HBL AGM 2025 highlights :

I got an opportunity to attend the agm and participate in the QnA , please find the Partial notes from AGM.

Highlights from Chairman Commentary:

The cover of our last annual report had shown that the sales for FY25 will be flat, that there will be no growth, and in fact, there was a mild decline, but that was still close to what we expected. And the reason, of course, is the Kavach orders. We expected some Kavach orders to begin, and every month’s delay in the receipt of those orders will lead to a delay in our deliveries. The cover also showed a steep increase in FY26, and the surprise now is that the increase will be even more than expected. Again, the primary reason is the drought of our orders has now become a flood, and this is typical of these kinds of customers we have.

The other point about the annual report cover this year is I used the words “next orbit”. Somebody wrote to us saying, “What does orbit mean?”. I thought it is something everybody understands, but what I meant was that if you look at the last five years, which we have summarized for you in the MDA, you will notice that the preceding three years we were stuck around less than around 1,000 crores to 1,500 crores. In the previous two years, we got stuck around 2,000 crores, but from now on, I think it will not be lower than 3,000 crores, and therefore it’s the next orbit. We are budgeting this year—budgeting is the word, I’m not forecasting, we are careful not to say it is management guidance—but we are budgeting for 3,000 crores in sales of this fiscal year.

Because of the publicity given to the American tariff decisions, some of you may be wondering whether it has any impact on our sales. No, there will be no impact because our budgeted sales are only 50 crores, and all of it is not lost. People are still saying that there may be an agreement and something will settle down. But our customers are those who cannot easily switch from one to the other just because of an increase in price. So they will negotiate, we have to compromise, and they’ll also budget something, and if the tariff remains in the future, they will plan for this on their own.

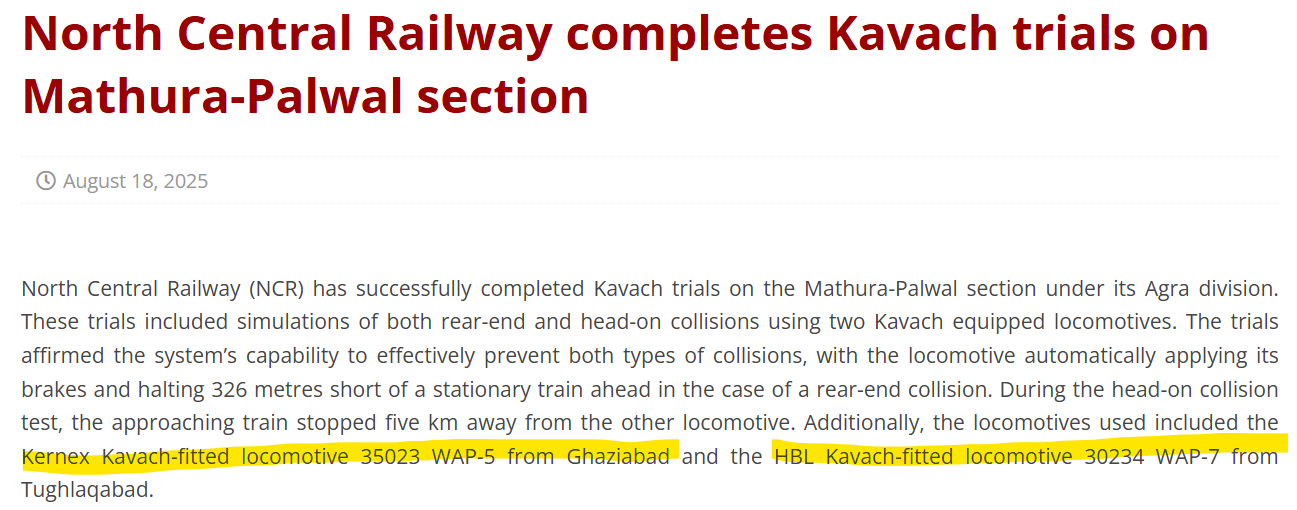

The big story of the year, of course, is Kavach. As explained in the management discussion and analysis, the business in the next two fiscal years should be almost as good, definitely, and perhaps better in the next year than this year. So there could be a decline in FY28, and how much depends upon many unknowns. At this point of time, out of five companies to whom orders were given by the railway ministry, only two companies are qualified. The other three are yet seeking to get qualified. Nobody knows when that will happen. And we had a lead on our competitor by about, I think, 8 to 9 weeks. So I see quite clearly that Kavach is going to continue to be important. By FY28, even if Kavach falls a little bit, I don’t see any reason to worry because I expect the growth in sales to continue due to two reasons. One, the TMS, which the railways have been too busy to pursue, will now become… they’ll have time. And more than that, the sales of electronic fuses for ammunition, on which the company has been working for 20 years. There have been a lot of favourable developments and enormous progress made by our team. But all told, we are going to enter a niche market that is as sound and, in investor language, they call it a moat. I like that word. This is a moat that not even three people can cross.

So overall, the visibility for the next three years exists, and beyond that, you have to take my word for it because a lot of developments I don’t want to talk about unless there is something firm on the ground. And the MDA had said that we’re hoping to get 4,000 crores by FY30. As of today, that still seems a reasonable number. That is enough about the current business prospects.

Highlights from Chairman response of QnA:

As of today, we are the only company in the country that makes batteries for fuses. And let me assure you that in the whole world, there may be five or maybe three, four countries with five or six factories. That’s it. This is important to keep in mind how we got into it, and then we tried to look at the rest of it and found that it is also going to take time. We started working on fuses in 2005—for 20 years.

So, recent RFI, and why the fuse business has suddenly grown. India wakes up in a crisis. Everybody has now realized that this operation, whatever extraterritorial activities it may have, highlighted the threat of drones. You can’t launch a missile at a drone, nor rely upon a soldier firing a machine gun at a drone. The army had an air defence wing with a senior lieutenant general in charge, and there was heavy import. The foreign supplier of the fuse stopped supplies. The army then asked, “Where is HBL?” HBL had been aware of this device for a long time, but earlier there was no interest. Then came urgent requests: “Can you give me in three months? Can you give me in six months?” HBL replied that it would take time since such items are not readily available.

One of the most amazing stories is the grenades. When you throw a grenade is it has to take a few seconds before it lands and explodes. We had this attack on the Taj Mahal Hotel 26/11. Soldiers from a special forces that were asked to get into the hotel and drive the terrorists out—two died. One died because when he threw the grenade at the terrorist in the corridor, it didn’t explode on time. That fellow threw it back. It exploded near the person who threw it. Second one died because it exploded too early. Now, why this happened? Because they were using mechanical fuses. So the army wakes up again, and by this time the Defence R&D organization, ARDE, was very helpful to us in getting us introduced to these customers because otherwise, they’re not authorized to talk. So we have developed fuses for grenades, and we are certified to produce grenades. We have got orders for grenades, so we are using our fuses in these grenades. I think I’ve answered basic questions on the fuses. And why I’m saying it will be '28 is if we are at this stage today and I’m not going to jump and produce more than I can safely deliver, I’m taking the next year for that ramp-up period. The recent RFIs were all connected with air defence—the 23, the 30, the 40mm.

This stock tested my patience ( and probably other investors too) over last 2 years. Going by management commentary of 3000 cr top line we are looking at 40-50% growth this year.

Ps : Holding and no recent transactions.