I am keen to know how is this working

As I understand Zee NCDs are overdue ,which has been subscribed to by these FMPs.

If as of 31 March a FMP had exposure of Rs100 face value plus Rs2 interest and if as of today the interest has become Rs2.5 , is the HDFC AMC buying at Rs102.5 OR are these NCDs traded and are being bought at MP?

Not all NCDs are overdue, only some have passed their maturity date. They haven’t clarified how exactly they would value, but my guess is they would take the accrued interest upto the date of transfer into consideration while doing the transfer i.e. Rs.102.5 in your example.

No, it doesn’t require shareholder’s approval.

The FMP investors are not complaining. They are happy.

I believe even investors in HDFC AMC are not complaining. They know this will help increase AUM over longer term.

People who are neither investors in HDFC AMC nor FMP holders are complaining. I don’t think HDFC AMC is bothered about this set of individuals.

If you are running a business you will use your competitive strengths (in this case a strong balance) to get out of adverse situations.

16 Likes

Not all shareholders are happy. This complicates how to value the stock as we as shareholders do not know the extent of their exposure to such troubled bonds and whether they will bail out every time. If they bail out, will they do it at a hair cut or full price? This looks like a bad precedent complicating a good and simple business which could probably even bring losses to one business which do not get in to losses.

1 Like

Agree, it complicates things. How do you relate it to life insurance companies? Their ULIPs or market linked products carry same risk? Is there any such case for life insurers in past? Thanks

I don’t think we can relate this to life insurance companies. First both shareholders and purchasers of insurance products knows the risk they are getting into before the purchase which is not the case here. Then risk and return lies with the purchaser of insurance product. But here’s the return goes to the FMP purchaser but the risk is borne by the shareholders which is unfair.

1 Like

Does anyone know the composition of customer(unit holder) category for these FMPs? Are they mainly corporates and HNIs?

While this incident looks like a bad precedent, it makes the task of valuation harder. However, fearing that AMC businesses will become loss-making ones is probably an extreme position. One must trust capitalism that any action that appears to be self-harming would necessarily be done with an eye on future profit, so never underestimate corporate greed!

@Investor_No_1 rings out an excellent point. It has always been my view that Insurance products carry the same risk as the AMC did in this instance, as Insurance is all about underwriting risk! Yes, while policy holders and share holders are expected to understand that Insurance is about being in business of risk, it appears to my simple mind that share holders probably do not (to be accurate, cannot) estimate the risks that the Insurance companies have taken on, on the premiums collected. Perhaps its somewhere deeply embedded in the Embedded Value  .

.

In case of AMCs, the company battles against regulators (expense ratio, disclosure, ethics etc) and peers (performance), and companies (one large bet can take you down several notches). Insurance companies have the same battles and addition of Act of God, or risk of unknown.

You can read a bit more about this aspect of Insurance: https://www.cairn.info/revue-management-et-avenir-2009-7-page-225.htm#

9 Likes

Sir, thanks…what I understand is underwriting risks are related to nonparticipating products that is protection business and also to some extent in protection part of participating that is ULIP kind of business. The risk I was talking about was purely investment risk of the float which is what AMC also carries…only positive, and I think a big one, for insurance firms is that they make money from the protection part of the float while in case of AMC, the complete float belongs to the unit holders. Views welcome! Thnx

As per latest annual report of HDFC AMC they have 90.3 lakh accounts (folios).

So, as per above calculation, HDFC AMC should be worth around Rs 28219 Cr. Presently market cap is 39000 crore something.

Hi

Have started reading the annual report and was also looking at some AMFI data (shared in a different form earlier by zygo).

Raw sheet is available on google sheet here. I intend to keep adding more data points into this in multiple tabs.

Growth this FY - I do not know the reasons for SBI. If somebody does please share.

| FY19: Q1 to Q4 AUM | |

|---|---|

| SBI MF | 22% |

| HDFC AMC | 12% |

| ICICI Pru | 3% |

| ABSL | -1% |

| Reliance MF | -3% |

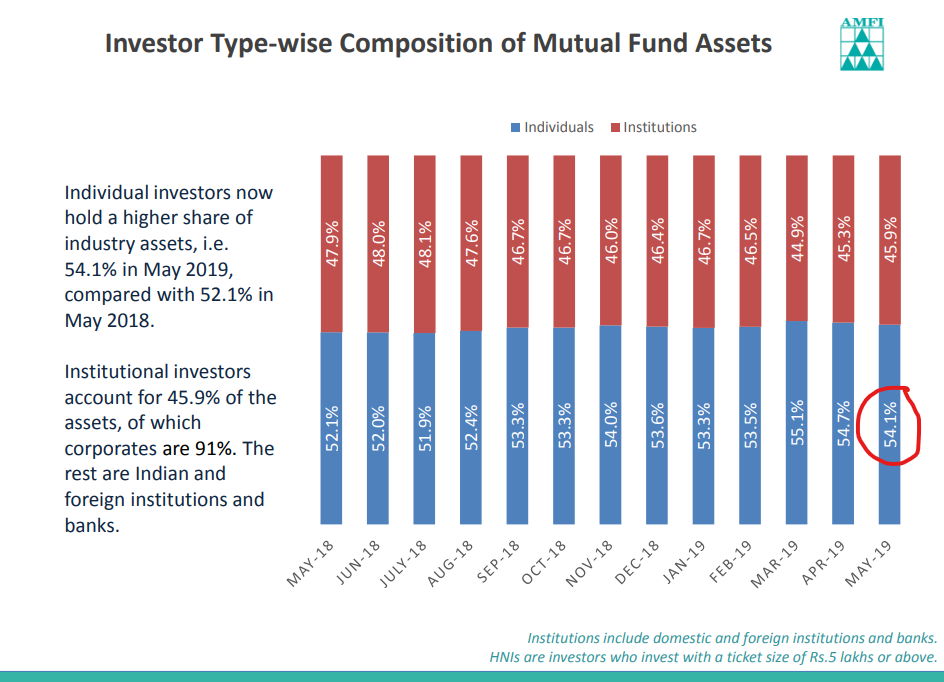

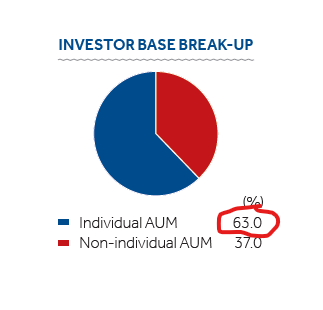

On the individual side. HDFC AMC seems to be pretty strong. They have 63% individual assets compared to 54% of industry average.

In addition the electronic txn share for HDFC amc is 67% in FY19 with a 42% cagr from FY15.

I think this individual focus via electronic means could be a key differentiation in the future. Will try to find out competition figures for the same.

Rgds

disc: invested since ipo. not a stock recommendation.

9 Likes

I think the AUM growth of SBI MF is because they are getting EPFO money to manage.

2 Likes

AMFI targeting 5 fold increase in MF AUM in five years

I know government projection are not good source of investment thesis but it’s shows some possibilities

Thanks

Ashit

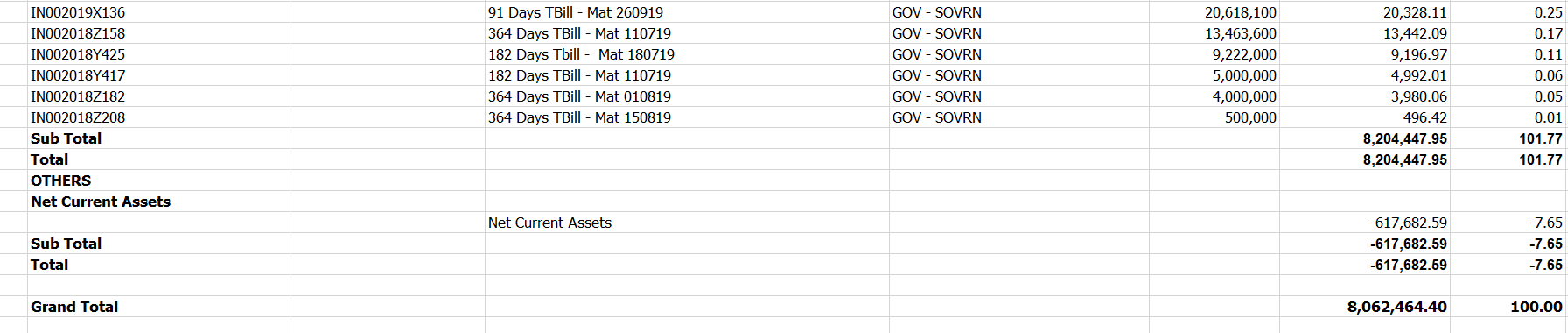

In the June monthly portfolio of HDFC AMC, for the HDFC LIQUID FUND, I see the below. Can you anyone help me understand what net current asset mean in here and what does it mean to have a negative value? The same for the month of May was a positive number

(Source: https://www.hdfcfund.com/statutory-disclosure/monthly-portfolio)

June 2019:

May 2019:

1 Like

Negative Current Assets would mean the fund has borrowed from overnight / call money market. The fund may do this if it is fully invested and there are redemptions to meet. If the invested assets are earning more than the overnight rate, the fund may find it beneficial to borrow and pay the investors instead of liquidating its assets. Doing this to a small extent is fine, to meet short term inflow / outflow mismatches.

5 Likes

Thanks much to @zygo23554 for his contribution. Helps us to understand the industry immensely. Posting some questions / thoughts below.

- Tried to understand how much cyclical this industry is really. One very important difference between the past and future cycles is the share of equity funds in the industry. As equity funds share increase, the industry is going to get more and more cyclical. So directly comparing with the past cycle may give misleading insights. Below is an exercise to understand how cyclical the market in the next crash.

Data is collected from AMFI:

https://www.amfiindia.com/research-information/aum-data/age-wise-folio-data

For FY20, I assumed that there is a drop in Equity AUM by 40% and Non-Equity AUM by 10% which lead to 25% drop in total AUM.

I believe this drop was smaller in 2008 due to lower proportion of proportion of Equity.

| Financial Year | Equity AUM | Equity YoY | Total AUM | Total YoY | Equity Share | |

|---|---|---|---|---|---|---|

| 2009 | 120027 | 417024 | 0.2878179673 | |||

| 2010 | 214353 | 0.7858731785 | 614547 | 0.4736489986 | 0.3487983832 | |

| 2011 | 216936 | 0.01205021623 | 596976 | -0.028591792 | 0.3633914931 | |

| 2012 | 203140 | -0.06359479293 | 587659 | -0.01560699258 | 0.3456766594 | |

| 2013 | 193730 | -0.04632273309 | 702493 | 0.1954092424 | 0.2757749899 | |

| 2014 | 213396 | 0.1015124142 | 825243 | 0.1747348372 | 0.258585653 | |

| 2015 | 380072 | 0.7810643124 | 1082757 | 0.31204627 | 0.3510224362 | |

| 2016 | 441009 | 0.160330148 | 1232823 | 0.1385961947 | 0.3577228848 | |

| 2017 | 672699 | 0.525363428 | 1754619 | 0.4232529731 | 0.3833875046 | |

| 2018 | 993344 | 0.4766544918 | 2136035 | 0.2173782456 | 0.4650410691 | |

| 2019 | 1205640 | 0.2137185104 | 2379584 | 0.1140191991 | 0.5066599876 | |

| 2020* | 723384 | -0.4 | 1779933.6 | -0.2519979963 | 0.4064106661 |

Now another important point is the margins are higher in Equity AUM business.

Blended EBITDA / AUM is 35-40 bps with 50% AUM from Equity and 50% from remaining.

In a conf call, management mentioned that Equity AUM’s margins are double of non-Equity AUM’s margins => Equity AUM has around 50 bps EBITDA margin while remaining has 25 bps.

So cyclicality impact on profitability is much higher than cyclicality impact on AUM.

Cyclicality impact on AUM is already demonstrated above. Lets try to do the same for profits now.

| Equity | Non-Equity | Total / Blended | ||

|---|---|---|---|---|

| AUM | 50 | 50 | 100 | |

| EBITDA / AUM | 0.50% | 0.25% | 0.38% | |

| Profits | 0.25 | 0.125 | 0.375 | |

| AUM (60% Eq, 90% Debt) | 30 | 45 | 75 | |

| Profits (60% Eq, 90% Debt) | 0.15 | 0.1125 | 0.2625 |

Assuming 100 units of AUM with 50 in Equities and 50 in Debt / Liquid gives profits of 0.375 units.

Now 40% fall in Equities and 10% fall in Debt / Liquid would give you 25% drop in total AUM. However, the fall in profits is higher by 30% as margins are higher in equity business. The above excel calculations help understand that. Ideally, the margins will also drop due to fixed costs. So the impact would be even higher. I assumed same margins for simplicity.

I think in the long run, equity share of total AUM will move towards 60+% as individual investors put 70+% of their money in equity funds. This implies cycles are going to get even bigger going forward. One can infer individual investor’s AUM composition here: https://www.amfiindia.com/Themes/Theme1/downloads/home/Individual-Investor-May-2019.pdf

@Yogesh_s bhai, where could you get the AUM data for years upto 2008? I could get Equity AUM and Total AUM only from 2009 through AMFI.

-

Why did the company do IPO? It always had a lot of cash over the past five years. I don’t think there was a need. What was going through the management’s head when they decided to go for the IPO?

-

Are we blindfolded with the card that HDFC is always good at corporate governance / risk management? I have never looked up a financial company before, so I may be wrong in terms of expectations but there are already couple of incidents in HDFC AMC over the last one year.

a) IPO share allotment preference given to distributors

b) Exposure to IL&FS group & Loans to Essel group

c) IPO timed before the SEBI’s TER rule (although on ground reality, it is hurting the distributors more)

Discl: No holdings

11 Likes