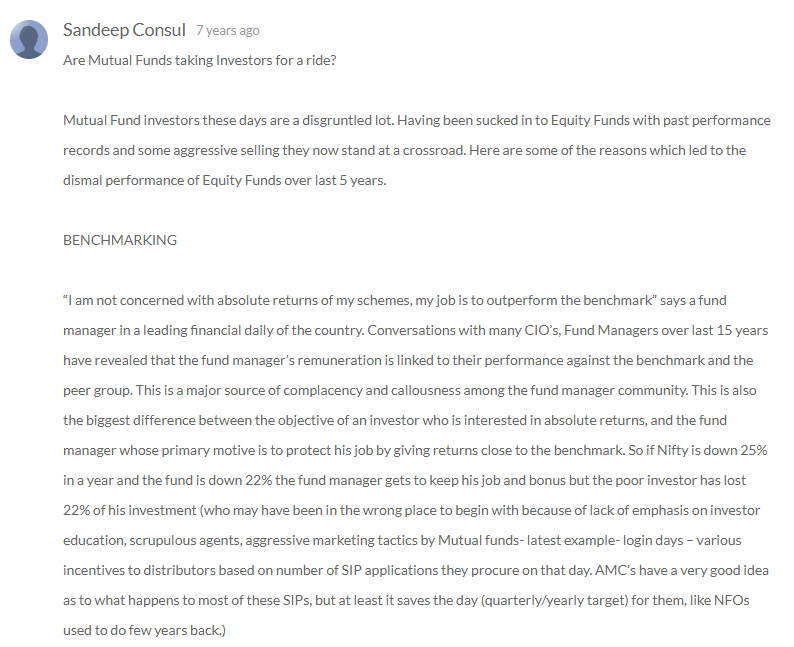

I was checking the past articles about how mutual fund industry fared in previous difficult years.

Apart from the article, there is a very good write-up in comments section by one user Sandeep Consul. It is a long write-up, I am just pasting the first few lines.

Fund managers are basically getting incentive only if they beat index and most fund managers were buying shares of those few heavy weight companies like HDFC Bank, Reliance etc in percentage of their index weightage for most of the new money coming to the fund by default so that they have less uncertainty about their bonus. Safe game. Had the KPI metrics also include beating FD returns an extra perk, they would have been more dynamic. The SEBI reclassification of MFs came only in 2018.

Some good fund houses like Fidelity have tried their hand in penetrating the mutual fund market in India but eventually left the market. So, due to cut throat competition, the expenses would have been more for the new fund houses while penetration. The advantage HDFC AMC has is the distribution edge which helped in keeping mostly predictable flows coming in and HDFC AMC is process driven to keep their expenses under control.

In India, there are some years in equity markets where the returns will be touching the roof like - 2017, so all the SIPs collected before that becomes fruitful. The distributors will showcase the returns of last one year etc conviniently and will add more people. Apart from distributor edge & expense control, what is helping HDFC AMC is the consolidation of MF industry - Morgan Stanley, Goldman Sacchs, Fidelity(taken over by L&T) etc were acquired/merged. L&T Finance itself wants to put their MF business up for sale. I agree as the AUM increases for a particular scheme it is difficult to generate alpha but people like Peter Lynch generated CAGR of 29% return for 13 years. It certainly is an exception though.

As an investor, I wish one such Peter Lynch joins HDFC AMC!

Like @zygo23554 I too feel ETFs + PMS/AIFs are the way forward for asset management companies.

The management in their last concall have also acknowledged the recent underperformance of their equity funds and are looking to churn their portfolio for a more index agnostic kind.

They have also recently appointed Mr. Gopal Agarwal as a senior fund manager for 3 of their flagship fund. Let’s see how that pans out. Let’s hope he can bring a touch of Lynch in the funds.

I’ll just say this for any AMC company in India right now. BlackRock, the largest asset manager in the world with over $7 trillion of AUM has a market cap of $ 90 billion - just under 1.5% of AUM. HDFC AMC is valued at $7 billion when all of India’s mutual fund industry is less than 5% of just Blackrock’s assets - India is a rounding error in global asset markets. Remember also that fee income is going to go to a few basis points on the back of passive / indexing trends as well as digital distribution. Now add to this that HDFC AMC isn’t particularly the best asset manager either.

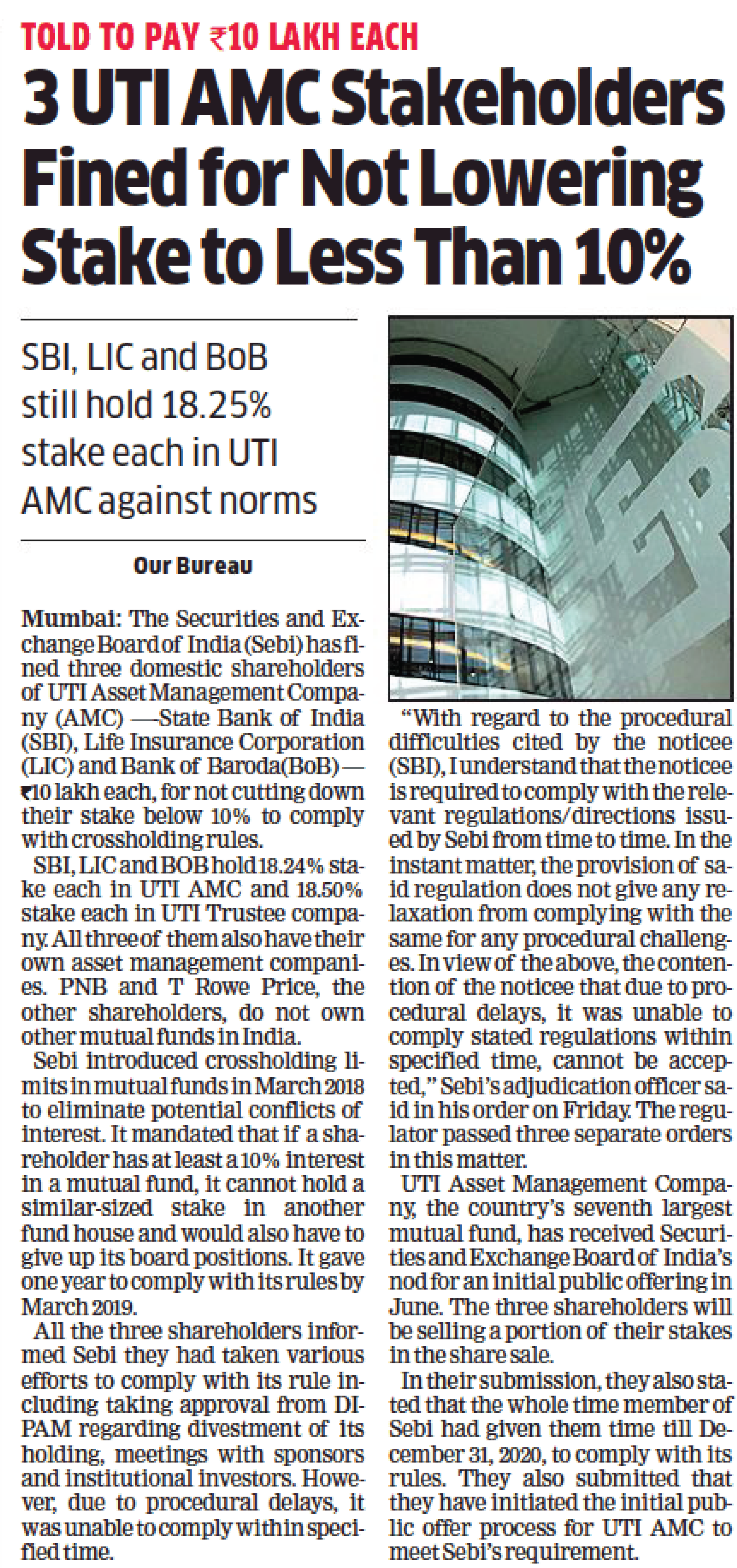

Sebi fines SBI, LIC, Bank of Baroda for violating mutual fund norms

Markets regulator Sebi on Friday imposed a penalty of ₹10 lakh each on three public sector financial institutions – SBI, LIC and Bank of Baroda – for not complying with the mutual fund norms.

Sebi observed that State Bank of India (SBI), Life Insurance Corporation of India (LIC) and Bank of Baroda (BoB) are the sponsors of SBI Mutual Fund, LIC Mutual Fund and Baroda Mutual Fund, respectively, and they also hold more than 10 per cent stake each in these mutual funds.

In addition, LIC, SBI and BoB are also sponsors of UTI AMC and hold more than 10 per cent stake individually in the asset management company (AMC) and trustee company of UTI MF.

This is not in conformity with the requirement of mutual fund regulations, the Securities and Exchange Board of India (Sebi) said in three separate orders.

The regulator amended the mutual fund regulations in March 2018, wherein a shareholder or a sponsor owning at least 10 per cent stake in an AMC is not allowed to have 10 per cent or more stake in another mutual fund house operating in the country

Sebi, in the orders, said the entities have violated the provision of mutual fund norms and are liable for penalty. Accordingly, the regulator has imposed a fine of ₹10 lakh each on them.

I’m very new to this but unable to figure out what exactly is the correlation between AUM and the profit making ability of an AMC (which should derive the market cap of a company).

From Pat Dorsey’s book - “The five rules”, I’ve figured out one thing that one should buy into AMC stocks during a market fall as the AUM shrinks but unable to understand the logic behind this. Can anyone please explain me why an AUM fall should necessarily result in drop in profitability?

Expense ratio is charged based on the NAV which will come down when the market corrects (existing AUM decreases). However, existing investors in these funds have already paid the TER if my understanding is correct. So, what’s the impact on the AMC?

Future Investments into these funds be it lumpsum or monthly will be charged TER on the basis of NAV which is hit but we as mutual fund investors don’t buy 50/100 units of a fund, it’s ₹5k/₹10k which means we will still pay the same TER (in terms of rupees) as we would pick up more units during a market fall. Here too, theoretically (provided it’s right), AMC would still earn the same amount of money

PS - There’s a possibility that many investors pull out during a crash and all that but that is not a direct impact because of fall in AUM. I would consider this as a qualitative aspect which is based on an investor’s behaviour

Theoretically, if AUM increases with markets at same level in few months or rather if AUM over a period of time maybe an year has grown at decent cagr then month on month falls is only an opportunity to invest.

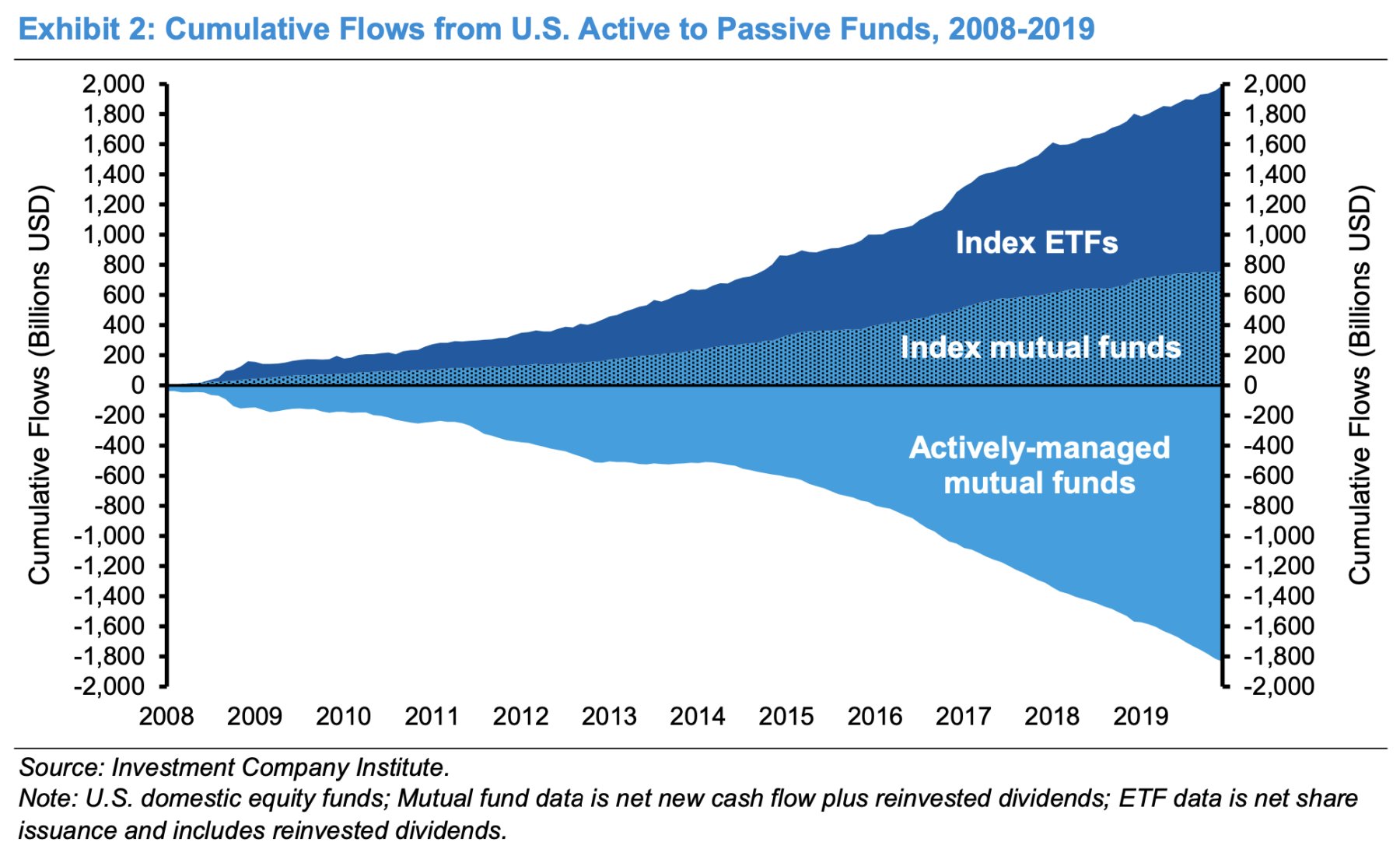

The real threat here is passive investing/index investing/low margin ETFs and investors moving to stocks directly. How AMCs have coped with that in US and what happened to their stocks in US, where passive investing has been the trend since sometime now, will give us some insight into long term prospects of AMCs in India. India is still behind in passive curve but eventually it will come strongly.

Came across this article today and haven’t been able to reconcile this with what is generally happening across the equity AMC industry. On one side there has been increased noise over underperformance of active funds and how they have underperformed their respective indices while index funds with sub-0.5% TERs have been becoming more and more popular among investors (esp. people who invest into direct mutual funds)

Keeping these in mind, increasing the expense ratio for direct schemes appears to be a contrarian move and a risky one at that too. What could be the reason for this increase across MFs almost simultaneously? Does one see a broader trend playing out which I, in all my naievete, have missed out here?

It could be an indication that they are losing business and hence have decided to increase their charges to make up for the shortfall.

Not everyone has the time, inclination or the capacity to invest in stocks directly. In such a scenario, this seems to be like a good move by the mutual funds (not for their customers)

New hire as Sr fund mgr - responding to dynamics, not in status quo

ETF launches - new NFO - responsive to market

Last 30+ days- most days delivery % higher than 70 - accumulation

Relative HDFC schemes performance for past 1 & 3 mo in upper quartile ( e.g HDFC top 100 as top 5 and 10 in 70 large cap scheme, HDFC midcap at 10 in 43 schemes and so on…) - this will be factored in new investments

AUM getting better with every month and it is a broad based rally - mix may evolve with higher debt and etf part vs earlier years and may have some impact on income mix but most likely offset by lower costs - 90%+ Digital channel

SIP flow has been resilient - HDFC has largest cut and point 4 will support going further

Debt fund inflows are healthy for trusted brands - esp HDFC

Industry consolidation- by end of FY 21 - how many players and schemes wind up - likely and to benefit bigger guys.

After consolidating , Technically a bottom is formed with and 5,10,20 DMA turning bullish, expect sizable buying to come once 50 DMA is taken out

TER increase is by all fund houses - they know the game and timing and per some scuttlebutt- inflows are healthy

Already had characteristics of compounder to play financialization theme, short term head winds seem to be subsiding too…

The price increase by even the MF company which showing good scheme performance. Eg Mirae asset. Also it shows that it’s will get toucher day by day for small company to compete with bigger Co. I believe in future many small fishes will be taken over by big fish… L&T finance, IDBI bank already put there MF business for sale…

The article fails to mention that exit WAS available by selling in the secondary market. Though probably at a discount (I had bought some in the secondary market).

Also though equities are not for 3 years, one can always reinvest the proceeds received on maturity.