Wonderful thread Suvi. Keep them coming. May be you should consider writing a book. Great content. Really loving it.

Guru Mantra 13: Value Investing (Investing Values to Life)

Back to 2012, unusual cold engulfed Mumbai that year; the mercury dipped to 8 plus degrees. It was around 6 O clock in evening, I rushed out of airport quickly and jumped into an auto. Without even looking at driver’s face I said loudly, Bhai Saab “Parle Chalo”. That’s Mumbai, the blood line of Indian financial system, the gatekeeper of Indian treasury and also a place in India where you can comfortably jump in to a cab or auto without looking at face of driver. If I started ranting about Mumbai, the betenoire of the city may shake their head and write me off as habitual imprudent flag bearer of Mumbai. Needless to say I am one of those who worships Mumbai spirits and will continue to do so.

By the way I didn’t went to Mumbai for paying another tribute to impeccable queen of India but to keep my head straight and listen to one of Guruji’s friend along with few others. When I saw the gentleman he must be late in fifties, with one of those white old pyjamas, black type of specs may be outdated. A room full of books and apparently we knew his portfolio was close to 70-80 Crs. So I asked Guruji what are we up to today? He said nothing I just wanted to introduce you guys to an old friend of mine. I was more than displeased, murmured myself Guruji I flew from Bangalore to Mumbai …may be not a best idea on a chilled evening.

It was a gathering of 8 people, as usual value investing comes up on the table. We were all in a mood not to spare Ben Graham that day citing value investing in real form don’t work today. Now this person (the friend of Guruji) finished one large peg at one go. Then it was fiery speech which I never expected from a person whom I perceived initially as a nerd person.

I am using his verbatim, lot of words today were spoken by that great man whom I again apologising for initial bigotry thought.

He roared, tell me guys; why somebody who was throwing news paper apparently create self made wealth of 60billion dollars lives life like any other middle class and donate every pie he got through entire journey. Is it weirdness? Fallacy? Unstable mindset? You can name anything……value investing is a way of life……it’s a religion of charity and mankind for followers.

Value investing ignites a passion within anyone who is involved into investing in equities anywhere in world. It has become a way of life, an identity for practitioners. Very few will agree it’s absolutely not the same concept what Ben Graham taught all of us. Then bigger question is what is value investing, let us understand one of our own countryman first.

Prem Watsa: Cry for few dollars more

His acquaintances say Prem Watsa spent good amount of days in absolute struggle in the chilling winter of Toronto. Now he buys public companies, often called as Warren Buffett of Canada. He promptly agrees his calculation of initial fund was terribly wrong which drove him to a park. He is an icon for me, after graduating from IIT Madras he moved to Canada to work with insurance companies. Value investing has been passion since then, like any other value investing bugs him so hard he decided to become an investor. Currently his net worth is stamped at 1 billion USD. 2012, he bought the famous Black Berry.

Prem Watsa is one of many successful value investors who has been in news for almost a century. Let’s have a look at list of well-known value investors:

Warren Buffett (United States)-67 B , William Ruane (United States)- 4B , Irving Kahn (United States)-19B , Charles Brandes (United States)-2B , Charlie Munger (United States)- 2B , Seth Klarman (United States)- 1.47 B, Walter Schloss (United States)- 1B, Christopher Browne (United States)- 650Million, Alex Roepers (United States)- 14 B

This a small list of value investors who cut into billion dollar club, the full list needs a book. Though any value investors list includes folks predominantly from US actually they are spread across. The basic tenet of value investing is such the value investors are not media savvy, lead a principled life. Before we plunge into the nerve chilling idea of value investing and it’s influenced investors let’s pay attention to some kind of pattern for value investing.

Most of value investors started from scratch, Buffett was throwing news paper, some one was selling flowers, George Soros was a refugee without food, Ben Graham couldn’t pay education fees….the list is long. Conclusion: humble beginning.

Value investors continue to be principled and humble in their entire life. Buffett stays in a 5 bedroom house and travel by economy, Chadrakant Sampat travelled by Bus, Seth Klarman lives in small apartment. Conclusion: humble lifestyle and end.

Value investors donated through roof and land, Buffett donated 99%, Sampat 90%, Irving Kahn almost 50%. They donated money more as they create more wealth. Conclusion: give more expect less.

Hard to get value investors into media glare, most stay as oblivion.

Research has been back bone of value investing, every value investors roughly spend 1000-1500 hours every year.

Writing is connector for every value investors to their imaginations and thoughts.

Extreme caution is warranted for buddying value investors, value investing influence your philosophy, change your life style and more importantly can fundamentally tell you what currently you are doing is worthless ! A radical change may not be needed for all, hence people shouldn’t blindly follow value investing. Most of the times it test extreme patience, can be unsuccessful and asks for tremendous hard work and contrarian mindset.

Genesis of Value Investing

Ben Graham advocated first don’t look at the price ticker published in news paper then. Rather understand the business, buy a piece of it at a valuation so that it delivers more earnings that stock market thinks. The concept remain same, methods are completely over turned; it started with his biggest disciple Buffett himself.

Graham used to buy companies below what he defined as intrinsic value and sell it once it crosses a certain limit over intrinsic value. Buffett put a larger lens by exploring a profitable and log term survival of the business or he called out as durable competitive advantage.

Pre-Requisites for Value Investing

A. Reading is a good habit

Value investing does not ask you to be an accountant or finance person. It does expect you to be an avid reader, philosopher and researcher. One need to create their own spectrum of “Reading Chart”. Currently this my reading chart:

Newspapers: I don’t them read anymore, I rely on alerts from Google, Economic Times, Wall Street Journal and Bloomberg.

Magazines and Publications: 1. Mckinsey Quarterly 2. Monthly HBR 3. The Economist 4. Money Life 5. Dalal Street Journal 6. The Capital Market

Blogs:

Random search, I don’t want to put them to favourites.

New and Old Books: at least 1 every month. Last new book I red was “Super Forecasting by Phil Tetlock”.

Investor Profiles: At least one in a month, last I red was about a guy called Lukas Neely. He wrote a book too:

Popular TV Shows: None, media news are distortion.

B. Change of lifestyle and philosophy

Get ready for a bus ride, walking through dusty road or even a place where you never like to go.

Liking for “uniqueness” whether its music or movie value investing prefers strong focus. This comes with own risk, it may ask you to quit something which you even like.

Arrogance and ego is recipe for disaster in market place. I know it’s not easy to overcome, but those with lesser egos and arrogance will do well.

Predefined mindset thinking this is the best way is going to be an obstacle. Changing views and wandering mind is key force behind value investing. Expect to change your views and mind very often, you may not implement all of them.

Optimism and live with less, information is abundant and plenty yet right information scarce. One has to take decision with available information. Avoid grand ideas and statements.

Ok great, I won’t extend further pre-requisites. What about the “MUST AVOIDS”…yes a small list again.

First and foremost, plenty of investor in market thinks they are investors or value investors in reality they are not. No homework, no discipline ever lead to success in value investing. If you don’t want to spend time you are not an investor……you may keep buying shares, investment is buying business.

I get money from employment I buy what I like and what I think is correct. Perfect way to lose money, in other words you are novice. Hence again get ready to be disciplined again.

Behavioural finance: if you don’t know then read, no one is asking to invent anything. Follow the successful concepts, that’s sufficient for value investing.

I red a small cosy little book by Debasish Basu (plain truth about stock investing), not sure about entire book now. But I like the 16 golden rules what he emphasised :

- An attempt of making quick money leads to losses far higher than the initial investment.

- If stocks don’t seem cheap by historical standards, stand aside or invest in small amounts. There is always chance to buy everything, nothing is end of world. BSE was standing there for 100 years, it will stand another 100 years.

- Buy and hold does not work always, never average down a losing investment unless it’s a part of well thought out method.

- There is no such thing as hot tip.

- Don’t fall in love with your stocks, it will never fall in love with you but fall with market.

- Valuations don’t matter in short run and short run can lasts for months even beyond a year.

- Calculate first how much you can lose not how much you can gain.

- Experts care about risk, novices dream about returns.

- Forecast usually done by experts are trash.

- Develop a method and stick to it and have patience.

- Lots of humility helps, a rising tide raises all ships and so you may be lucky to part of tide.

- Stocks fall more than you think and rise higher than possibly you can imagine.

- Investing in what popular stocks, fad industries or new ventures are riskier than they looks.

- Bear market start in good times, bull market starts in bad times.

- Neglected sectors often turned out be good values.

- Don’t assume either media or fund managers know more than you. Record shows they don’t.

What next? Before we plunge to value investing methods and philosophies an obvious question….why so much efforts? Isn’t going to distract from employment/other activities? Am I not going lose money? Fine, let’s talk about rewards……

“World is shrinking, blank pages of map getting filled up….we must find our own place or perish”- From the movie “Pirates of the Caribbean- Dead Man Chest”

Reason 1: Equity as instrument beats inflation considerably even in a high inflationary country like India. Indexed equity (only large companies) have delivered 17.8% CAGR in last three decades against inflation of 6-7% average (peak was 16%, low is 3.8% now). Inflation eats into your money, meaning value of 1 Dollar/Rupee is 0.95 next year and so on.

Reason 2: Debt which is also loan either loan from bank (liability) or deposit in fixed deposits in bank (assets). Remember Net Interest Income for bank is earned in by lending to us minus paid to us for deposits. Hence rate of interest in loan will always be higher than deposits. For a person with EMI and deposits both is actually negative cash flow which otherwise is positive for bank.

Reason 3: They say knowledge is inner freedom, freedom rules conscience and conscience defines the path to success. If you think knowledge is key to your DNA then equity is best platform, it asks for people with IQ less than 40 and move then to 150 Plus. Value investment requires knowing economics, psychology, finance, anthropology, Meta physics to name a few. PHD gets you a degree, value investing tells you how to turn knowledge to value.

Reason 4: Prospect of a monumental wealth creation and open dreams. Value investing targets somewhere between 100 times to infinity (few stocks delivered more than million time returns) as return. Dreaming in an open space can be nostalgic than within bedroom.

Reason 5: Value investing though synonymous with wealth creation it actually asks you to create values in life. It’s combination of wealth, philanthropy, integrity and honesty. What else one need in life?

I am sure in our childhood we liked something or other, I was a crazy fan of Rock and Metal (till now too!). I kept buying those rectangle shaped “audio cassettes” from every part of world I can access to whether it was courier, or even going to Nepal. I gather around 1400-1500 cassettes, put them to specially made wooden box with electric bulbs inside (someone said they help removing moistures!). Little did I realised audio cassettes will become an item for museum, as different mediums replaced these cassettes I just look at the three giant boxes now (bulbs are now off) which reminds me constantly about stupidity. Luckily, I learned a valuable lesson from the whole experience. Although I don’t exactly remember what that was, I’m pretty sure it had something to do with the importance of saving money for things that you might want or need in the future rather than wasting money.

Unlearning the biases and prejudices

When we speak of Warren Buffett we can’t ignore his basic rule, books (thoughts, articles, research) drives your philosophies, philosophies derives methods, methods and principles executed together with discipline and hard work is stairway to success. This is not applicable only to equity investment but all facets of life.

They say pen is mightier than swords, properly written words can cut across the thoughts and perceptions of masses resulting principles and ethos sometime also called “way of life”. Indeed writers continue to influence generations for long as good role models are imperative. They give us something to aspire, and someone to look for. Of course they do motivate us.

So does investors do write books as well, so what’s difference then; these guys are not someone who go to Alps and sit with windows open against view drop of snowy mountain to strike an idea what can be next human relationship; On the other hand investors got back to table when they started near vision eye glass, with the pedigree of their acquaintance and experience. They don’t write to earn from book, but to guide the “misguided ones”, to ensure the wisdom juggernaut rolls on, an eternal pursuit towards an un-ending tunnel of full lights.

An investor is told to read some books and create a customise discipline and method for practicing the investment. Question is do they matter? Can anyone rake moolah in market by reading books? Well we do not have straight head answer but most of these books help in saving yourself from losing money!

“When you identify action with passion wealth is outcome”.

A investor develop an endless desire to learn for art of stock picking. A perspective investor be absolutely passionate about investing and anything remotely connected with it. Passion of investment is different from passion of stock prices!

The first job of an investor is to look for a group of likeminded people who are focused with serious investing. Having find a group which is devoted and selfless investor should develop a habit of reading, an act where there is no substitute. Create a list of books and understand their investment philosophies. It’s like exam preparation, underline, bold and get prepared for actual market.

Must Avoid

Looking listlessly at stocks which have grown over a period. The price is future business not past track record.

Peer comparison is a disaster for recipe, unless cooked properly it can damage more than a wrong investment. Most of peer comparison is made on financials not business!

I found 99% of people do not invest based on documented decisions but more gut feeling and very little broad data. As a matter fact, 5 out of 10000 investors have tracked, analysed investments systematically on a paper over the years. And those 5 only succeed!

I feel this is right, I need not believe others. This is one major problem I had always during employee days. I always thought I am right all others may be ok but they must pay attention to me. Similarly if I think Mr. X is does not agree with my views I will keep disturbing conversation and somehow I will not believe whatever s/he says. This attitude did not cost a lot during employment, however during initial investing days I lost not only my hair but shirt! Marketplace brings down the most of high fliers almost crashing to ground. I was lucky I escaped with few thousands….you may not be that lucky!

Learning the rope: keeping eyes on ground will help rather on sky. Be truthful to yourself……again going back to employee days. 3+ plus year syndrome at office: by this time I was acquainted to office space, I knew where cafeteria is, I knew how to manage managers……employment is my stronghold! Of course I started cribbing….you know what by accident I am a finance person……I always wanted to open a garment retail outlet. Infact we had the blue print but family commitment kept me away. When I got few critical observations during performance appraisal, first thing I did was to find out another employer! Stop lying to yourself for God’s sake!

Optimism (Extracts from Basant Maheshwari Book- The Thoughtful Investor) with minor amendments- QUOTE

The attributes that can make the mental framework of a person desirous investor can neither be learnt nor taught. It is a general offshoot of how the person has been brought up and how he views the world. Among the trick of games one of the major attribute is optimism. He has to go to bed thinking that tomorrow will be better day. Equity is on basis of what business will do in future, if you feel future is dark……equity will never perform also.

Despite of this investors talk about negativity more, if stocks goes up more they talk about valuations. If prices are low environment is to be blamed. For a defeated person (or investor even) defeat is a complaint book, for a person who makes living out of something have to accept his responsibility.

You must love the market not hate, a person who loves will be more in game ….winner have one thing in common….running for them.

Pain of Loss

The investor does not understand the stock may fall after he buys or rise after he sells. This heartburn can change once you become matured and serious. An investor decide a price to buy and sell, market just provide the platform.

Stocks do not go straight up, if they go come down equally fast. When I was using local transport for saving money 20% fall in portfolio was easier to manage as my expenses was limited. Today even 1% loss hurts me more emotionally as I can’t travel without business class. Now with every loss I compare did I lose the trip to Paris? The imaginary discomfort from not buying things rise with every fall. My suggestion live a modest life, it helps. Falling stock prices are like child falling while learning to walk.

Investing is about making more and more investment and retaining less. Market does not bother about whether you get your capital is recovered or not. All that it does price based on information, opinions.

One of avoiding of pain of loss is you buy more. But as most investors are invested for initial amount conviction level goes down. It is easier to bear the pain collectively when all his friends are also loosing money. There is a strange sense of comfort in seeing everyone loosing money.

Conviction

An investor who does self research is in a better position when downward trend starts. Stealing an idea is easy but borrowing conviction is matter of grit and skills.

(Extracts from Basant Maheshwari Book- The Thoughtful Investor) with Minor Amendments- UNQUOTE

Though equity investment is part of process of globalisation…….its evolving day by day against new challenges, opportunities and threats. Combined with research and patience I am sure we can conquer the fear!

Let’s talk about what is a nest and how to infuse security, safety and random thoughts before we move to investment specific subjects.

15 Likes

What a writing man! I am loving it! Keep posting. Thank you very much for sharing all the learnings!

1 Like

This is incredible stuff, I am getting etched to it… There a wealth of information in your posts!!! Keep posting and help us enrich our investing skills.

amazing, thank you for sharing, learning a lot from the posts!

Excellent stuff Suvi, It would be nice if all your stuff is available in pdf or word format at the end

Wonderful one like the earlier mantras. As I said earlier, it frightens people like me who are beginners, but at the same time highlights what is expected to become a value investor. Its also important to be aware that understanding theory is different from practice. The real challenge lies in execution and may be that is a reason Value investing is an art rather than pure maths or science. Thanks Suvi - Kumanan

Dear Bipin

What I have done is noted more than 10000 conversations, telephone calls as scribble and put them to pages file (mac version for word) all these years (2002-2016).

The information are more abstracts, no indexing as such neither sequence.

This stuff what I produced are here individual page file. Post completion will consolidate and upload if it helps.

Regards

Suvi

2 Likes

wonderful,amazing,inspiring, awesome,impressive but i think words will limit my praise. your writing on the topic shows your extreme knowledge of subject.Thanks for the sharing,keep postings.

1 Like

Guru Mantra 14- The NEST: Building Blocks for Accomplishment

The NEST and mundane thoughts

Why Nest, why not portfolio, why not apartment? One of my friend raised the question with nonplussed eyes. Nest is required by many, can be build anywhere, can be used by many and most importantly durable. The sanguine part of is Nest by definition is a biological urge for users!

Great, what is parlance of Nest in context of equity investment or value investing?

Nest is build by following process:

When we are saying we will build a nest we want to keep something inside it which to our opinion are valuable. Otherwise there is no point in building and spending. There are two types of nest building one Sculpting by clearing the ground, making installation ready. Second is Assembly where requirements are gathered to create a structure. And finally lets not write off saying nests are meant for birds and their eggs, once offspring comes the utility of nest is over. This is the best part, there are nests on ground which can hold millions of individuals like communal nests which are permanent structure goes on for centuries.

Fair point, now break down the components or else we cant practice:

-

Something valuable inside nests are equity shares or a piece of business

-

Protection from competitors or enemies so that my piece of business is not taken away.

-

Homogeneous pieces of business so that I can understand all of them other wise what happens neglected pieces of business will be taken away by enemies. This is nothing but we call it as circle of competence.

-

Successful offsprings be given a choice to express their wisdom. Now our offspring here is the earnings made by piece of business, the wisdom comes from by “exercising an act which gives happiness”. This act can be spending for your own need including nears and dears (say the goals we spoke earlier), giving away money to make you and others happy (here is multiplier effect).

-

Unsuccessful offsprings are fallen from nest, no matter how much pain a mother bird feels by loosing a offspring she has to offload them. This is similar to sell, we have to throw the laggards out. Here there is a twist, as our offsprings doesn’t have life and blood we need not be emotional. If we get healthier ones we replace the dead and weak ones.

You will realise 1-5 above is basically buying, selling and allocating with maintenance. These are investment specific subjects.

Isn’t it simple? I guess not, how do we a build a nest in first place? How do I know where do I build this? What are requirements to build a nest?

You would have seen in above we said first we need to do a cleaning work then gather requirements and assemble it to make a nest.

Two very important things one cleaning up, second assembling. This is where soft and social science come into play. Congregation of ideas- strip out existing model or modify and then assemble with a fresh set of ideas. Sounds lots of preaching, isn’t it? Initially a couple of years I literally broke off my head to visualise this. I will try to ensure your head remain upright there !

Step 1 of Building a nest: Setting up of a seedbed with a defence mechanism

Step 2 of Building Nest: Establish Controversial Behaviours

Step 3 of Building Nest: Rationalise controversial behaviours with defence mechanism

Isn’t sound like jingoism, I advocated all these while for simplicity now throwing up some words to ensure I have a linguistic pretension! Unfortunately I faced the same situation, but let me try to ease these things in simple language if I can. This is bad world of scaring people.

This was just a background work what I did to arrive at my approach. I wont repeat these lines further, let me put it in black and white and trust me this was the most difficult part.

The reason for writing these jargon was basically to tell you, when you run out of ideas and cant explain properly you come with these bombastic lines. By the way this was a lesson I learnt from one B School seminar on mental models.

Also going forward let’s try to be more simpler as execution part is coming.

Nest is a portfolio in our common world term which needs to be created with one more equity shares and protected well so that it create wealth for me and my circle’s happiness. Sounds better?![]()

Better our steps should be

- Create a portfolio

- Fill up with right quantity and quality of equity shares

- Protect them with due care and diligence.

- Create wealth by selling, re-allocating and distributing

Can I ask for a favour, let us flip the word equity share with a “piece of business” and wealth with “happiness”. Rest all seems to be fine to me for now.

Now, if you want to buy a piece of business then there is only one question why I want to buy piece of business? And there is only one answer, to share the earnings of company. That’s it, all our effort going forward is to ensure and know how company is going to earn higher and higher.

To understand let us create a hypothetical scenario:

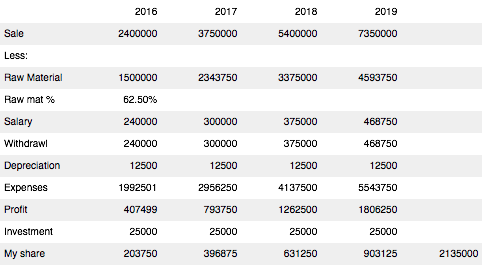

Jatin is selling Vada Pav on streets of Mahim. He needs thela (the hand cart) and other kitchen equipments (lets call it out as Fixed Asset), tomato, potato, masala, pav and other ingredients (raw material for our example) and two assistants (to do the cleaning and other work). Thats about it, keeping simple.

Jatin sat down and prepare a budget:

Fixed Asset- 50000 Rupees required

Salary to two assistant- 10000*2=20000 per month

Raw material- he doesn’t know even!

Great, our Jatin bought fixed asset and with new 2 vibrant assistants moves for greener pasture. First day he bought on estimation raw material of 5000 Rupees.

He put a per plate price of 25 Rupees, at by end of first day he could manage 200*25=5000 Rupees.

Lessons Learnt: Jatin realised he could only recover raw material cost and realise his cost doesn’t mean only raw material rather a piece of every thing that goes into making the finish the product.

Next day he comes back with with 40 price tag. He could manage the same number of customers i.e 200 customers returning 8000 (200*40)

Now lets assume the business goes for 300 days a year with same price tag. Forget 25 bucks price tag now, I brought it as most management learn the trick of trade with time, it can be years for sometime. After all they are humans like me and you.

So our sales per year is 200 customers per day , 40 a plate for 300 days (20040300) or 24 lacs much higher than a IIT engineer!

Salary paid to two assistants 20000 a month for 12 months i.e. 2.4 lacs

Raw material he bought for 300 days at 5000 per day which i 15 lacs

So his profit is 24-2.4-15 or 6.6 Lacs.

Is that all? What about using that Thela (fixed asset)? It has a self life say 25% every year wearing out or 12,500.

What about his own time spent? After all he is an entrepreneur. He thought I will charge myself 20000 per month which works out to 2.4 Lacs.

So what is our profit now: 6.6. lacs- 0.125 lacs-2.4 or 4.07 lacs.

Assuming all customers paid in cash and he paid all vendors in cash also, he walked out with 4.07 lacs with a investment of 50000 rupees. This is whopping 814%, better to sell vada pav than working in employment.

Now lets twist the story, he doesn’t have 50K, he has only 25K. Obviously he has to go to bank or take some money from somebody else.

Take the situation he took bank loan for 25K at 15% interest. At the year end his interest cost would 3750 Rupees only. That means Jatin’s profit will come down from 4.07 lacs to 4.04 lacs.

If he invite me or you to invest that 25K what happens then? I come in as a partner with a 50% share. That means by investing 25000 I walk out every year with 4.07/2 or 2.04 Lacs profit. My return is 814% same as what Jatin alone was taking!

Now let me compare this 814% with the money I could have earn by putting into fixed deposit of 8%. This is an extreme case, just to spice up. But it does happen and that’s the secret power of equity only if you are buying a good piece of business.

Good, what next? Now another one Robin opened another vada pav stall next to Jatin funded by another me or you. He put a price of 30 rupees a plate, Jatin sell dropped naturally; he was forced to bring the price at 30. How does this impact business?

Cost remains same: profit becomes 4.07 lacs minus reduced sale price (10200300) or loss of 1.93 lacs.Fortune changed over night.

Scene 1

Can Jatin still maintain the same price with same customer base? He can if he’s got a taste of masala which cant be found with Robin’s vada pav. People don’t mind pay to additional price for the masala. This is called a competitive advantage for company.

Scene 2

Jatin is not keeping well, he was replaced by his brother Stephen. Customers starts complaining masala is not tasting good any more. This means we need Jatin, or we have to check who is managing the business? That’s called quality of management.

Scene 3

Jatin is so busy or for some reason the vendor is not supplying on time, customer is not paying on time. He needs to sort out these issues….these are called operational risk management which need to be there for efficiently managing operations.

Similarly at 20 Rupees Jatin didn’t even realise he is making losses. He needs to know his pricing or he doesn’t even know whether he can pay off salary or bank loan. These are called financial risks, to ensure our financing methods are robust to provide any return.

Next, the tax men is asking money and want Jatin to fill up forms. We like or not if he doesn’t do the tax work business may got wound up. These risks are called compliance risks.

Last Jatin must think beyond, if 500 customers turned up can the current thela be sufficient? Or does he know Mahim is going ban vada pav next year? These are called strategic risks.

Scene 4

Today Jatin is making 4.07 lacs a year, he called me to invest in his business. I realised after 7 days Robin comes and knock off Jatin’s business. How do I know there are undercurrents to ensure Jatin will stay on course with same earnings? We call them as future catalysts. Future catalysts is an extended application of first three i.e. competitive advantage, quality of management and risk management capabilities.

Scene 5

Now Jatin knows by investing 25K I will walk away with 2.04 Lacs profit a year. He feels he is the one who set it up, he’s the one who prepares that tasty masala. And of course he’s entitled to think so. He asked me pay off 10 Lacs if I have to enjoy that 50% profit every year. Where is 25K and where is 10 Lac? Will it still be profitable for me or not? May be or may not be. This is we call valuing a piece of business and keep a safety net for ourself for errors or** margin of safety.**

Scene 6

Now Jatin holds a business interest in his brother Stephen’s thela by putting same 25K. And Stephen is running this business at Andheri and making same 2.07 lacs a year. The value of 25K what is shown in Jatin’s business is grossly understated. Isn’t it? We call these type of situations are special situations.

Smacked down, just now we described my strips of concentration or I love to call them concentration bands. For me these are six characteristics if a business manage there is no reason why wont my investment deliver a return superior to fixed deposit.

Few terms in investing to connect the dot: the 814% return we spoke is known as ROE (Return on Equity), the 2.04 lacs my share of earnings is called EPS (Earnings Per Share). The two most important terms that drives equity investment.

Just to recollect:

- We are buying a piece of business with some one like Jatin to share his earnings.

- We expect Jatin to be man of hard work and integrity and he will protect my piece of business as he does for his own piece.

- We expect Jatin to manage operations as good as finance and compliance and also have an eye on future (strategy).

- We think Jatin has enough fire power which makes feeling he will do well like expansion etc.

- We are paying some money to Jatin for buying business, it does left something for us as well. We shouldn’t land up paying so much that we don’t get anything.

- There are something we and Jatin know but it doesn’t show up in Jatin’s business like his stake holding in brother’s business. Sometime Jatin may not be knowing and we come to know.

There is another way of looking at business or tedhi soch. As we said investing is all about sharing earnings. Let us ask ourself few basic questions:

Say Jatin is a sleepy guy but his masala is so popular it doesn’t matter. I call them as “enforced earning driver” without any intervention of anyone. And classic situation of user oligopoly.

We are expecting Jatin to take certain steps like negotiating with vendors and customers to make sure earnings goes up. Let us call it as “voluntary earning driver”.

Now find out a company where 60% of revenue comes from enforced earning drivers. You just hit a 100 bagger! Click a button in 2016, cash comes out till 2026, wonderful. Fine, let’s break our wish list and get into real world.

How do arrive at enforced and voluntary drivers. They all reside within six concentration

bands, only we need to twist our thinking (tedhi soch)

Once again I will be using these words heavily going forward, next dozen of writings will be execution heavy.

First band of concentration- Competitive Advantage

Second- Quality of Management

Third- Risk Management Capability (Financial, Operational, Compliance and Regulatory)

Fourth- Future catalysts

Fifth- Margin of safety

Sixth- Special Situations

End of story for now, but quite unfortunately not all businesses are vada pav nor every one is Jatin. That’s where we need to work hard to find out, but our objective remain same that is : ( A REPEAT FROM TOP).

Now, if you want to buy a piece of business then there is only one question why I want to buy piece of business? And there is only one answer, to share the earnings of company. That’s it, all our effort going forward is to ensure and know how company is going to earn higher and higher.

If you go above we said there are four parts:

- Create a portfolio

- Fill up with right quantity and quality of equity shares

- Protect them with due care and diligence.

- Create wealth by selling, re-allocating and distributing

What concentration bands we discussed is only to know we are going to put good business into portfolio. To get answers for A-D we must know:

- how many businesses we must hold?

- how do we track and protect them?

- how do we create wealth?

The subjects are embedded to portfolio management. After knowing business requirements we will get into them. But believe me bringing or buying good business is toughest part, a mis managed portfolio may bring opportunity loss but not permanent loss of capital which can happen by buying bad business at bad value.

Next we will discuss the first concentration band or business requirement called “Competitive Advantage”.

Also I have a request, if there is a short cut way of knowing “future earnings and protected” please let me know. We need not have to do all these drama at all. All six band drama is to find them out reasonably.

Before I sign out just wanted to pin down an example to show magic of equity:

Assumptions:

- Year 2,3, 4 price per vada pav plate becomes 50, 60, 70 for 250, 300 and 350 customers per day respectively.

- I have given a 25% hike to both entrepreneur and staff!

- I am using capex cycle for fore casting, this means after four years new asset replaces the old one. Hence no capex till date.

None of these are absurd assumptions, you can say optimistic. So imagine when you become optimistic with a CEO like Jatin and good masala and decent customers I make 204% CAGR every year which makes 25000 Rs investment to a mind boggling 21.35 Lacs in a matter for four years only. Welcome to fascinating world of value investing!

Thank you so much for nice words, warm wishes for wealth creation.

11 Likes

This is most simplistic way to explain Business. great going indeed!!

That would be great reference material for future . Thank You in advance

@suvendurath ji

Take a hypothetical stock X. It’s in a profitable business (ROE>25; ROCE>50) and able to grow the business. Dividend payout is around 15-20% so able to invest the profits also. Management is also good. Lets say the business can grow at 14% CAGR for the next 8 years. Further lets say it has a semi-unique product and thus not much of competition. Obviously Mr. Market is not a fool and assigns a PE of 60.

Can I buy the stock now? Obviously buying “cheap” is a better option or wait for a correction which might not happen and thus the associated opportunity cost.

Thanks a lot for all the gyaan. Much appreciated.

Ashwinji

First thanks for trusting me to answer the question, second it looks like you made lot of thoughts putting behind right parameters.

Let’s come to your question straight away i.e. buy price.

There are two ways to value the company 1. Relative Valuation i.e understanding and making a sense of market price from fundamental parameters. This means we use a fundamental attribute like EPS and a market attribute like market price. 2. Intrinsic valuation or a business valuation. This method ignores completely market price and try to estimate a valuation based on company numbers and fundamentals only.

I would prefer to use intrinsic valuation and support by a relative valuation to get comfort.

If you want to use a relative valuation then you can try this:

- Take average PE of last ten years than current PE

- Use previous 10 Year book value growth as a estimation for EPS. Book value is our portion, the equity value of company.

- Discount future value to CMP to find out a expected return.

Say Average PE is 35, 10 year book value growth- 20%, Current EPS is 30, CMP is 1000.

If we compound EPS 30 with 20% book value growth for next ten years future EPS value would be 185.75.

http://www.investopedia.com/calculator/fvcal.aspx http://www.investopedia.com/calculator/fvcal.aspx

Multiply future EPS value 185.75 with average PE of 35 we get 6501 expected value after ten years.

if we discount back 6501 to current market price of 1000 around 20.6% CAGR. That means we will get 20.6% return per annum for next ten years against 8-10% of fixed deposit or corporate bond rates.

A caution: these valuations are good to use at entry stage. But unless substantiated by intrinsic valuation which is derived from business itself may be misleading due to the fact future is likely going to be different. It may maintain growth rate, but understanding that growth drivers comes from nuances behind financial numbers.

I will cover intrinsic valuation under margin of safety.

5 Likes

Guru Mantra 15- Competitive Advantage: Racing for Uniqueness (Part I)

Note: this section is bit academic heavy and will be so for some more time.I have tried to use simple words as much, but without understanding concepts behind business and industry its going to be extremely difficult to find out a competitive advantage for company. In later part we will talk about how do we find them from financials and other places. But we will not able to connect the dots unless we understand economic behind such thoughts. Further despite after all these years I understand very little from business strategy, perhaps 10% or less. This is a sincere attempt of offloading the same, apologies in advance for major errors, please do rectify. Happy to include into my practice notes.

If we revisit our understanding about nest building last time we just want to buy company who will produce earnings either at same speed as past or accelerated. Past may not be fool proof indicator as competitor comes in eat away my business earnings.Earnings is that portion of money which is available for shareholders or Earnings Per Share. That pushes us back to think how do we know a company will protect its earnings from competitors for a long period to come? To understand this better we need to go back to history.

Graham, Buffett and Greenwald

Benjamin Graham gave all of us idea that you buy the company if its available less than asset value more specifically net current assets. Buy them and sell them after they spike by 50%, in the process he landed up in buying few hundred shares. Ben Graham didn’t care for much whether company is good or bad, management was poor or better.

Buffett realised during 1970’s that few of Graham companies had gone bankrupt after we sold them beyond a valuation. That forced him to think companies need to stable and at good hands to deliver return, he couldn’t find much companies who survived for a long period. The quest led him to coin a word called, “moat”. As per him moat is the one which protects company from competitors with defence mechanism. Imagine you have a castle which you want to protect from enemies. You may load with water, add crocodiles, make it on top of hills (some of these can be found in real life in Jaipur). In investing sense he started searching for three things:

- Unique product

- Unique Service

- Better Cost Producer

He also wanted to focus on a monopolistic situation which he can understand. This made him buying a bunch of product companies which defined the life style of Americans like Coke, Gillette, Hershey or services which are integrated like Washington Post.

Graham and Dodd wrote security analysis which gave us idea to look at business valuation in tandem with:

Buy at asset value (reproduction, we will touch upon this with margin of safety; this is competitor price tag to buy assets)

Earnings power (how much capital I need to justify the current earnings)

The value of earnings growth

Bruce Greenwald is a passionate professor who spend a lot of time after cracking security analysis post Buffett era. He used both security analysis and moat to propagate a concept which says:

Use reproduction value of assets (same like Graham and Dodd)

Estimate the earnings (again from Graham)

Compute franchise value (he felt if earnings potential are higher than asset value then company is using a moat which gives the extra power. He call it as franchise and tried to value that).

Influence of Charlie Munger

Buffett moving from traditional Graham theory to moat evolution has a lot to do with his partner Charlie Munger which he accepted on public forum as well. During multiple speeches starting from late 90’s at various university, few books authored later on Charlie spoke about multi disciplinary way of managing investment. Charlie advocated on basis that the traditional education doesn’t teach us all that we require to manage day to day work including investment. He was of opinion we need bit physics, economics, chemistry, finance etc and utilise them while investing to a business. Famously he adopted the word mental model and called “network of mental models”. Mental model is a concept as old as 140 years advocated how do we perceive real world by classifying different relationship of particular subject and a persons acts and consequences. In simple word it was psychological tool to think systematically about a subject and seek means of improving it.

Mr. Munger spoke in length about various subjects with their application, a lot of them you can read from Poor Charlie’s Almanack, The Worldly Wisdom and many other books.

Business Strategy

Michael Porter the professor from Harvard Business School chase the word strategy all his life. Strategy as we all know is a an action plan to achieve our objective in long term. Apparently one of the most profoundly used word from home to parliament. Even people sells strategy consulting commands highest respect and money as well.

Prof Porter in famous thesis competitive strategy backed up second sequel competitive advantage spoke in length about value chain of industry, the drivers behind such value chain and nuances of those drivers. Ostensibly the popular usage of word competitive advantage, credit goes to Prof Porter only.

But before I get overwhelmed by Prof Porter, it has a second side too. Prof Porter with equally another genius Mark Fuller created a strategy consulting firmed called Monitor group. Their first assignment was Libya with Mr Gadaffi for transforming country. Not only Gadaffi sir went to oblivion but Monitor also filed for bankruptcy in 2012 and subsequently acquired by Deloitte group. Hence the application of Porter’s thesis remain questionable though widely used.

Chan and Renee both INSEAD guys came out with another business strategy landmark in 2005 called Blue Ocean strategy which analysed 30 industries , 100 years and 150 strategic cases to find out uncontested market places. Of course it did not went scot free without criticism, but Competitive Strategy and Blue Ocean Strategy have been two successful models among billions who chased and are chasing the elusive term strategy.

Fair enough, we are retail investors; we don’t want to be Prof Porter and neither we are going to Harvard. All we want to protect our business from competitors, the concepts unfortunately lie within business strategy. We need not follow completely but basic understanding is a must to survive.

But few bold lines again:

Moat is not competitive advantage, may be a small subset of it.

Mental models are no way competitive advantage. When someone calls network effect or switching cost as mental model they are doing a disservice to Prof Porter. All these words were coined and used by Prof Porter only. Mental models are psychological application to find out situations and solutions, suggested as one of method. This happens to got popular with Charlie bringing on to table. No one knows how many others outside a section of investing fraternity even mention about mental models._

Competitive advantage is a business strategy term used by all stakeholders of business value chain including investors.

Competitive advantage is not something always management is good at, rather it is embedded to economic fundamentals, a link between value I create and how I perform.

Then what is competitive advantage:

** everything I write today comes from 1500 pages two book sequel from Prof Porter.**

Unfortunately Prof Porter theory was very complex, even the managers who wanted to adopt was finding out very tough, still now! We continue to struggle to adopt many of his concepts. Let us try to roll his words what ever we can but with a focus on our objective, “we want to find out those facts which creates a protection for company in grow it’s earnings”.

There is going to be competition within businesses which will require a strategy to conquer. Competition is not “being the best” but becoming unique. Competition is not a direct contest between rivals but a broader struggle over profits, a battle who will capture the value an industry creates. The value I create is my Profit and Loss and competitive advantage is used to perform better. Competitive advantage is doing differently from rivals.

Understanding of Competition and Competitive Advantage

Let us repeat competition is not war fare but creating a unique value. War fare destroys value, competition creates value. As Prof Porter says creating values, not beating rivals is at heart of competition.

How do we know where does superior performance comes from? One is from structure of industry where competition takes place. Because this decides the how the value is created and shared. This is where Porter Five Force comes from which explains industry structure and profit an “average company” can expect. Second leg is “company’s relative position” within industry. A superior position will allow make company to exercise better choices.

The difference between “superior” and “average” companies within same industry traces back to steps taken by company and these “steps” or “strategy as per Prof Porter” are called competitive advantage. It took me 29 readings on 258 pages to understand this. Pretty sure I am a dumb!

Prof Porter said, “strategy explains how an organisation faced with competition, will achieve superior performance. The definition is deceptive simple” yet The Economist magazine all most call me short of megalomaniac!

When everyone jump in chasing same customer the situation is called competitive convergence, all business looks like same which My Guru called earlier sick company. The other important point is customer value may not be company value. For example when competition is limited as a customer you have pay too much extra which something you don’t want. On the other hand company will enjoy but may not be for long as other’s will start joining the race.

Competition should be unique

This is about choosing a path different from others. Let me try to Porter’s example in Indian way. Assume pre-Shatabdi express days between Bengaluru and Chennai. If you want to go you have to spend a full night on train or take a flight, land outside city and drive back and pollute by burning fuel as well. Now Shatabdi starts at 6, by 10.30 I can get down at Bangalore Cantonment and 10.50 I am at MG Road which is my destination. You start at 6 in Chennai to catch a 8 O clock flight, land at 9 and reach ultimately at 11 in MG Road. Does this theory work between Bangalore-Delhi (2200 Kms), no. Shatabdi express is a unique competition, its not competing with airlines or buses but offering it’s uniqueness with added comfort.

Becoming unique is not easy, identifying and executing strategy is not easy either. Otherwise Mckinsey, Bain, BCG, Mercer won’t be charging us a bomb and highly respected as well.

The roots of superior performance lies within 1. Structure of Industry 2. Company’s relative position within industry.

Structure of Industry- The Five Forces

This is nothing but competing for profits within a industry, not between rivals but involves multiple players, let us understand. There is a competition with supplier, customer, substitute and so on.As Prof Porter says “the real point of competition is not to beat your rivals. It’s to earn profits”

Porter developed a five force which basically tells how the industry works and creates and shares value. What are these five forces, just the names now:

Force 1: Threat of New Entrants

Force 2: Bargaining Power of Suppliers

Force 3: Threat of substitute products or services

Force 4: Bargaining Power of Buyers

Force 5 or Core Force: Rivalry among existing competitors

Few misconceptions which we also keep singing day in and day out:

Same forces works for all industries, their relative strength may be different.

_Industry structure determine profits- there is nothing called high growth or low growth _

industry, high tech or low tech, heavy or light regulations. Structure trumps these factors.

Industry structure is surprisingly sticky.

What is industry structure?

Just to repeat five forces framework explains the industry’s average prices and costs and therefore the average industry and profitability we are trying to beat. To know more about Porter five force google, you may get more than a billion pages.

More powerful the force it will exert more pressure on prices and costs both which will make industry less attractive. The hear of business equation remains that is profit!Profit comes after deducting expenses from income, isn’t it? Think expenses are resources used in competing including finance costs, this will transform the industry to create a value. Income reflect how customers value our offering and compare with alternatives.If we don’t create values for customers our income will never costs. Now if a industry creates a lot of value structure becomes critical in understanding who can capture it. A lot of value for customers and suppliers may leave the companies earn little for their efforts.

Joan Margarita of Bain and Company brilliantly expanded once in her speeches, book and article:

When threat of entry goes up, profitability goes down because incomes goes down and expenses goes up.

When supplier exerts more power, profitability goes down because expenses goes up.

When buyers exerts more power, profitability goes down because income goes down and expenses go up.

If substitutes become plenty profitability goes down because income goes down and expenses goes up.

When rivalry becomes intense profitability goes down because income goes down and expenses goes up.

If you look at statements suppliers are only force having an impact on expenses. All others work on dual levers i.e. cost and profit or income and expenses.

Understanding your customers

If you have powerful buyers they will use their clout to pull down prices and demand. Now guess I am selling tooth paste , buyers are limited either Colgate, HUL or few others which will dictate the pricing, thats what they do actually. Most of soaps for HUL is manufactured by small players, pricing and branding is done by HUL; this leaves mark up pricing for small player. If you put the situation on HUL side, it can bully any small time players.

Understanding channels as to how products are delivered can be important to understand customers powers more so when these channels influence customers. For example investment advisor have enormous power in influencing a common man as to which financial products to buy. You can understand now how investment banking are making a moolah.

We might come across cases where segments of customers are less negotiating particularly when they are price sensitive. And this works when products are undifferentiated, expensive to their income. For example you are buying an airline ticket , how does it matter to you which company to use. Or you are buying a LED which is a important decision and substantial investment, we all become price sensitive.

Now take the reverse situation, you are going to buy toilet cleaner; will you bother about cost? Or you want to buy an Apple product, you wont mind paying as you think Apple itself a prestige for many.

Sometime the product becomes mission critical, for example you cant build a house without electric switches,even if switches cost a fraction of apartment cost.So Havells keeps adding teaser price, you continue to ignore them.

Understanding the suppliers

Suppliers can charge higher prices and ask for favourable terms. Hence suppliers capture more value from industry leaving less for others. Example would be perhaps Intel who keep on bull dozing lap top guys. Even the bargaining power of labourers like trade union can be dangerous. That’s why software is a preferred investment decision than tea or sugar.

How do we know the suppliers exerting power?

Check whether suppliers are large and concentrated in industry in terms of percentage?

Whether supplier needs industry or industry needs supplier? For example for guys like Premco Global who makes elastic they need Jockey to survive not other way.

Switching costs are costs (financial and non financial) when you choose one products or services over the other which you are already using.

Switching cost tied to suppliers, for example products like ERP where so many things are interconnected its not easy to switch. One of them is need and investment, I wrote sometime back, here is the link:

Anywise we will cover some of these key terms in detail later as well.

Now If I am a soap manufacturer then I have to sell it through like someone HUL or Godrej.

I don’t have a choice but to accept, as people recognise soap with them. This is called differentiation which can be real (technology) or even perceived (brand).

Also HUL decides to manufacture its own soap, this creates more panic with small guys and prices further fall.

Substitute products or Services

If a product meets same basic need of another product it can put a cap on industry profitability. For example Tax preparation software can hit practising CA’s, but we will continue to use jargons in income tax even software wont understand! ![]()

Substitutes are not direct rivals, they may be unrelated and come from unexpected corners. Sometimes we don’t spot it easily, example IPOD knocked off Sony Walkman with fan fare , little it realised all mobile phones are giving one music player as package. Of course Apple has it’s own share via IPHONE but nevertheless IPOD became unattractive.

Some substitutes have a catastrophic effect, imagine petroleum is gone and everyone started using Algae. The entire auto industry, engines, infrastructure, ancillary have to change their cars, equipments and so on.

But the substitute must offer an attractive value or else it doesn’t look like trade off. Like online video library for renting are much cheaper than buying a movie.

Substitutes works wonderful on both frequent usage and casual usage. Say you get another Gillette at lesser price or say even after you watched a movie utility is over. Both way it works!

Substitute may not be cheap always, for example luxury bus services even higher will be preferred for short distance as it offers saving of hassles, comfort and last mile connectivity.

Switching costs have a role in substitution, cigarette smoking is a such strong habit people wont even switch with lower price.

We covered three forces, two more to go. We will touch upon then Blue Ocean (contrary to what Mr Porter said) and move to what investors made out of these strategy more importantly Mr Pat Dorsey. Finally we will end competitive advantage as surveyors, how do we hunt them from financials and other places.

Thanks once again for giving me an opportunity to write. I hope you do enjoy as I am enjoying by writing, checking and collating.

14 Likes

Guru Mantra 16- Competitive Advantage: Racing for Uniqueness, Part II

First we will capture key concepts from last episode:

Every industry have it’s own structure which Mr. Porter said Five force drives it. Actually buzz words like switching cost, network effect, cost advantage are all part of five force theory.

Within an industry a company stays ahead of others (or relative positioning) by taking some steps which is called competitive advantage.

Competitive advantage helps a company to be unique not starting warfare with another.

We spoke about three out five force last time Bargaining Power of Customers, Bargaining

Power of Customers, Threat of substitute products. Fourth force is:

Threat of New Entrants

Here though Mr Porter included new entrants as weapon, the subjected has been debated long time ,right from days of Joe S Bain through his famous book, “threat to new competition”.

We want to protect new entrants for the simple reason new fellow will add capacity and seek to gain market share. This in turn will hit our profitability by caping the prices (price war) which makes price unattractive for new comers to make an entry. And at the same time the incumbents have to spend more to satisfy the customers.

- What are the typical entry barrier for a new comer?

- When we produce more does per unit cost also goes down? This is called economies of scale, what happens the fixed cost gets distributed over larger number of units which ultimately pulls down the cost of production. Or may be we are using new technologies which is driving costs down or you are exercising bargaining power of suppliers, negotiating costs through volume.

- Does my customer have a switching cost from moving from me to someone else? We discussed about switching cost last time, we will come back later as a stand alone subject.

- Does my value of product goes up when more and more people started using? This is called as network effect. Like telephone, we need to two telephones to talk to each other. Sometimes value comes from size of network like commerce guys like flipkart, snap deal.

- What is the admission price for a new entrant? This include capital investments, mental hassles etc? Classic example is Pharma, you spend billions for research and get rejected finally.

- Do I have a proprietary technology which restricts new comer like Apple, locations, distribution channels like Asian Paints. The distribution channel is a formidable barrier when especially customers are locked up.

- Does government policy restricts and prevent new entrants? Like liquor license in Tamil Nadu.

- What would be retaliation when a new guy enters? Imagine a cab aggregator arrives tom, Uber will make your all ride for a week free.

The last element connects to four forces to single thread of competition.

Rivalry between industries

When rivalry is intense profit is lower like FMCG. Buyers get benefited by lower costs. Rivalry happens through price, advertising, new product, increased service. Drug companies may be spending a fortune for research but they don’t fight on prices. But if you look at e-commerce their sole way of fighting is price.

How do we know intensity of rivalry:

- There are many competitors which are roughly equal in size. If you have a clear leader like ITC it will dictate the pricing.

- If there is slow growth it provokes battle over market share.

- High exit barriers prevent companies from going out which kept on adding to already burgeoning over capacity.

- When earnings is over ridden by emotions something like national pride, Air India?

- When customers have low switching costs, this will drag the prices down.

- Fixed costs are high, we need to have volume to cover this fixed cost. One way of having volumes is to drop prices.

- Unwarranted capacity addition left and right.

- A product which is perishable, this doesn’t include fruits etc. but hot fads going out quickly like garments, hotel rooms.

The impact of five forces on business strategy

Industry structure decided how the economic value created by industry is divided, how much is captured by companies, customers, government, suppliers, distributors, substitutes and also potential new entrants. Five forces can be connected to Profit & Loss and Balance Sheet.

Mr Porter provided a holistic way of tagging five force to financials.

For any industry let us understand the scope by way of product and geography.

- Identify the players for each five forces and where appropriate segment them to groups.

- Assess underlying drivers of each force like strong, weak.

- Identify which forces drives profitability.

- Analyse changes or likely changes to each force.

Joan provides few model questions to help us:

- why the current industry is profitable?

- what’s changing in profitability?

- What are the limiting factors?

The real point remains, earning profits; not taking business away.

Let us not get carried away by these jargons, once we connect in table format much easier to follow. I will paste a table once we complete competitive advantage.

The Competitive Advantage

This is trump card of Prof Porter’s theory, but without understanding five forces above we wont be able to spot competitive advantage.

If you have a real competitive advantage you can command a higher price and operate at a lower cost at same time.

Competitive advantage about superior performance. One of the best measure of capturing performance is ROIC is Return on Capital Employed. It basically compares all profits generated against all funds invested including expenses and capital. As per Prof Porter ROIC deals with creating value for customers, dealing with rivals and using resources productively. ROIC varies industry to industry, for example in a metal company it takes around 8 years to bring a new plant in line where as in service business you can barge in within a year also

We should compare ROIC with guys within same industry. If you have a competitive advantage your profit should be higher than industry average.

To know the nuances we need to break down the components, let us remember two most things drive profit is price and cost.

Pricing Power

A company can charge higher price if it offers something unique and valuable to customers. Economist call this is “willingness to pay”. A consumer’s willingness more likely to have an emotional or intangible dimension either through a pride or brand or even a status associated.

Relative Cost

The cost advantage comes from lower operating costs, efficient usage of capital including working capital or both. Sustainable competitive advantage involves all parts of company not just one function or technology.

The Value Chain

We must repeat competitive advantage is a superior performance resulting from higher prices, lower costs or both. So its not about switching costs or network effects which are structural components of a industry. But we must understand the source of competitive advantage, these are things which management can control. And management controls lots of “activities” which ultimately drives a cost or price or both. Activities can be sales, procurement, marketing, finance and so on. The sequence of concept to produce to sell and receive cash is called as “value chain”.

As investor we shouldn’t go into strategy and non core competence to know the exact source of value chain drivers, rather what we can do is:

-

Map the company activity from concept to sell to collections. Compare key activities with competitor, if you can do upstream and downstream it would be better.

-

Let us stop here, for band 1 stock which is around 14-15% of my portfolio what I do is:

- I take out all significant items (more than 5% of PL, 3% of BS) from financials and list them like sales, purchase etc.

- I start connecting elements between themselves to know which department is feeding a financial figure. For example purchase, stores, factory and finance are the ones who are key players for procurement.

- I compare this processes to a competitor to see whether additional value chain is hitting the bottom line. Comparison is not on names but on numbers. Example company A does not have a quality department where as B have. Can this missing component have an impact on profitability?

- Start thinking can you miss one step and still maintain the value chain. For example measuring options between out sourced customer service and in house.

- Focus on key cost drivers, more so where expenses is rising.

The competitive advantage comes from analysing the value chain or key process of company. More information you can gather from financials or some where else it will help you analysing better. I try to do mostly number crunching (will cover them in Risk management section) but still its one of toughest job for me.

Knowing a switching cost, cost advantage or network effect is not competitive advantage but its important to know where the advantage is embedded to value chain or process. And this is where experience, circle of competence comes handy.

Mr. Porter further provides on guidance what best strategies can be executed by management to stay ahead of the pack to meet the gold standard of competitive advantage.

-

a distinctive value proposition (ask questions which customers you are serving, which needs are you going to meet, what relative price is acceptable- basically need and price). Prof Porter gives an example of Indian case Aravind Eye Hospital. He says this hospital have an extra ordinary value proposition. One it targets affluent customers for those who can pay. And at the same time who cant afford the hospitals offer sight with same infrastructure but with stripped down price. Perhaps the same strategy is adopted by Narayan Hrudalaya.

-

a tailored process or value chain (processes are build over time, there is no single size fit for any company. So when you see an acquisition case, you should be extra cautious, the whole value chain may collapse and drag down both companies who married.I was trying to peep into Narayana’s operating style. In one of speeches Dr Devi Shetty says when one patient is getting operated the next patient is ready on a table behind him. The moment one operation is over surgeon moves to next! This has created a standardised process even in one of most intellectual and highly subjective industry like medicine sciences. We can see the number of massive number of operations Dr Shetty and his gang makes a year. He charges who can pay , lower the cost and partially pass the benefit to who can’t pay. It will be interesting to see though how Narayana is unlocking earnings through this model)

-

trade offs different from rivals (more is not always good like selling more services or products. If you take one path sometime you cant take the other, and still you remain hugely profitable. For example all airline have their own routes, it gives them choices to focus on their routes doing at a lower cost. Trade off arises mainly due to product features may not be compatible e.g. you wont enjoy buying 500gm milk packet in a huge Reliance Fresh. Secondly trade off within activities e.g. small lot size of products may be less efficient for large plants. Last is inconsistence in reputation e.g. Maruti producing bicycles.)

fit across process or value chain (the processes should be interconnected within themselves well. For example Flipkart wants to lower the costs, then it has to use inventory in a such location which is outside of city bringing down inventory carrying cost. At the same time deliver happens from same place which makes the sales cycle faster. For example Big Bazaar initial days when a customer asks where is a given item, Mr Biyani strictly instructed staff to accompany customer rather than giving a direction. He was desperate to negate the idea, too big shop to shop!) -

continuity over time (this is all about change management, good to have plans but has they been challenged and effective over time).

We come to an end as how Prof Porter conceptualised industry, its forces and competitive advantage around value chain or processes. I agree if you think, this is not so easy to correlate while analysing a company. But people like Pat Dorsey categorise the concepts into making easy for investors. Yet if you want to dug a competitive advantage one has to understand processes and strategies around it. And that’s never going to be easy, hence claiming easily a competitive advantage is half hearted attempt in building another Taj Mahal!

Next lets talk about Blue Ocean, which is quite inverse thinking. I think if we can apply

10% of Five Force and 10% of Blue Ocean it makes us a decent investor.

Thank you.

11 Likes

just joined the forum and by chance came to this thread . Most fulfilling superb and mesmerizing . Thanks suvi.

This is like Gold Dust! I’m so hooked on to this.!

Thanks & Appreciate the wealth of information &knowledge imparted

Regards

Mahesh

Interlocking Business Strategy and Competitive Advantage

Legendary management consultant Bill Bain (Bain & Co) not only challenged Marvin Bower (Founder of Mckinsey & Co) on his home turf, but at same point time it was a awakening for his mentor Bruce Henderson (the founder of Boston Consulting Group). Henderson and Bain has been instrumental writing down interconnected dots of business strategy and competition. It’s always wonderful when practices comes out of academics. Bruce Greenwald and his team redefined the way of looking at franchise based valuation but before that he has worked extensively on competition, an edge on same.

Below is a compendium inspired by Bill Bain and Bruce Greenwald.

Bill Bain propagated if the there is a level playing field only way you can roam freely without bleeding is having operational efficiency. This would mean all competitors have equal access to customers, technologies and other cost advantages. If someone becomes smart and does something different then immediately it get copied. The imitation continues till the time economic profit becomes no more lucrative. But Mr Bain pointed out operational efficiency is a matter of tactical weapon not a strategic move.

Lets flip the side, where multiple competitors have advantages (competitive advantage) then its about managing their edge. If few incumbents are there that’s where enterprise create a value for a sustainable period. So we should look basically an area with few super guys who are far ahead of clock, not an easy thing to get but not impossible.

Prof Porter’s ground breaking study gave us a definitive direction to look at, but the question remain which is strongest force among 5, which is weakest. How does the force connect to value chain of an enterprise and subsequently an investor can reach a plausible conclusion on his buy, sell or hold.

Bruce Greenwald emphasises that barriers to entry is one of most structural force to watch out and gave substantiation to support it. Pretty clear unprotected industry will be fought to the wire when economic profit becomes insignificant. If you do not have an entry barrier what’s left to the firm become efficient and be on toes.

Look for incremental expansion

With increasing global environment trade barriers are getting non existent. But does that effect in local circumstances? Asian Paints first started in pockets of India, tested before expanding big time. It expanded incrementally outward from the geographic base, add new distribution system and prototyped the competitive advantaged learned as it progresses. Watch out for dominance by a single company in local arena with small number of less equivalent firms e.g. PC Jeweller. Dominance at local level may be easier to accomplish than at global level.

Impactful competitive advantages

Greenwald advocates there are three type of genuine competitive advantages. On supply side you have strict cost advantages where I can produce lower than my peers. This can happen due to privileged access to crucial inputs like mining minerals or a proprietary technology which is protected by patent/know how.

On demand side few have command over market which is not matched by competitors. This may not be due to product differentiation or brand my “captivity” based on a habit or switching cost or even search cost.

The last leg is produce more, spread fixed cost over capacity; this in turn bring cost advantages through economies of scale.

Linking strategic analysis to competition

If there is competition there would be competitors. If one company dominates then others will be simply at disadvantage, they should simply get out painlessly. Watch out for sectors where companies are getting shut down, this may not be always due to bad economics of sector but may be due to one superman is forcing others to surrender. I am watching keenly whether Reliance Jio is making Aircel or Docomo out of job! Here if Mr Ambani messes up then smaller ones may get a chance, not speaking of Airtel or Vodafone.

Even when big and mighty enjoys a competitive advantage and it doesn’t have to worry about competitors still it has to manage its advantage. Watch the growth and capex numbers volume and geography wise.

If several companies have equal advantages then strategy become demanding. This gets into different ways of managing business strategy I think have little relevant for retail investor. In case you are interested I can send you a copy of his three approaches of managing equal advantages.

Summary of recommendations

- The supply advantages is competitive costs outside patent protection (e.g. process modification in speciality chemical industries which take years to amend and can not be duplicated easily).

- Access to cheap capital may no more be competitive advantage with crowd and several ways of funding available.

- Watch out for a sector where leader forcing small players to shut the shop, it will wide it’s profit network only.