Monthly Portfolio Note - April 2021

Portfolio Commentary

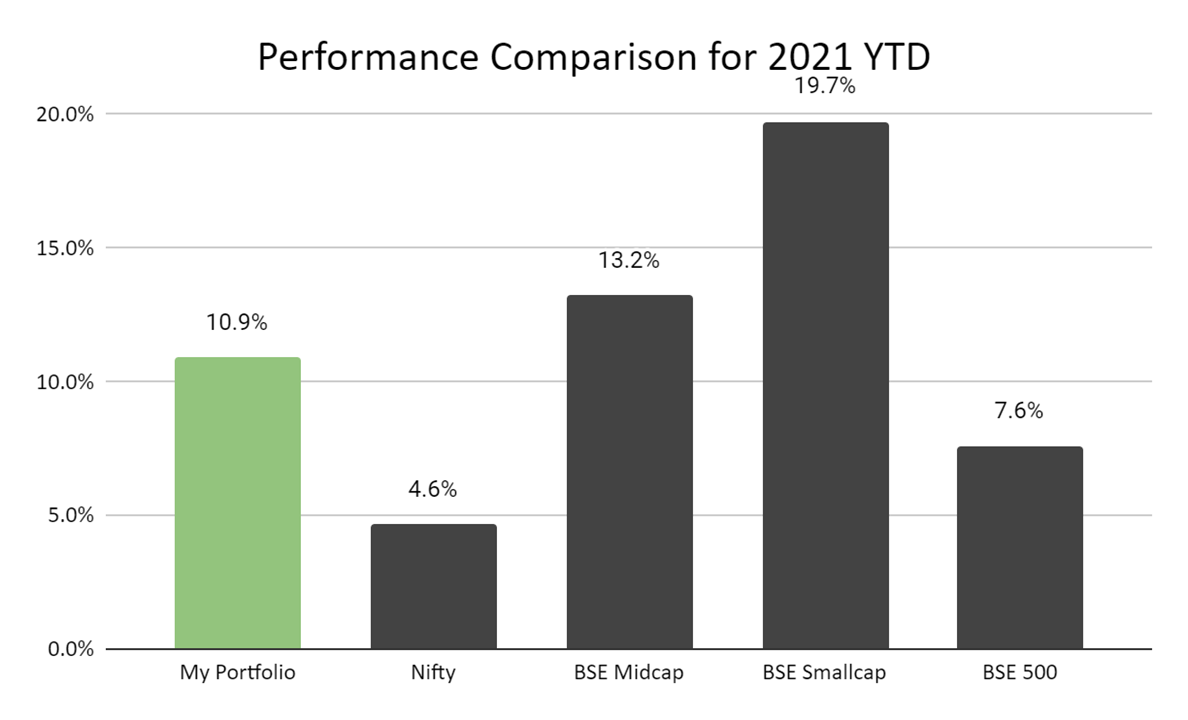

Reasonably good month and well on target to achieve 15% CAGR for the year despite the fact that 10% of my PF was invested in Office REITs this year whose DPUs are not included in the above numbers. I thought we were in for a decent correction with Covid 2nd wave, however Mr. Market is quite smart and didn’t repeat it’s folly from last year’s vertical decline. Basically, Covid is not an unknown unknown for the market anymore. Anyway, I’ve have been adding on all dips through April and trying to increase my exposure to some high beta top notch financials as they’re available at reasonable valuations. However, also meant having to exit some positions I may rather have not, details below.

Poly Medicure (minor profit booking at 4.5x levels), CAMS, Fine / Valiant Organics and ICICI Pru Life seem to have driven majority of PF gains this month.

Exits

-

Beta Drugs - Sold with 100%+ profits. NSE SME listed pharma company operating in unregulated markets. Nothing wrong with the business as such except a SME company is relatively hard to track and get good insights on with 6 monthly results and bare minimum visibility via annual report / AGM. And I was looking to raise cash to avail of opportunities during the 2nd wave Covid decline in mid-April. Big mistake!!!

In terms of stock performance, it had been in the same range for almost 4-5 months now and almost as if the stock was waiting for me to “GET OUT”, I KID YOU NOT - the stock hit 10 consecutive upper circuits from the next day onwards to become almost 3.5x from my 2x - 75% opportunity loss!

Don’t believe me, see this!

Selling is definitely not my forte yet ![]()

-

Pidilite - Booked out at 50% gains, very very small position from Mar 2020 and same line of thinking as Marico, Britannia, earlier - do not foresee 15% CAGR on long term 10 yr basis at current valuations. Happy to re-enter any of these businesses at lower valuations if ever…

-

Sun TV / Huhtamaki - Booked minor 15-30% gains, opportunistic bets in satellite portfolio. Wanted to reallocate cash to higher conviction bets

Entry / Increased Allocation

-

Muthoot Finance - New position, 2point2capital’s letter really caught my eye and I started thinking about the gold loan business. Read through latest concalls, annual reports, watched management interviews and came to the conclusion that this is a fail-safe business as long as the world lusts for gold. There can be intermittent periods of volatility in value of gold prices but there are very very strong barriers to protect the business model. Just this 1 number blew me away from the management - ever since the company got listed, not a single rupee of regulatory reported NPA has resulted in actual losses as the physical gold has been auctioned which more than covers the loan amount at 70-75% LTV incl. making charges. Although management has admitted banks / other NBFCs have also started hunting in this ocean, there are ample opportunities for growth for the foreseeable future. Also gold prices have a double tailwind - precious metal which is limited supply and long term USD INR depreciation

-

Bata India - New position, has to be looked at from a long term perspective. Footwear is an essential product just like clothes. And I was thinking about all the last few global / economic crisis of any kind. 2008 financial crisis, 2001 IT bust, 1992 Harshad Mehta scam - none of these crisis would have any major impact on Bata’s business. So whatever the next crisis will be, I’m pretty confident it will have limited or no impact on Bata unlike Covid. Now, Bata’s brand has a very strong recall and the company has been aggressively investing in growing their reach by doubling/tripling store count over the past 1-2 years. This can be a 1 lakh crore market cap company in my view over 10+ years.

-

HDFC Bank / Kotak Mahindra Bank / MAS Financial - Increased allocation, I’m very bullish on select financials to keep on accumulating market share and consolidate the very very large Indian FS market over the next few years. But need to be very selective in leveraged names. Bandhan Bank is a great lesson for me in terms of the difference in business models across banks (MFI unsecured book vs semi-secure mortgaged books of HL/AL, etc.)

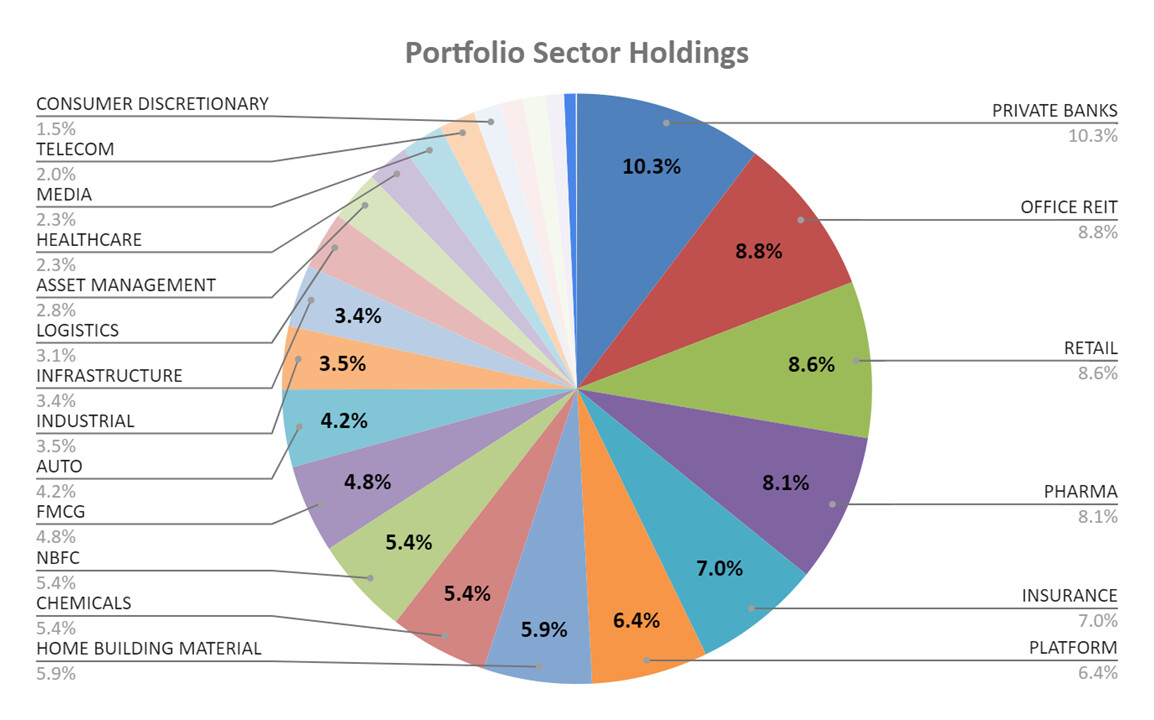

Since the number of PF stocks are more than 70, sharing a pie-chart of the holdings across sectors which helps me better understand my weightages and exposures:

See you next month!