Dear Sateesh,

It has been advised by moderators many times to dig in more depth before posting any new idea on forum.

Just copy pasting few lines from some blog wont help much and rather be a turn off for others.

I request you to please share more about their business, management and valuations from your point of view to make this discussion a worthy one.

Dear Vikas,

I posted it in questions&answers sections to get the other member views. I can copy paste the content from blog but it is disrespect to blogger research work. I am novice and if moderators do feel it is unwarranted request them to delete the thread.

But i just want to know any negatives from others.

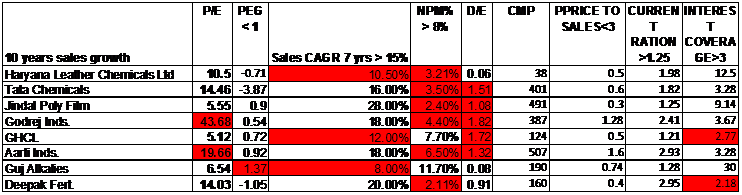

Yes, but in the current year last 2 quarters are showing improved profit margins.

Establishing dealership network domestically and internationally will be the key growth driver going forward.

Company’s R&D work in acrylics, VOC free polymers needs to be understand from my side.

I am searching the same on net.

Book value of 54rs, CMP of 33rs, EPS of 4 and PE @8, market capitalization is @16cr and regular dividend player for last 6 years. What am i missing here for reason for dirt cheap valuation @16cr market valuation with annual sales of 40cr and nil debt.