Inspite of delivering excellent output why this stock price not growing?

My views,

- Have shared my reason earlier on HGINFRA.

- Apart from the above, there is lack of order inflows from NHAI this year, which has been one of the reason for underperformance of road infra stocks, in my view.

having Said that, if NHAI come close to their 6000 km order target, then road infra companies will have a great order inflow this quater and they may give some outperformance.

Disc: Invested in HGINFRA since about 200 levels.

4 Likes

thanks ![]()

I want to hold it for 2 years more.

I think most of the orders are delayed keeping in mind of general elections…Most of the orders will start flowing in this quarter with feel good factor for central government.

Orders have certainly picked up both road and rail.

1 Like

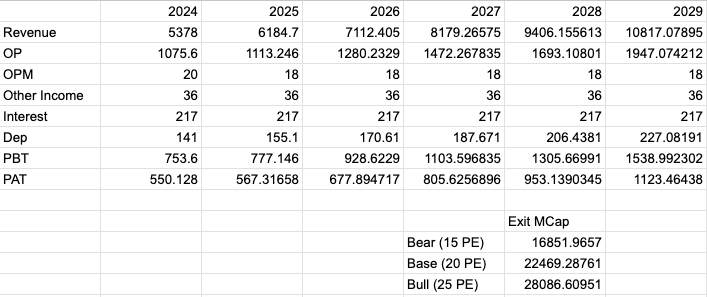

Sharing with you some numbers of #HGINFRA

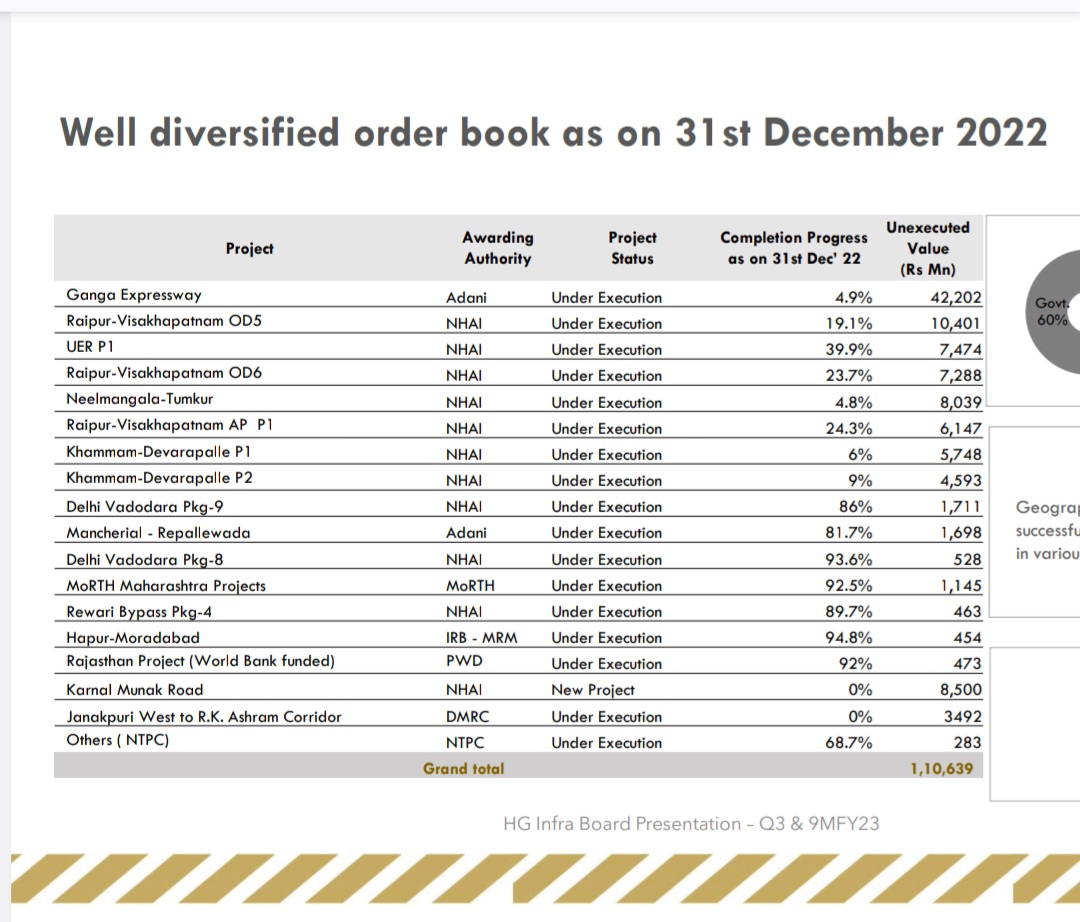

● Imorovement in orderbook

As of Dec 2022 = their orderbook was 98% Road, 2% Rail

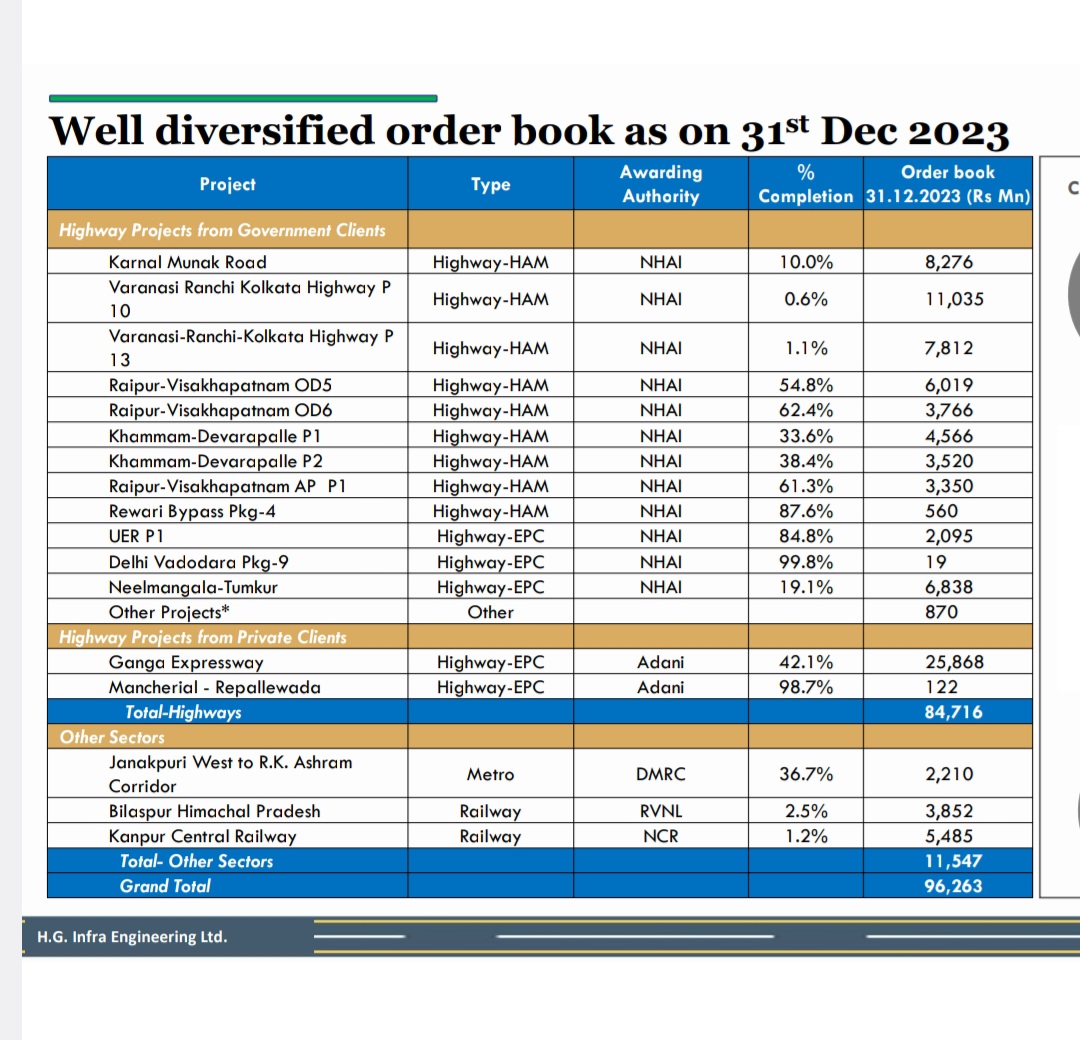

As of Dec 2023= Their orderbook was 87% Road + 13% Railways

As of today= Their orderbook is 72% Road + 22% Railway + 6% Solar

● Orders received in last 3 months

Railway= 1872 Cr

Highway= 1472 Cr

Solar= 1560 Cr ( Joint venture )

As of today their orderbook

Road= 9940 Cr ( less this quater )

Railway= 3000 Cr ( less this quater )

Solar= 1560 Cr ( Joint venture )

Current orderbook is at about 2X/ FY 25 sales & much better award wins are expected in FY25 after election

In last concall, company has guided for 6k Cr topline, 15-16% Ebidta, 10-11% PAT FY 25

Disc: Invested since 2021 - sold some last yr ( to make my invested capital free at about 4x gains & to invest that in other sector ) now adding on dips this year, as orderbook looks much diversified, May be biased - sharing for learning

4 Likes

Tried digging up the details of the JV but to no avail. Two things, a) the Solar order value I believe is inclusive of GST, so net of GST the actual order value would be close to 1320 Cr; b) The share of HG Infra is unknown meaning the order value on their books will be significantly lesser than 1320, am I right?

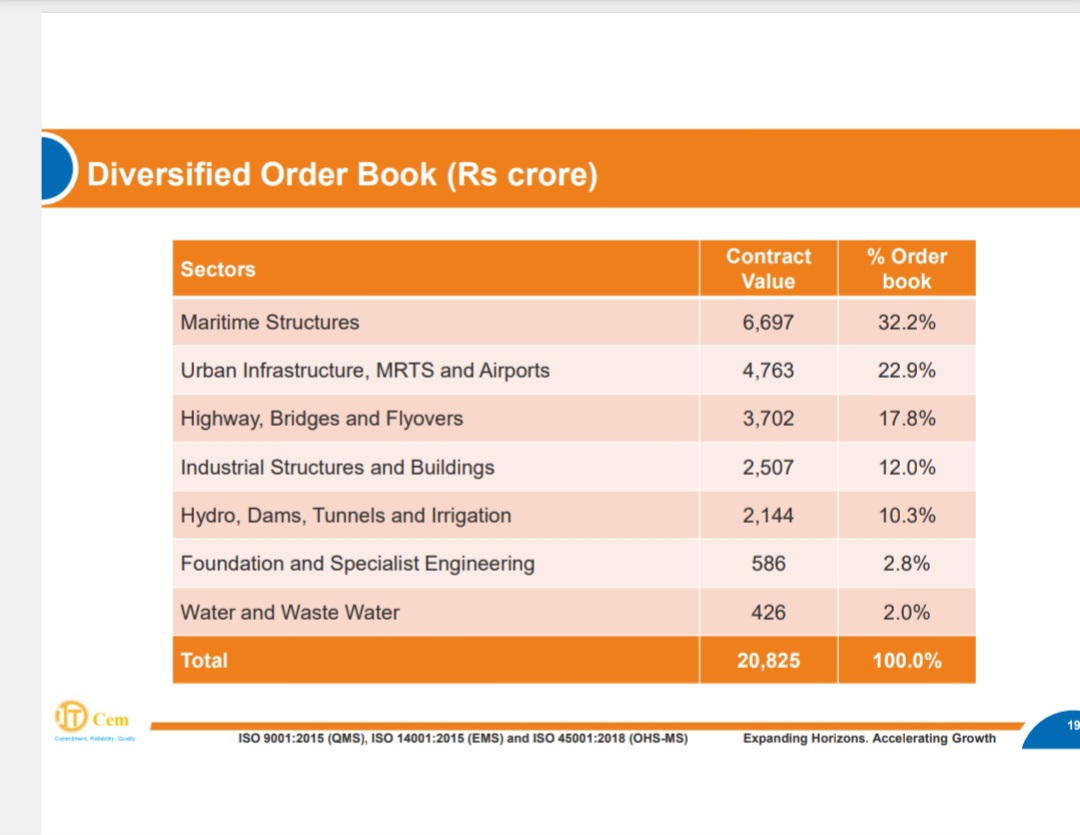

I’ve been tracking this company for a while now but the market seems to be favoring ITD Cementation among the infra pack ![]()

1 Like

Even I couldn’t find JV details & hence taken 50:50 jv assumption for the calculation of orderbook.

Now even at 1320 Cr, they need to execute it within 12 months - so it makes 10% of their revenue for FY 25 - which is good considering their first year in this segment ( calculations are based on 50:50 jv assumption - which I havent verified )

On ITD cementation - They have very good diversified orderbook and thats why they enjoy premium. Infra companies with good diversification is a positive factor in their valuation

4 Likes

Q4 FY24 Concall notes

Diversification and Sector Overview:

- Diversification into solar power plant projects.

- Indian infrastructure sector booming, with significant funding boost.

- Vision 2047 aims for extensive highways and high-speed corridors.

- Interest in Namami Gange program and water infrastructure projects.

Project Highlights:

- FY '24 new project projection: Initially aimed for INR8,000 crores, achieved INR4,350 crores (due to all time low NHAI awarding).

- Q4 FY '24 secured three new railway projects in EPC mode, totaling INR1,872.33 crores.

- Two new highway projects awarded in Q4 FY '24: Chennai-Tirupati Package 2 and Kalimandir-Dimna Chowk.

- Entry into solar segment with KUSUM-C project for 543 MW DC valued at INR1,307 crores EPC.

- Collaboration with Stockwell Solar Services for Jodhpur solar project worth INR2,300 crores.

- Future guidance: Aim for INR11,000-12,000 crores order inflow in road, railway, solar, and water sectors.

- Expecting 15-20% growth in top line with steady margin of 15-16%.

Operational and Financials:

- Order book stands at INR12,434 crores, diversified across EPC, HAM, railway, and solar segments.

- Challenges faced in Neelmangala-Tumkur project due to land availability.

- Railway projects progressing well, with DMRC Metro projects at 50% completion.

- Varanasi-Ranchi-Kolkata Package 13 and 10 in initial stages of land acquisition.

Solar Segment:

- Solar segment contracts under KUSUM scheme: Split project with consortium, HG responsible for 65% of INR1,300 crores.

- Majority of solar project (85%) involves procurement, with HG’s existing EPC team handling civil work.

- Margins maintained at around 15% for EPC contracts, with equity at 14-15%.

- INR1,300 crores project purely EPC, excludes maintenance.

Namami Ganges and Water Projects:

- Namami Ganges projects in initial discussion phase, focusing on water sector projects like desalination and treatment plants.

Order Inflow Breakdown:

- INR11,000-12,000 crores order inflow projected.

- Breakdown by sector:

- Highway: Around INR8,000 crores.

- Railway and Solar combined: INR2,000 crores.

- Water: Approximately INR1,000 crores.

Revenue Projection and Run Rate:

- Anticipated revenue for FY '25: Around 50% of INR12,434 crores order book, i.e., INR6,000 crores plus.

- Similar run rate expected for FY '26.

- FY '25 revenue breakdown:

- New railway projects: INR700 crores.

- Solar projects: INR500 crores.

- Additional revenue from Jharkhand, Jamshedpur, and Tirupati projects.

Solar EPC Project:

- Majority of project EPC tied up with prominent supplier at rock bottom prices.

- No expected price escalation for electrical ancillary components.

- Equity investment around INR520 crores, approximately 40%.

- Monetization plan for project post-completion.

Railway Projects:

- New railway projects initiated despite peers’ exits from railway segment.

- Railway projects structured similarly to NHAI projects, ensuring milestone-based payments.

- Positive changes observed in decision-making and payment schedules by railways.

- Expectation of timely payments to mitigate working capital cycle challenges.

BOT Opportunity:

- Current focus on subcontracting for BOT projects.

- Not pursuing BOT toll projects directly.

- Collaborations with companies like Adani and IRB for BOT projects.

Overall Strategy:

- Continued focus on profitable projects despite industry challenges.

- Monitoring working capital closely, anticipating timely payments from railway projects.

- Seeking growth opportunities through strategic collaborations and subcontracting.

4 Likes

Points for importance

Page 3 & 4/24 on commentary page: Water Projects

H.G. Infra is keen to participate in projects like Namami Gange to clean the backend and rejuvenate the Ganga river, position abetments infrastructure development near the river projects related to water desalination, waste water treatment plants and other water supply projects in rural/urban areas like under JJM schemes. Rainwater harvesting storage under Jal Shakti Abhiyan will be our priority card to contribute with a revenue of around INR50 crores for which we have targeted for this financial year.

Furthermore, we are looking forward for partners with strong background with credentials to cover the technical eligibility for strategic partnerships for breakthrough projects in water sector.

Page 5/24, HAM Project and monetization plan

The total equity requirement of 10 HAM projects is about INR1,461 crores out of which we have infused INR694 crores in this financial year and INR545 crores is estimated to be infused in FY '25. Let me give the glimpse of the status of the monetization of 4 HAM projects. First tranche on the 3 projects which we have sold in the last year, 3 SPV is Gurgaon Sohna, Rewari Ateli, and Ateli Narnaul. They have been completed on 21st of March – 21st November 2023, with 100% SPV shares transferred from H.G. Infra to Highway Infrastructure Trust. We have received INR315 crores as of now, and INR60 crores will be released on the receipt of approval from NHAI for GST changed in law claim. It is expected to be received by June 2024.

1 Like

Any idea why they are incorporating so many subsidiaries? Is it to place tender bids where they are planning to execute in partnership with some other company?

1 Like

I sent an email asking the exact same question to management and waiting for a response. They incorporated 40+ subsidiary companies in the last 8-12 weeks !!!

1 Like

Did you hear back anything?

Their spree of opening subsidiaries isn’t ending. What are they cooking?

I had sent a similar email. This is what the company secretary shared

“Please be informed that new subsidiary companies are incorporated/being incorporated to execute the solar projects awarded or to bid for new solar projects in the future. A new subsidiary doesn’t mean the award of a new project. The award of projects will be separately intimated to the stock exchanges.”

2 Likes