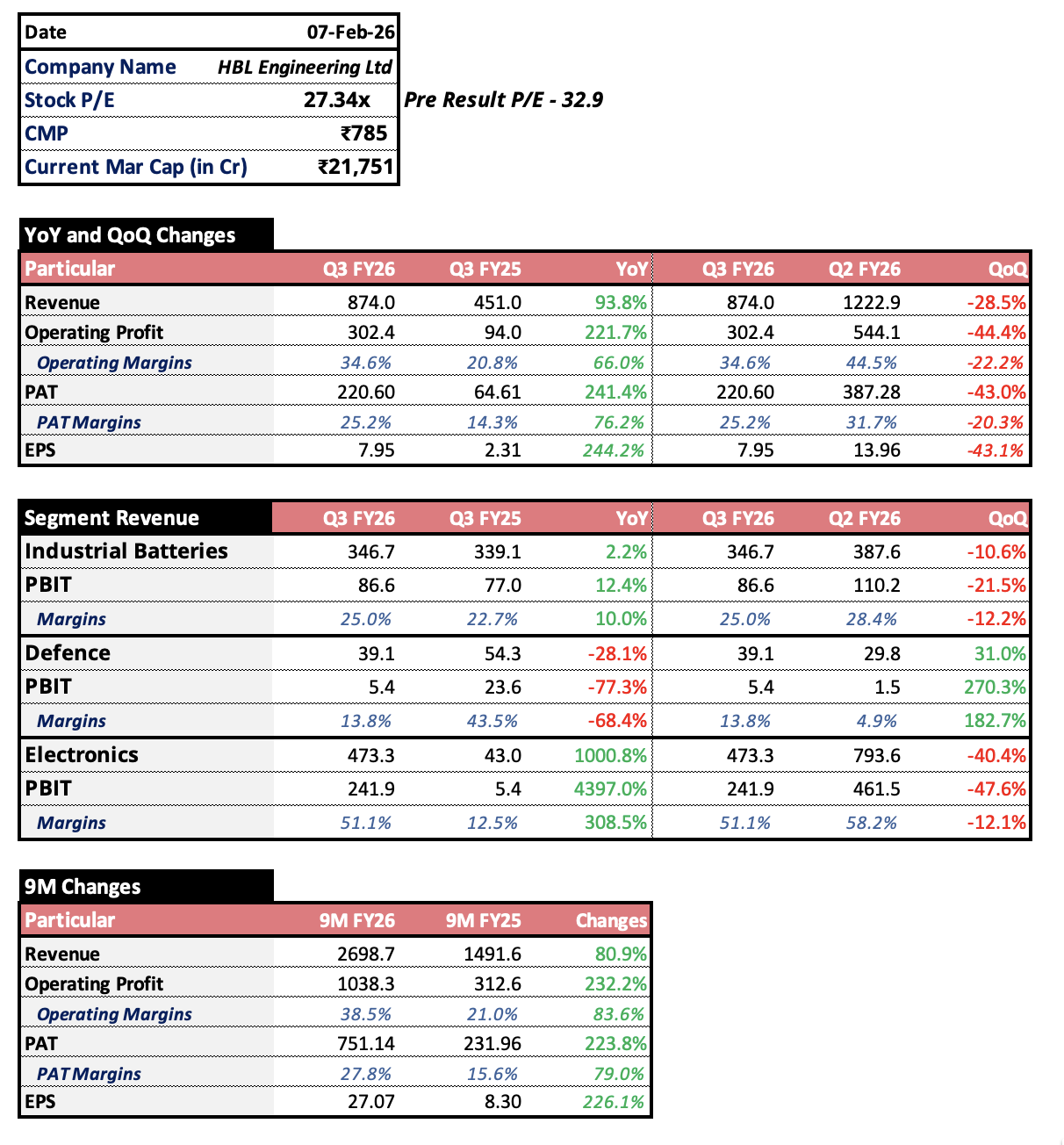

Investing in HBL has been a rollercoaster ride for a lot of investors. Especially in the last couple of years. And topsy turvy markets don’t help its cause.

This is a business with inherent lumpiness. The growth engines keep changing from time to time. Earlier it was industrial batteries, and they enjoyed higher margins for some time due to Russia Ukraine conflict because of shortages created in supply of Nickel Cadmium batteries.

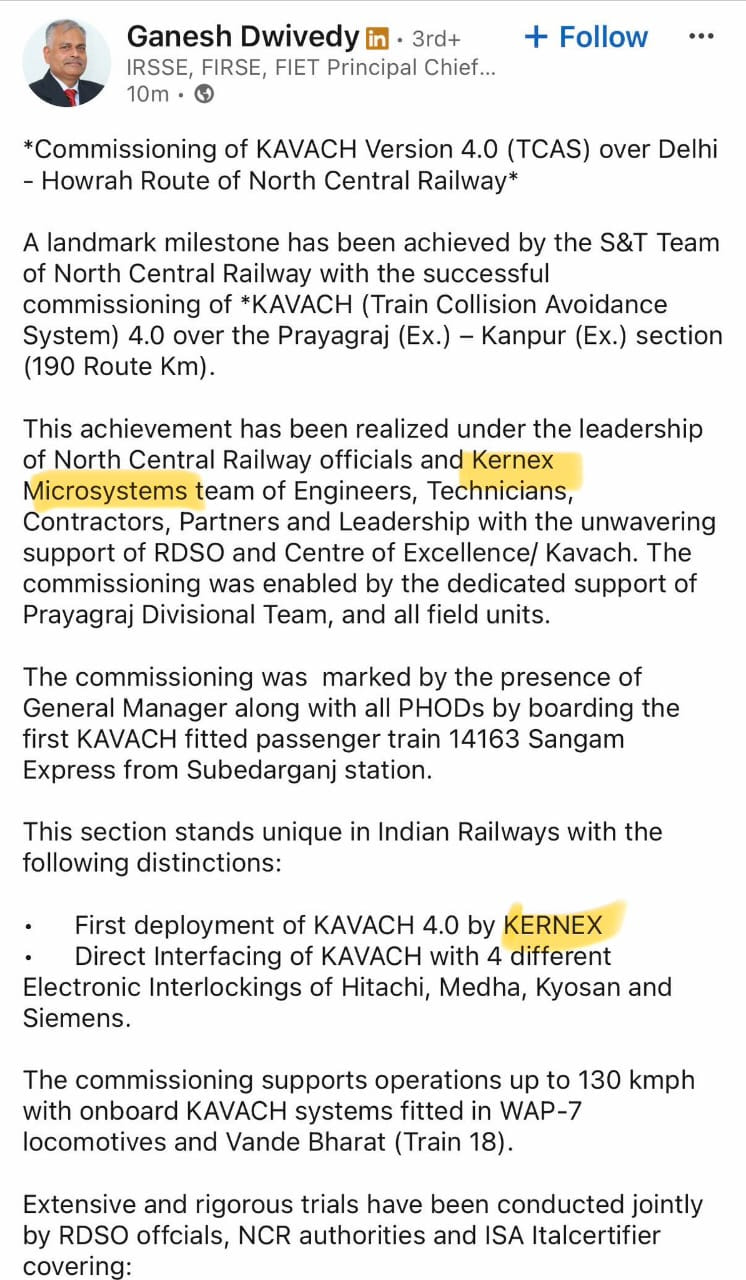

Next was the much anticipated Kavach. Here loco Kavach has taken a front row seat recently, while Track and station Kavach has taken a back seat, though order execution should see some traction in the latter. HBL recently bagged two orders totalling around 1200-1300 crores ( adjusting for GST) for Kavach locos. This should provide visibility for next few quarters.

We need to see how the track Kavach execution takes shape and what kind of margins the company reports. Though in view of reticence of the management in sharing details, it would be difficult to figure out exact margins of this segment of business.

Next bunch of triggers could be defense batteries like torpedo batteries and the likes. Plus marine batteries where it has joint venture with Cochin shipyard. ( need more clarity on the addressable market of the latter segment).

Another much talked about trigger is the Electronic fuzes. Again there are a lot of wild guesses as to the kind of opportunity this segment offers.

The heartening thing from results till date has been clean balance sheet, steady margins in battery business, and contributions from newer growth segments.

The big negative has been lack of communication from management, and lumpiness of the business.

The lacklustre results in last quarter are as per management communication conveyed in q2 fy 26 note. However there was some reversal in stance post that note in another note. Overall FY 26 should be good, though not spectacular, and that sets the stage for lesser expectations from FY 27. With the recent correction from 1000 plus levels to around 700-800, valuations also have seen some correction.

If and when the management communicates about the prospects of the business and its segments, we can get a better idea about how things stand. (disc: invested and hence my views are biased. _