I booked profit ling time back. Promoter is ethical but he is nearing 80 so why wud he put in long working hours . Let 2nd gen enter n then.evaluate

2 Likes

Hawkins offering fixed deposit with 10.75% returns

http://www.hawkinscookers.com/Fixed_Deposit_Scheme.aspx

Interesting. Any idea about the rationale behind this?

It’s for there working capital that’s what is mentioned. Seems they have done it earlier as well.

Why this schemes is called as unsecured fixed deposit ? . I think the interest rate is pretty good . What are risk factor we need to consider while investing in any company’s fixed deposit scheme ?

For retail investors always better to go thru Debt MF’s instead of company FD’s.

Hawkins looks low risk as the business has excellent cash flow and high dividend record.

1 Like

Why are they even doing it? They can get loan at a very low rate given their excellent track record and high cashflows. Why give 10.75% interest and gather funds for working capital?

1 Like

Amount being raised is just 1 crores - Rs 1,11,93000 to be exact - see 2(iii) of the fd application form .Last year the amount was 75 Lacs or so and got filled up in 30 minutes of opening.

Hi,

Looking into 5 years chart I saw that there is virtually no growth in terms of share price of Hawkins.where as its eps has increased from 60 odd levels to 100 now.So fundamentals are improving more and more.So I don’t understand 1 thing,why the share price is stagnant for such a long time??

Disc - I am invested

Thanks,

Deb

It is undergoing time correction (de-rating) as the growth visibility has reduced compared to its Peer TTK Prestige, which has diversified its offering and is maintaining growth momentum.

1 Like

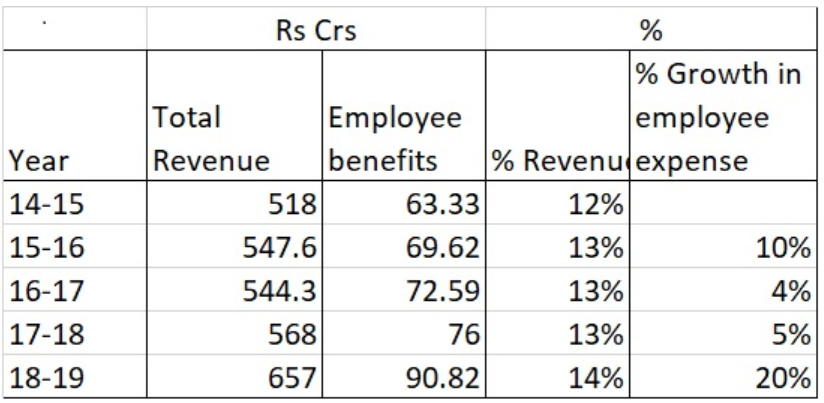

Though the employee benefits as % of revenue is more or less consistent with last few years, but still i felt the employee expenses should not be more 10-11% for such industries. In absolute terms it has increased from INR 76 Crs to almost INR 91 Crs in 2018-19 which is a steep growth of ~20%.

1 Like

Hi,

Hawkins reported good set of numbers.

Thanks,

Deb

Enjoyed reading Hawkins’ Chairman Speech at 59th AGM available here. Thanks to Jatin Khemani for the tweet.

Highlighted below are few nuggets. Recommend reading the full speech at the above link.

Strategy - what not to do

- We prefer to fuel our ambitions with our own money, not with hot money that has to be returned when you need it most.

- We also are uncomfortable about other people using our money. We run a tight ship on collections. We have a record of collecting 99.996% of our dues without fail. We are not in the habit of “buying” sale with unlimited credit or credit to suspect parties. We give lucrative discounts for paying upfront and so a substantial part of our business is run on full advance.

- We really believe in serving our customers who trust Hawkins. This prevents us from picking up doubtful merchandise from China, putting our name on it and increasing our revenue.

- Hawkins chooses not to put its name on anything that is not of the highest quality and the best design.

- What we do, we try to do well and we will only do other things once we do them well.

Testing

- Every pressure cooker that goes out into the market is tested, with its lid in place, by dipping it into water to ensure that it does not leak. To my knowledge, no other pressure cooker manufacturer in the world does this. Largely because it’s a messy thing where you have to immediately dry the cooker, otherwise you will get water marks.

- Other 25 tests are done on randomly selected finished pressure cookers and a similar 25 other tests on cookware.

- And it is not just the finished product – the raw materials, the packaging, the safety valve, the gasket, the anodising, every aspect of the product is tested rigorously.

- Product testing is not only at the manufacturing level but also at a product idea level when we deal with new products or product innovations. We believe in extensively testing the prototype in our Test Kitchen where we use the product as a consumer would use, and find out how the product performs. Does the handle get too hot? Does the food burn at the base? Can you pour without dripping? OK water pours fine, but what about milk? Milk is fine, but what about Rasam – those tiny floating bits?

- This relentless validation is key to our new product development and many an otherwise promising product idea has been killed in our Test Kitchen because it does not meet our exacting standards.

- <<For additional details on written test for candidate, rigorous test during 18-month training period, efficacy of Marketing Schemes and Advertising campaigns, etc, please read full speech>>

Hawkins reported 17% YoY growth in top-line and 28% YoY growth in bottom-line in Q1Fy20. Historically Q1 has been co’s weakest quarter. Remarkable results considering a general slowdown around. When the going gets tough, the tough get going. Endurance.

Disc: No holding.

8 Likes

and to add to your wonderful analysis sandeepbhai if u compare segment wise with ttk, ttk has degrown in cookers ,may be hawkins has taken market share from ttk.

I think they made this comment in the context of the unusual receivable ( By Hawkins standards) this year. Historically ( for last 3 years or so) their receivable was around 45 crore. And the provision was around 1cr. ( I dont know if this provision column includes only the receivables or something else too). This time the receivable is 78 cr. I think we will know by next quarter ( where they disclose the balance sheet) if they are able to match the previous collection track record.

Should one pay 26PE for Hawkins, considering it showed

- 12-month Trailing 3.25% growth in sales

- 12-month Trailing 5.5% growth in EPS

In 2018-19 the stock showed a negative Cash From Operating Activity; this is a first in ten-years.

Quite clearly the business is showing a slowdown and is not deserving such a high PE. It is a very good business, but a good stock to buy at a lower price.

Pleasantly surprised by the very good results posted by Hawkins. Good growth of 11% over last year and 34% over last quarter as this is the season where maximum sales happens. The EPS has also shown good growth which has translated to increased cash flow from operations. All in all good results on all fronts. But i am surprised to see the stock price movement was happening for the last few weeks as the market seems to have got an estimate that the profitability would be much better than last year even during this economic situation.

1 Like

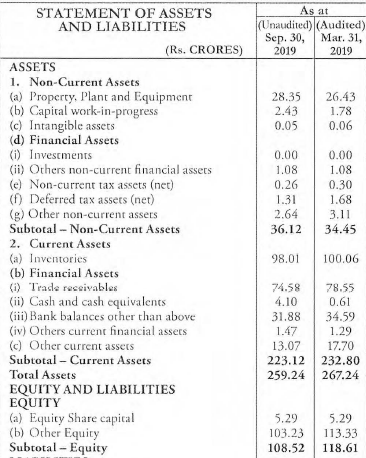

not much reduction in inventor and receivables in h1.

also, there seems to be an error in the figure of total equity. how come other equity as at sep is lesser than as at march, inspite of profits in h1?

1 Like

Hawkins Cookers _IC_Angel_Jan2020.pdf (482.4 KB)

some comparison with ttk. hawkins have grown faster than ttk.

4 Likes

- The company has been delivering sales growth north of 10 % in such difficult enviorment.

- Corporate tax cut has boosted the bottomline in a big way but the growth in sales is more exciting.

- will dig more into the reason for sales growth , specially what has materially changed in last few quarters. but the trend is pretty encouraging.

- Hawkins is a household name and any attempt to fory into ancillary business without raising debt can be incrementally positive. Though at current stage this is a just a assumption.

- The share price has touched new 52 week highs but on a one year forward PE it is at 25 PE (considering next two quarters also give 20 crores + in net profit) which makes it cheap as compared to ttk and other listed players.

- As written before more important is sales growth which was missing for years.

views are invited

disc: invested on technofunda basis from 3600 levels

willing to add on better results and mostly focusing on the topline.

regards

divyansh

2 Likes