They have finally entered into electrical appliances by launching electric kettle, and many more appliances will be launched in couple of years, lets c how it pans out,

2 Likes

True enough. However, they are looking to expand beyond their confines.

I like the simplicity of the business, zero receivables, and almost no inventory and payables.

If they get aggressive on growth, it’s at an ultra-cheap price.

3 Likes

If v look into the balance sheet asset side they are having CWIP 10 , So capex is also increasing , hawkins could be dark horse , v will have results in 2 years .mgt is slow but very shrewed .

1 Like

The company has recently partnered with Swiggy and is now intensifying its marketing efforts. It seems that management, possibly realizing this later than ideal, has acknowledged the need to innovate and diversify to stay competitive in a crowded market. To thrive, it’s crucial to launch new products and explore synergies with other businesses. By collaborating with Swiggy, they aim to reach a wider audience, enhance customer convenience, and potentially introduce new offerings that align with their core business. This could be a crucial step toward ensuring long-term success in a challenging environment.

1 Like

I plan to do a small valuation exercise on this company.

What is it that I should keep in mind.

I’ll will share my final valuation here.

Disclaimer: I am an MBA finance specialising student. I do not have any work ex as such. I only aim to learn through this exercise.

Swiggy is food delivery service , what kind of service swiggy and hawkins does together

Hawkins Cookers Limited is now live on Swiggy Instamart! ![]()

Get your cookware delivered faster than the first seeti! ![]()

#seetibajao

4 Likes

Hawkings Cooker profit margin mainly depends on the aluminium. Over the last five years, aluminium prices in India have seen significant fluctuations, driven by various global factors.

2021-2022: used to trend around 3000-3500 USD (OPM dropped to 12-13%)

2023-2024: around 2200USD (picked up to 15%)

Let’s see if we see any improvement in the OPM going forward. It is a very crowded industry with many unorganized players, so improvement won’t be great.

Key triggers-

- Operative leverage may start to play a role in this counter. The next two to three quarters are going to be interesting!

- The Company has increased distribution to nearly 10,000 direct dealers.

- 43 people who have joined management in the last six months

- Launching new electrical appliances to keep up with the trend. Company was one of the early moovers, but could not survive in this portfolio- They s had launched electrical products in 1981 – but they were far ahead of their time – the products were reliable; the electricity supply was not. Lets see this time management can do some wonders!

All these are my views. Biased and invested!

6 Likes

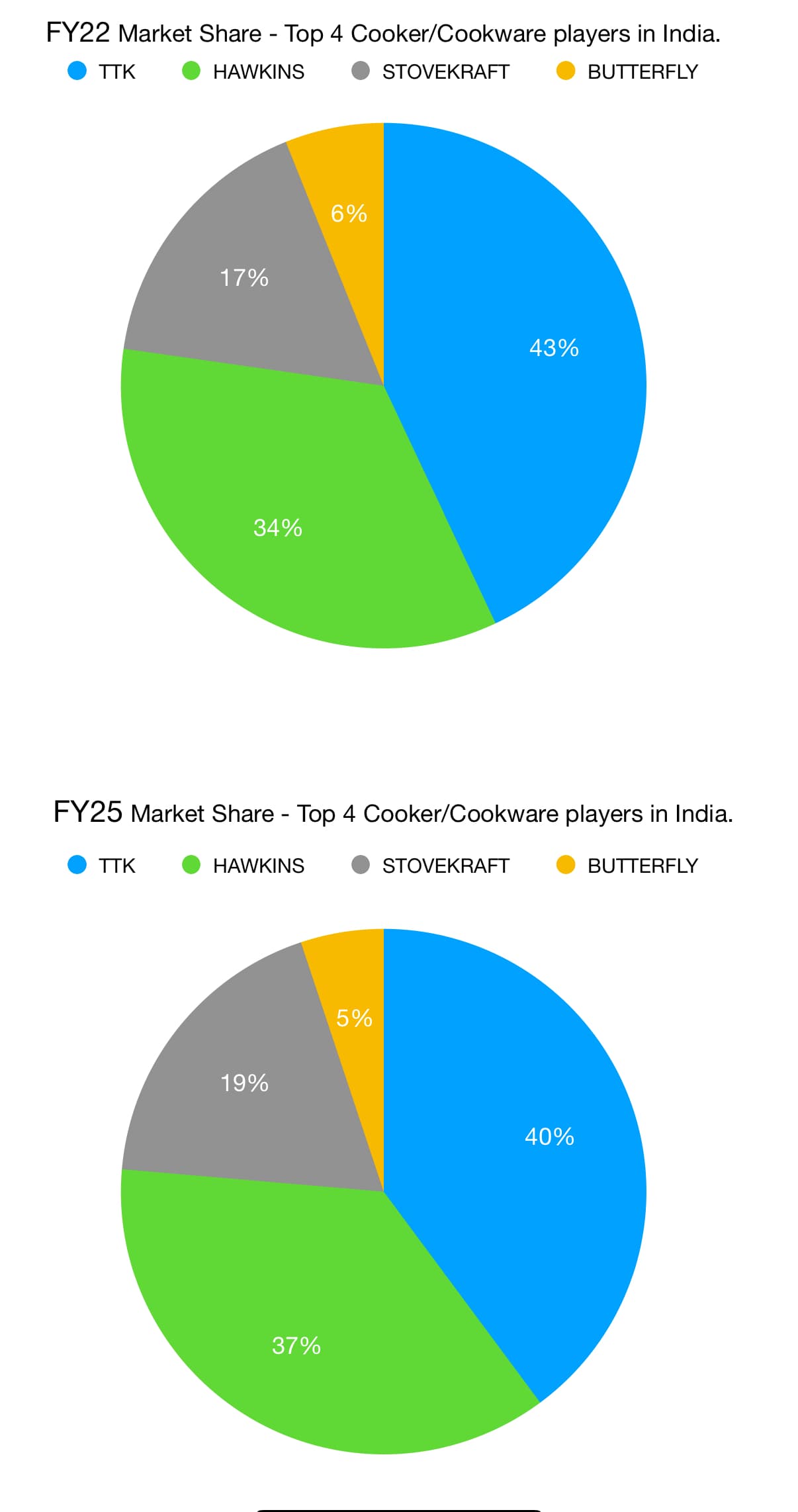

Profit growth since FY22

-TTK -50%(adjusted for one off)

-Hawkins +37%

-Stovekraft -31.5%

-Butterfly Flat(adjusted for one off)

Sales growth since FY22

-TTK +1.15%

-Hawkins +16.5%

-Stovekraft + 21.5%

-Butterfly Flat

2 Likes

What’s the source for the market share chart if I may?

Accidently stumbled upon this stock. This thread gives great insights into investor behavior. Will definitely read more if I get time. Anyone knows why Hawkins does not do any concalls?

3 Likes

Hey yeah.

Management only does AGMs. Back in 2022 in the AGM they had responded to the volume of requests for a quarterly concall. Essentially they believe the business isn’t so volatile to provide a QnA on a 3 month basis. They prefer the AGM route for addressing investor concerns. Plus Mr Subhadip referenced warren buffet logic behind not responding to too much noise in the market; too many concalls wouldn’t be value adding. The late md of the company Mr Brahm Vasudeva also had a similar opinion of frequent concalls. You can read their AGM transcripts although they’ve stopped uploading post 2022. I plan to join the AGM later this year.

3 Likes