“12. The third set of things that go through this testing process are ideas like

Marketing Schemes and Advertising campaigns. At the end of each advertising

campaign we review them against hard Sales data. If the idea did not produce sales,

we throw it out without any second thought, even if one of us had championed it. The

same is true for our Marketing Schemes. We test their efficacy every six months

against irrefutable sales data. We are, at heart, a data-driven organization and like

Darwin’s Survival of the Fittest works in nature – red in tooth and claw, we are

merciless about killing bad ideas”

the above is part of the speech of chairman during the AGM.

He speaks mainly about stringent product quality and conservative growth mainly fuelled through internal accurals.

its hard to figure what has propelled the sales growth but the sector does have tail winds like

:- 1. govt push for cooking on clean fuel.

2. The brand visibility on all online platforms with good reviews. there are no major discounts which show the pricing power of hawkins.

regards

divyansh

The company has reported Q4 results,sales are down about 21% and profits are down 30% compared to Q4FY19.

QOQ is much worse with sales down about 24% and profits down by 58%.

The company has also decided to skip dividend declaration for now due to Covid.

For the year as a whole the sales grew marginally by about 3% and profits grew by 33.7%.

Sales and Production have partially resumed in May.

Is anyone aware of the company’s Fixed Deposit Scheme? They seem to be offering 9% interest on 3 years, which looks quite good optically. Has anyone used this facility before? Have there been any defaults in the past?

This article may help for Long Term investors in Hawkins

Good brand… Good company… 5 years CAGR sales 8% … 5 years profit CAGR 18%…while valuation may be little higher but…

It is still better than MNC FMCG stock with good return ratio’s as far as valuation is concerned…

Unfortunately , there seems to be no investor fancy for this stock…

Hawkins has now come out with a FD scheme offering 9% interest against bank FD rate of 5-6%…

https://www.timesnownews.com/business-economy/personal-finance/planning-investing/article/hawkins-cookers-fd-scheme-2020-earn-up-to-9-compounding-interest-for-3-years/653315

Discl: not invested…

@hitesh2710 hello sir , are you still invested in hawkins? whats is you thought process choose hawkins not ttk presitge.

What is the rationale/difference behind raising money through the FD scheme than issuing bonds? Does it show the public trustability of Hawkins? Does SEBI have the say on it? Someone experienced in these procedures please explain, which will be helpful to understand the dynamics of the Hawkins cooker. Thanks

FY21 AR Notes:

- The Government of India has made the ISI mark compulsory for all pressure cookers sold in India from February, 2021. Company is the undisputed leader in quality and expects to gain from this development.

- Increased demand for our products post the COVID first wave, due to increased cooking at home, especially by the housewife. Demand for quality cookware was excellent.

- Expect our products to do well once the lockdown caused by the second wave is relaxed. Improved our presence in the online segment, while improving the distribution amongst dealers by 29%. Successfully launched Pressure Die-Cast Aluminium Cookware and a range of other Cookware and Pressure Cookers.

- Permanent employees were 609 (were 651 in FY20) through normal attrition and recruitment. The increase in the remuneration of the total employees during 2020-21 has been lower due to retirements of higher paid employees and induction of fresh employees

- Cash and cash equivalents plus balances with banks on deposit accounts as on March 31, 2021, were Rs.161.29 crores (previous year: Rs.42.57 crores). Plan to utilise these funds appropriately, in managing working capital during COVID led lockdowns and in expanding production capacity.

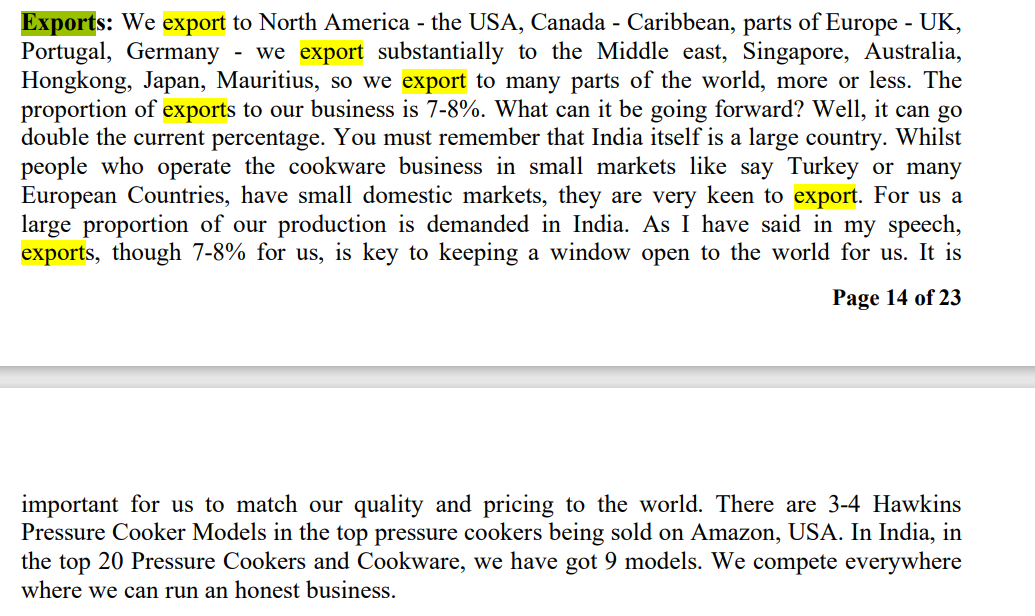

- The value of exports at Rs.65.58 crores in 2020-21 was up 63% over the previous year. In 2020-21, the Company’s exports were all on advance payment or Letters of Credit at sight. Therefore, the foreign exchange risk was minimal.

- The expenditure on Research & Development in 2020-21 was Rs.5.22 crores, 24.2% higher than the previous year.

- Company launched Hawkins Nonstick Die-cast Cookware in 2020-21. Die-cast technology allows for more precise engineering of metal thicknesses to provide metal where it is most needed for even heating, superior strength and more optimal metal consumption.

- Raw material prices are a cause for concern – most items have increased sharply in the last few months – we have taken a price increase of 5 to 10% in order to mitigate the impact. The principal commodity used by the Company is aluminum. The globally accepted benchmark for aluminium prices is the price quoted on the London Metal Exchange. The monthly average of the LME quotations in April 2020 was US $ 1457 per tonne and in April 2021 was US $ 2324 per tonne, that is, 59.5% higher. The Company has taken a price increase in its products in April/May 2021. The Company does not undertake any commodity hedging activity.

- Capex: Overall Capex of 14 Cr. Out of the same, 11Cr. is under Plant & Equipment.

- Outlook: We believe the outlook for our business is very good under the circumstances. In this year, we have further strengthened the good reputation we have amongst our consumers and traders, associates and vendors, by being available and open even in difficult times. We expect to continue to increase our sales and profits.

My observations:

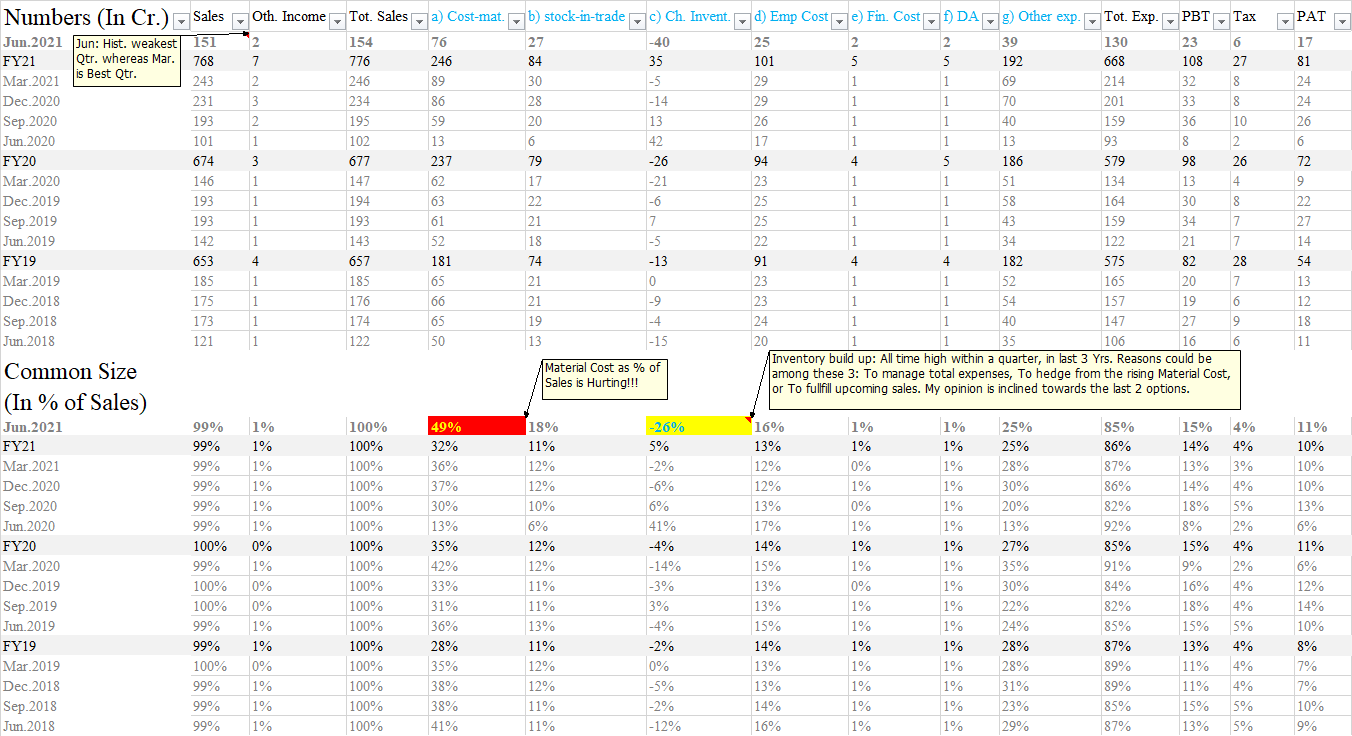

- Aluminum was 44% of the ‘Cost of Materials Consumed’.

- AR pays tribute to Late Mr. Brahm Vasudeva (Ex Hawkins Chairman), displaying snippets from his various speeches. So much wisdom, which is simple and written in minimum words, is hard to find at one place.

- Capex done in latest 3 Yrs has increased tremendously considering 12 Yrs period.

Disc: No Investment.

Hypothesis: Cookware manufacturing is now in-house and being scaled incrementally. Also, manufacturing operations are aligned to produce more Stainless Steel based products, both Pressure Cookers and Cookwares.

Basis: AGM Transcript of FY-20 : Provides a subtle hint, noted below for quick reference.

Since we find that the consumer is showing a preference for stainless steel, we have come up with large numbers of stainless steel products in pressure cookers and in the last year-as you can see at the back of our Annual Report-in Tri-Ply cookware which is an excellent quality stainless steel product from us. We are aware of the stainless steel market growing faster and we are increasing our production and we are increasing our product range. In rupee value, the Company earns more margin on the sale of a Stainless Steel pressure cooker compared to an Aluminium pressure cooker.

Product Sales Trend w.r.t other listed major competitor <Pressure Cooker & Cookware (Amt. in Cr.)> : Make your own judgement from the below data.

| FY-21 | FY-20 | FY-19 | FY-18 | |

| TTK Prestige | 933 | 888 | 948 | 865 |

| Hawkins | 761 | 666 | 647 | 550 |

Is the above sales trend sustainable for Hawkins? Likely because Competitors are dealing with COVID+China+ISI Mark, whereas Hawkins is focused on selling:

-

From the AR’s of TTK Prestige- Rerouting ‘manufacturing and supply chain’ of pressure cooker and cookware to India from China in last 2 Yr. Example shown below -

-

ISI Mark Impact: (From the Hawkins AGM Transcript of FY-20)

If ISI is implemented properly in this country, it will make a lot of regional brands and the non-organized sector improve their quality and that will be an opportunity for us because their price difference with us will come down as they use better materials and better their quality.

- Adding New dealers: (From the Hawkins AGM Transcript of FY-20)

In my speech I have said that this year we have made about 850 new dealers. There is a power in the brand when calling up dealers. We expect to create many more new dealers this year compared to the last year. We also believe that when there is a break in the market, and you are able to take advantage of the opportunity, you take market share.

Disclosure : Initiated a tracking position around CMP. Please do not use the above as an investment advice due to the below reasons: * I might be wrong in my understanding of the business, if history really rhymes.** You may not know if I change my mind.*** Resources around you will help to build the conviction, which is the most important thing for direct equity investing.

The real growth driver will be in stainless steel products. If they get this right, then they will do well in urban areas, where the dishwasher sales have shot up since the lockdown. Dishwashers are built for steel and glass cleaning, not aluminium. Will be interesting to watch their sales trajectory vis-à-vis dishwasher sales.

Rating (July 23, 2021) updates from ICRA- Link

Key Observations:

- FD program enhanced to 2X (~50Cr.)

- Vulnerability of the company’s profitability to volatility in raw material (Aluminium and stainless steel) prices and intense competition, relatively concentrated product portfolio and limited market size (Per May25,2021 Conf call (Link) of TTK, Pressure Cooker and Cookware Market is 2200+Cr. and 1400+Cr. respectively)

- Key rating monitorable: Company’s ability to diversify its products into new categories to reduce its concentration on a single product. In FY2021, pressure cookers contributed around 75% to the total sales, cookware about 21%

*Cookware now increasingly manufactured in-house, are still mainly traded. Distribution network, supported by ~6,500 dealers (Was noted as more than 5000 in FY20 report)

Disc: As above.

Thanks to the virtual mode for AGM’s. I was able to join, glued to the screen for 3+Hrs. and enjoyed the event. When couple of fellow minority shareholder’s went to weeds and started wasting everybody’s time, management’s management skills were evident in handling the situation!!!

Here are my main notes, recalling from memory and may contain inadvertent mistakes- Be on the lookout as the company may place the formal transcript on it’s website in the coming days :

- New product launch beyond cooker and cookware in Pipeline. Can not disclose due to competitive reasons.

- Mfg. moving in house - both cooker and cookware.

- Expanding capacities.

- Demand is excellent.

- Raw material price remains a cause of concern- Will not hedge and buy as needed, but open to increase prices for mitigation.

- Happy to display in MBO’s considering quality of the product.

- Worker’s monthly bonus rolled out, tagged to plant’s quality target.

Chairman’s AGM Speech - Link.

Q1FY22 results were also declared yesterday. My observations:

Disc: Invested.

> Not an investment advisor. Please do not use the above as an investment advice due to the below reasons: * I might be wrong in my understanding of the business, if history really rhymes.** You may not know if I change my mind.*** Resources around you will help to build the conviction, which is the most important thing for direct equity investing. ****Return expectations from this position suit my Risk profile, which is unique for each individual.

prof bakshis old blog insight about DNA of Company

Triggers :

1 High Margins Steel cookware has greater margins and higher remarket place .

2 increasing share of market .

3 Cash Conversion days is now around 40 -42 .

4 Unique initiative by company one of its kind

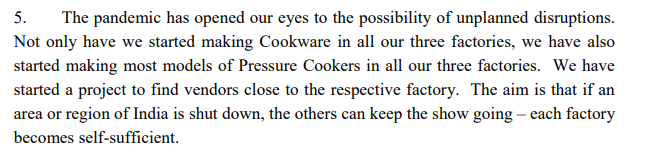

5 Aggressive sale points added and action been taken for each factory be hub of manufacturing all products at all the factories

6 Quality will endure and capture the market share

Disc : invested recently

Have just started tracking Hawkins. The exports as per last AR were up 60% YoY, however I am not able to find much information on which countries they are exporting to, what is the growth strategy here, how are they achieving these dramatic growths? Has management ever guided on exports before?

% growth may be inappropriate as base for exports is small. Sales- Domestic & Exports - number (from ARs) for the last 4 Yrs.:

| Sale of Products (Cr.) | FY18 | FY19 | FY20 | FY21 | ||

|---|---|---|---|---|---|---|

| Domestic | 515 | 609 | 625 | 695 | ||

| Export | 35 | 38 | 40 | 66 | ||

| Domestic | 94% | 94% | 94% | 91% | ||

| Export | 6% | 6% | 6% | 9% |

As far as I know, they do not give any guidance. On exports, managements view is available in https://www.hawkinscookers.com/download/Transcript%20of%20the%2061st%20AGM.pdf

Relevant snippet, which answers your question -

More details available @ Service: Rest of the World

Disclosure - Invested.

Few business updates that I sensed in the last few months:

- Raising FD money at lower rates

- Hiring initiative for IIM Kashipur graduates

- Bulk sales initiative for gifting- http://gifting.hawkins.in/

- Record Sales in Sep 2021 even though PAT remained unchanged on YoY basis

- Capex of 12 Cr. by Sep 2021 (highest ever spend for 6 months period)

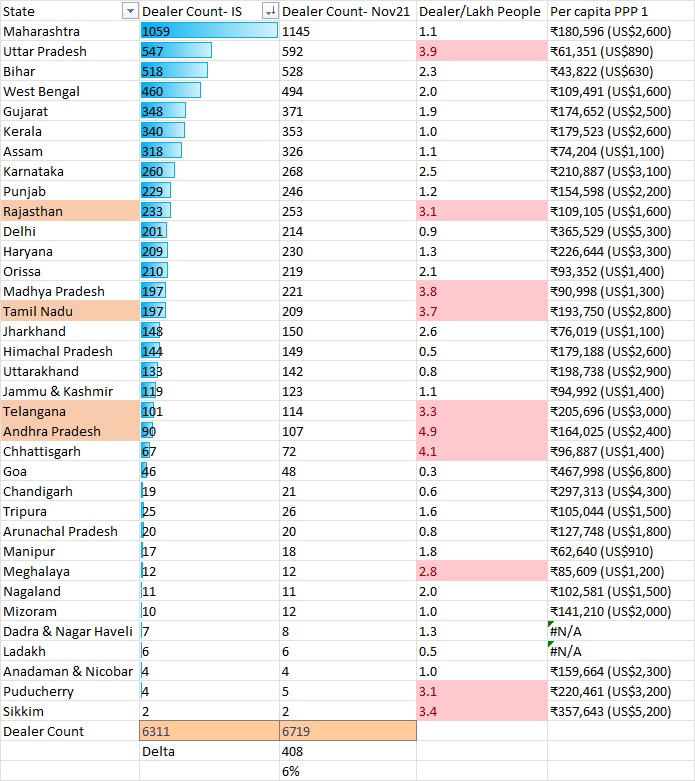

- Increased dealer touchpoint - +400 [Was 6311 till Oct | Is 6719 in Nov]. Refer image for details (Source - Company website)

Disc - Invested.

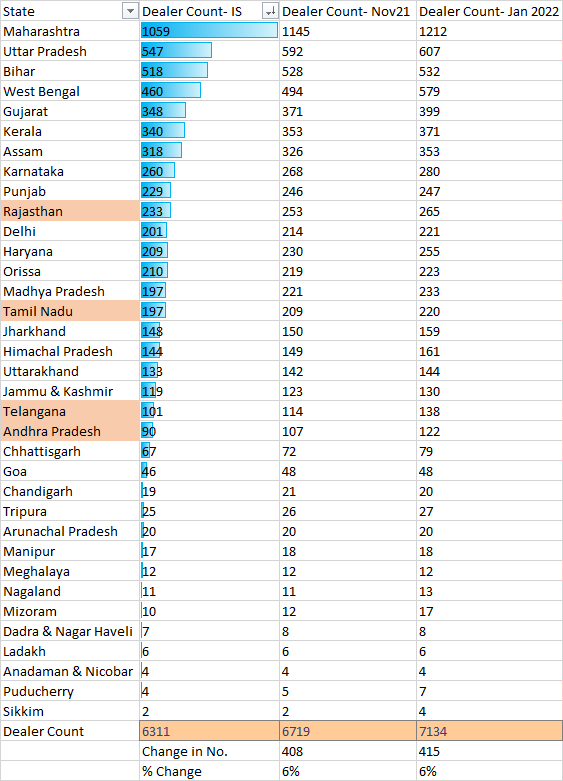

Another 400+ dealers added- Last column (source - Company website):

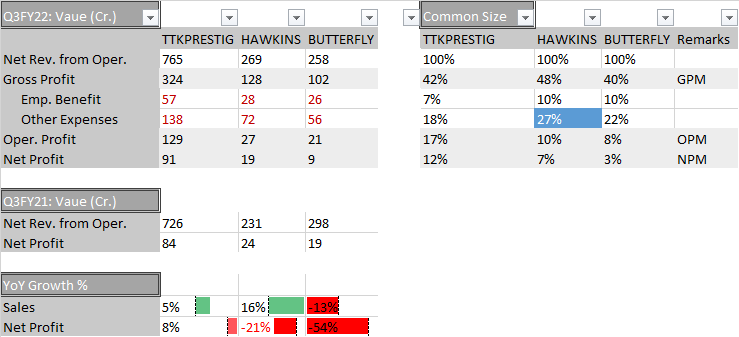

Results for all 3 at one place.

Two of them gave ‘festival shift to Q2’ as the reason for low or negative YoY sales growth. However, Hawkins remained silent as usual but numbers show sales growth of 16%. Other expenses, which were elevated in Q2 as well, did not let the fat to trickle to the bottom-line.

Disc: Invested.

Hi,

A good set of numbers reported by Hawkins even in inflationary market conditions.

EPS Jumps to 43.62 compared to 32.39 on yoy basis.PBT jumping to 30.91 crores compared to 23.03 crores on yoy basis.

Full Report attached(uploaded in BSE)

293341bb-5f5e-4da5-95ee-f1c92082ffec.pdf (2.8 MB)

Thanks,

Deb