Railtel new comer in kavach

7000cr tender on 19th sep

Railtel new comer in kavach

7000cr tender on 19th sep

RailTel w/Quadrant Future Tek

RailTel Corporation of India Limited signed a memorandum of understanding (MoU) with Quadrant Future Tek Limited for works related to KAVACH installation on May 1, 2024.

In the process of understanding the new entrants, I discovered that Quadrant Future Tek Limited has a DHRP on their website. They are in the works to list on the exchanges. Their DRHP is dated June 2, 2024. I have concentrated only on Kavach related notes in their DHRP.

About the company: Quadrant Future Tek Limited

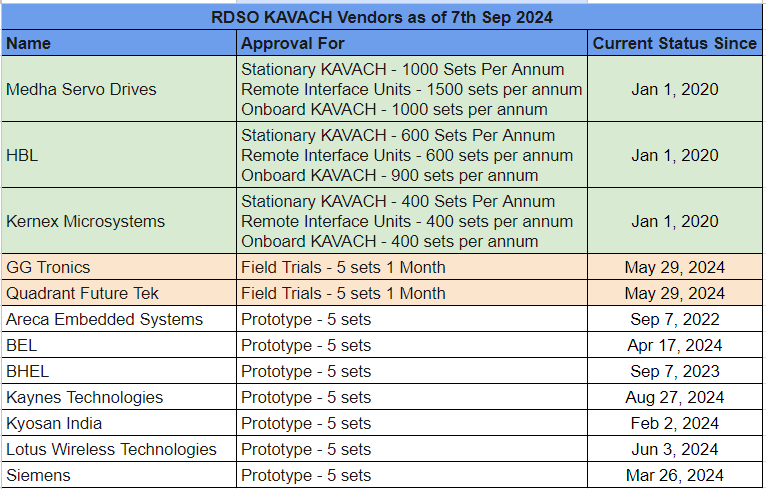

I downloaded the latest list of all RDSO approved vendors for KAVACH. I was surprised to see that all vendors, including Medha, HBL and Kernex, are listed as “developmental” vendors and not “approved” vendors.

Among developmental vendors there are 3 different levels of approval:

The actual PDF downloaded from IREPS website is attached.

KAVACH Vendor Directory 07-Sep-2024.pdf (2.6 MB). I have extracted and distilled the information in the table below.

So as you can see, not only are there 3 different levels of approval, the final approval also has a limit on capacity. Apparently RDSO also assesses supply capacity per annum. In one of the interviews the Railways Minister Ashwini Vaishnav also talked about awarding contracts based on manufacturing capacity. So now it all makes sense.

I am not sure how long does the process from field trial to final approval take. GG Tronics and Quadrant received the go ahead for field trials on 29th May 2024. As of today they have approval only for 5 sets of KAVACH (which means KAVACH for 5 station side equipments, 5 trackside and 5 onboard locomotives). So it appears to me that these 2 companies are not competing in the currently released tenders. The other 7 companies - big names like BEL, BHEL, Siemens etc. are not even eligible. I may be wrong, someone needs to cross check.

Also, as I mentioned before, everyone is a “developmental” vendor now. No one is an “approved” vendor yet. This means the KAVACH systems will undergo further changes. Currently it is at version 4.0 (previous was version 3.2). So it looks like the whoever is on the latest version will always have an advantage as far as eligibility for tenders is concerned. What I mean to say is - lets say a company has approval for ver 3.2 and wants to go for ver 4.0, then there will be some time lag due to RDSO’s testing and evaluation process. The tenders released are always for the latest version and if a new tender arrives before the company has received the approval for the latest version then they will not be eligible for the tender.

What would be the reason behind RailTel signing the “exclusive” MoU with Quadrant? I understand the MoU part, but not the “exclusive” part. Quadrant has a lot to gain out of an exclusive tie up with RailTel, but I am not sure if RailTel has. Logically speaking RailTel should be open to working with any RDSO approved KAVACH vendor. Anyways a MoU is not a binding legal agreement, so I would not read too much into it. The timing is also suspicious, just 1 month before they filed the DHRP.

Thank you @ganeshrpl and @fabregas for detailed inputs.

Yesterday I scanned through AR of Kernex. Have also been reading on Kavach opportunity and challenges involved in various magazines and articles. From what I could understand, since 4.0 is a big upgrade over 3.2, development, testing and migration, and certification of all vendors for 4.0 is taking a lot of time. There are multiple departments in railways that are involved which is adding to a lot of friction, in-fighting and overhead.

Also, original plan was to slow on roll-out but with recent accidents there is lot of pressure on govt to get this rolled out across majority of the rail network. However since Railways worked with smaller companies for developing the technology, the available capacity is very limited against the massive demand. Hence the push to get more vendor partners onboarded…but given the complexity of the technology and stringent railway certification requirements, this is going to take a lot of time.

So while the demand is huge, awarding tenders, announcing results, deployment of the technology, testing and railway acceptance is going to take a lot of time. No instant miracles here except for order book wins that might aid the companies share momentum price in bull run. Given the way railway operates, most of these vendors will have long implementation timelines, very long WC cycle, negative cashflows and lumpy payments.

Just my 2 cents.

Disclaimer: invested in HBL and Kernex

Have started reading through latest AR for HBL. On page no. 8, management has sort of tried to temper expectations of investors by giving a very cautious guidance as below:

POSSIBILITIES FOR THE NEXT FOUR YEARS

1 9. 69

EBITDA MARGIN (%)

When one gets the urge to predict the future, the wise man calms down

until the urge goes away.

With this caveat, HBL sees the near future as follows:

In-spite of management projecting flatish topline for FY25, stock price is still holding. Ideally this information should be factored in the price by now, though if there is a severe correction in the market, what would happen to an expensive stock is anyone’s guess.

While the management has been conservative and delivered above their projections in the recent past, I am unable to understand the rationale behind two things mentioned in the AR-

For EV trucks, HBL wants to go on their own instead of tying up with any existing OEM. Not sure how this will pan out - B2C success heavily depends on distribution/dealer network and service capabilities. Not sure how HBL will be successful here.

They vaguely mentioned about private equity being a new business avenue for them . I seriously hope HBL does not get in to this. Engineering and PE are two different things altogether.

Disc- Significant holding from much lower levels

The key takeaways for me from this year’s Annual Report are as follows:

This is very significant since HBL is the only company that makes everything in house from battery cells to battery packs in India as of now and cna have customised solution for various use cases. I am not sure about volumes here but onboarding Siemens for LIB is very significant as it shows how HBL can be a key partner in areas where China is not an option for batteries.

This is first time HBL has confirmed making newer EV trucks. The story until now was always retrofit. HBL owns the complete technology here from battery/controlller/charging infra/motors etc. Lookin at the current set of alternatives in the market I don’t see any competitor which has complete in house technology. How this will play out is very difficult to predict since it requires a lot of things to fall into place including financing + charging infra but having known HBL they will put their best foot fwd and not come with a half baked solution. They have also gained experience in setting up charging infrastructure with their subsidiary TTL ELECTRIC FUEL PVT LTD (EFL).

Going by the above HBL plans to offer a far more comprehensive EV solution than just selling EV trucks but limiting it for the area usage to a few highways in the beginning and later expanding the network.

Clearly acknowledging that it is difficult to compete with the Chinese EV battery ecosystem unless there is Government support. HBL has always been clear it doesn’t want to get into businesses which require govt subsidiy or duty support.

HBL over last 10 years have made two ‘PE type investments’ one was Igarshi and other more recently Tonbo. Even though both of these have been excellent investments both in terms of valuations where they were bought and the exit/visibiity that they have I hope that these ‘PE type investments’ remain far and few. I would have preferred if the promoters did it in their own account.

Looks like the company will move towards some kind of professional management model with key promoters ensuring business continuity.

I have similar concerns on the decision to become OEM for EV trucks. On one side they are saying they don’t want to get into “capex heavy” areas and on the other side this decision to become OEM will ensure they have to do heavy capex. Besides I don’t know how much margin they will make in this business, and how they will compensate for the lack of previous experience of running such a business. Partnering with one of the existing OEM would have been a less risky strategy along with faster time to market.

Without conference calls, hard to get insights into the reason for this management decision.

HBL AGM 2024 snippets.

Few points from Hbl AGM

Management has given guidance of 30% in FY 26 growth over FY 25 numbers but if forced to reveal, they will surpass this guidance.

No plan to do anything with Tonbo investment. It should list in early 2027. Hopefully will reap benefits then;

In terms of capacities, while Hbl can scale whenever it wants, currently it can do 2000 km/year of TCAS on tracks and 3000 loco/year. TCAS is a huge opportunity;

Hbl is the only company which has completely indigenous TCAS system;

Lot of scope of batteries (other than lead). Eg., Siemens wants Hbl to manufacture Lithium batteries for them. Traction in defence batteries remains strong.

Kavack 4.0 and 3.2 are not inter operable…Railways have to think about that; I got a sense that the recently tested Kavach 4.0 in presence of railway minister was HBL product.

Demand is huge but execution is slow because of lack of trained officers;

TMS will grow slowly;

Mgmt is nurturing high hopes on EV truck with in-house Electric Drive Train. Confident of sharing a prototype in January 2025 and production form Oct-Nov 2025;

Co has no plans to become big mass producer of trucks but a niche player producing…say 1000 trucks a year at a price of Rs 1 cr/truck (may not be immediately but eventually) with good margins. Thus WC will not be an issue;

Retrofitting old trucks with its E Drive train is not feasible cause trucks are old and run down;

Regarding defence products, co wants to focus on exports and not so much on indian defence. There is huge demand for fuses in variety of products.

Managment has committed to think about increasing dividend payout ratio in view of expected higher profits over the years.

Kernex FY24 AGM Highlights

HBL Q2 FY 25 results out. Flat topline, margin improvement helps in improving EBIDTA Y-on-Y.

Industrial battery and Defence and Aviation battery divisions have performed well.

Kavach is yet to fire fully. Next awaited trigger would be allotment of Kavach orders based on August tenders floated.

Received following brief from a friend yesterday on HBL results.

HBL Power 2QFY25 higher profitability despite lower sales

• HBL Power reported revenue of Rs5.2bn, down 6% YoY.

o Revenue of Industrial batteries grew 3% YoY to Rs3.7bn, Defence batteries grew 35% YoY Rs346mn while Electronics declined by 24% YoY to Rs1.08bn (due to lower sales from Kavach).

• EBITDA grew 8% YoY to 1.08bn, while margin expanded by 272bp to 20.8%.

Marign expansion seen in all segments.

• PAT came in at Rs871mn, up 29% YoY, led by higher other income and lower taxes.

• Stock trades at 47x TTM earnings

disc: Invested.

My one-pager presentation on Alphaideas 2020 - 16-Nov-24.

DISCLOSURE:

I have a personal holding in the stock. I have the stock in my PMS.

This is the 10000 loco tender around 7000-7500 cr going by the current estimates. Tender finalized status means we should be hearing allocation and order award from the companies soon.

Source:

Correct.

GG Tronics has today announced that they have received Rs. 500-600 cr orders for Kavach with execution of 1 year. The scope of the order comprises Supply, Installation, Testing, and Commissioning of Onboard KAVACH equipment as per RDSO specifications including annual maintenance for 11 years. The Supply scope also includes complete wiring, harnessing, cabling, and connection with Loco KAVACH system.

Source

CG Power announcement: https://www.bseindia.com/xml-data/corpfiling/AttachLive/d0f6b04f-8b51-4292-8fb9-4baa3c2cb5e1.pdf

Next phase of Kavach implementation is planned as under:-

Project for equipping 10,000 Locomotives has been finalized.

Bids for track side Works of Kavach for approximately 15000 RKm have been invited, out of which Bids for about 9000Rkm have been opened. It covers all GQ, GD, HDN and Identified sections of Indian Railways.

The cost for provision of Track Side including Station equipment of Kavach is approximately Rs. 50 Lakhs/Km and cost for provision of Kavach equipment on locomotives is approximately Rs. 80 Lakh/Loco

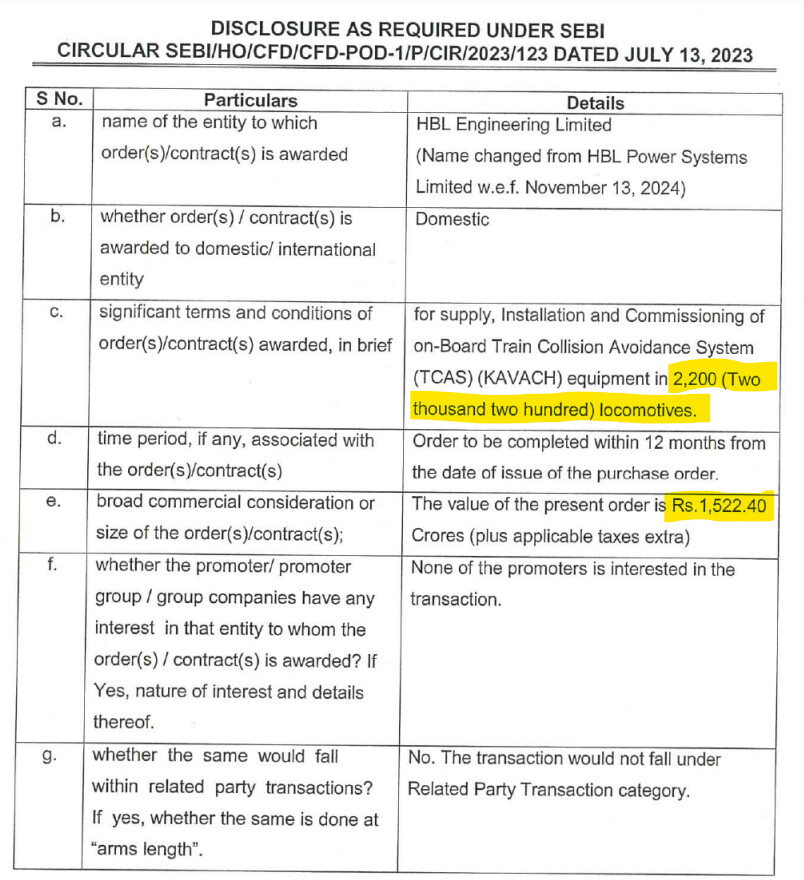

GG Tronics received this order from Chittaranjan Locomotive Works. This is the 10,000 locomotives onboard KAVACH tender. In the tender document they have mentioned a 80:20 split between approved and developmental vendors. As we all know that Medha, HBL and Kernex are the 3 approved vendors whereas GGTronics and Quadrant Future Tek are the 2 developmental vendors as of today. All other (incl. Siemens, BEL, BHEL etc) are in the prototype stage and not eligible for this tender.

Assuming that 20% of the 10k locomotives, which is 2000, are split equally between GGTronics and Quadrant - it suggests that GGTronics will receive a revenue of 500-600 Cr for 1000 locos. Looks like there was an intense competitive bidding and the pricing of loco KAVACH has come down to Rs 50-60 lakh (as compared to earlier estimate of Rs 80 lakh given by the Railways Minister). This is an assumption. We will have to wait for an official confirmation.

As far as the remaining 80% share is concerned (8000 locos), the tender document mentions that the the entire tender may be awared to the L1 bidder or if the L2 & L3 bidder agree to match the L1 price then the Railways reserves the right to split the tender among all the vendors who are willing to match the L1 price.

As of the time of posting this, there is no official announcement of award of either HBL or Kernex, the 2 approved KAVACH vendors who are listed on stock exchanges.

Dear Rokrdude - It is good news for all KAVACH manufacturers.

In listed space we are having KERNEX, HBL, CG Power, Railtel…

Concord Control is another listed company which has 26% stake in progota. This progota has conducted some trails on KAVACH. They are in final stages for getting approvals from RDSO.

Concord also planning to increase their stake in this company.

Holding: HBL & Concord Control

With thanks

Kernex has received an order for Rs 2041 Cr. This is for the 10k locomotives tender, out of which Kernex has bagged the order for 2500 sets. This comes out to Rs 81 lakh per set. https://www.bseindia.com/xml-data/corpfiling/AttachLive/e47780b8-1e11-4a3e-958d-07450cf2cb00.pdf

So out of the 10k sets, 2k were reserved for developmental vendors. Of the balance 8k, Kernex has bagged 2.5k. This leaves us with 5.5k on the table for Medha and HBL.

My guess is that Medha will get 3k and HBL will get 2.5k. During the AGM the MD had mentioned that they are expecting an order for 3k sets for this tender. Lets see. Fingers crossed ![]()