As the capacity will increase there profit margin will improve, they will buy raw material in bulk and fixed cost will remain unchanged so overall once they run up the plant at 100% capacity, there bottom line margin will improve.

With all above incentives, company can receive ~100 Cr as incentive in a span of 3 years from Assam Plant itself. This can boost the bottom line to great extent and company can beat the grain inflation with these incentives.

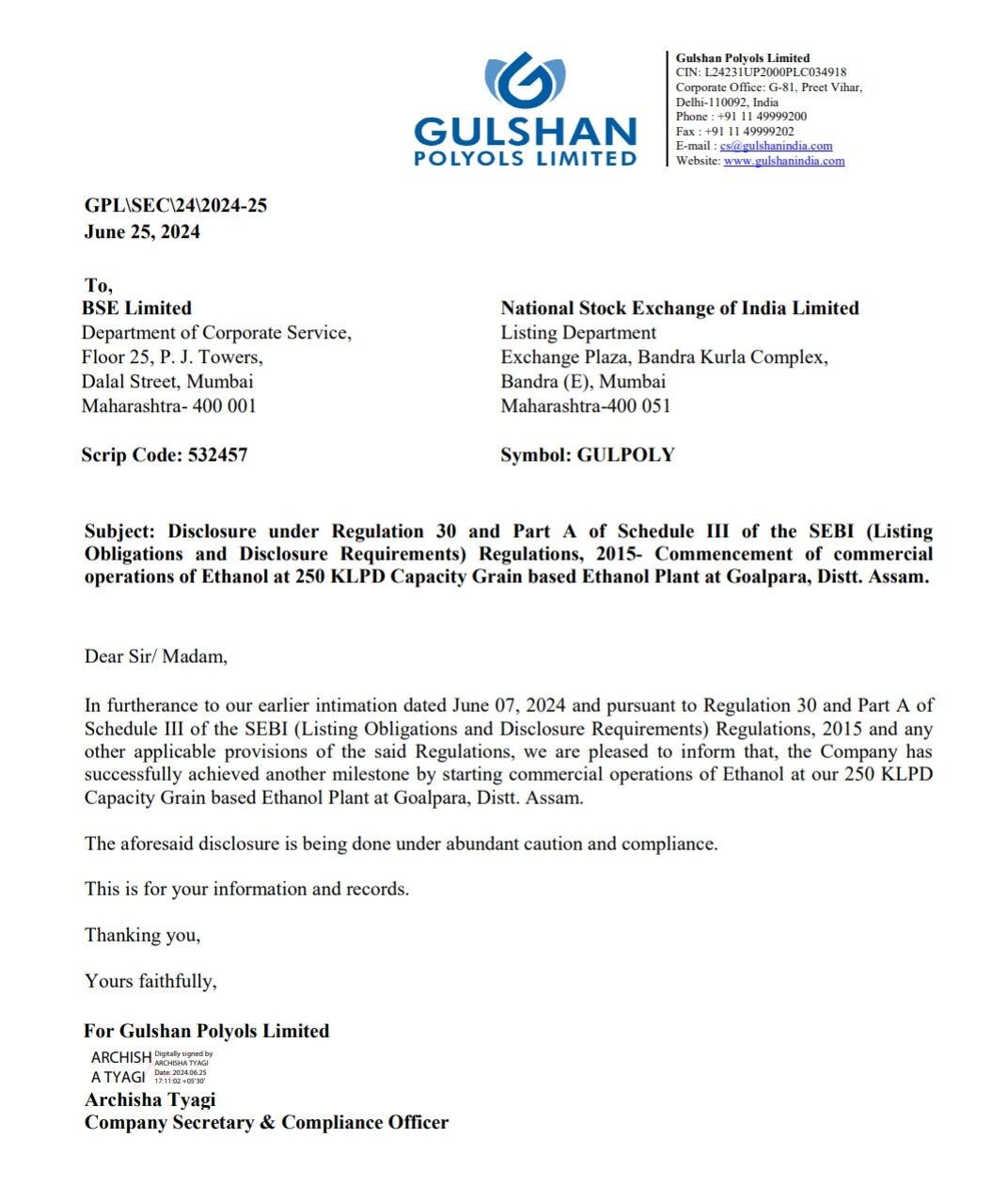

Even though Assam plant was commissioned by the June end, there is no improvement in the Top line of Q2FY25, as they said its running at 70% capacity we may expect some improvement in the numbers of distillery in Q3

2 Likes

Q3 is very good number

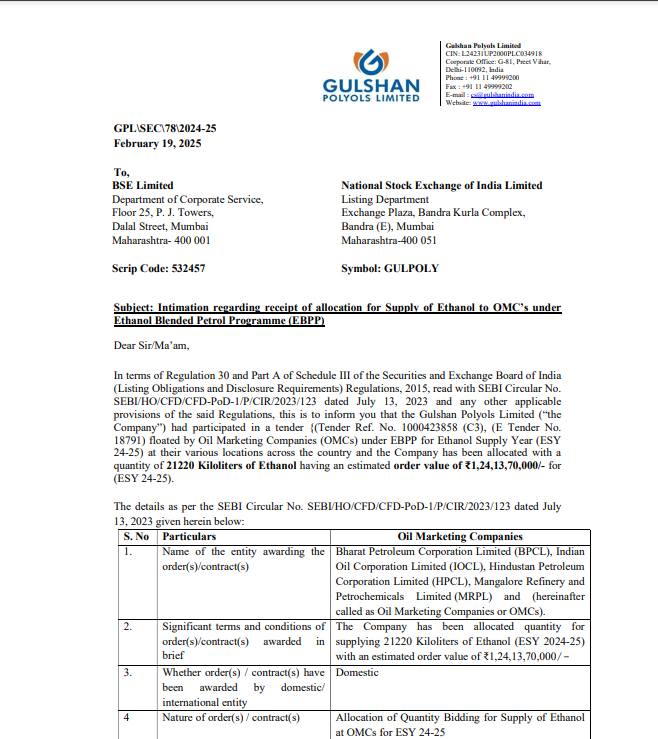

Gulshan Polyols won a tender to supply 21,220 KL of ethanol to OMCs for ESY 24-25, valued at ₹124.14 crore.

3 Likes

Hi Friends,

Could anyone explain me following points who track this stock’s fundamentals in details,

-

After GoI Scheme for maize purchases for ethanol production, has the company able to secured its RM Procurements at affordable purchasing prices, because it has been the 1 year, since the announcement of schem?

-

What type of Quality of Grain based Ethenol does Gulshan produces and who is in charge of such Ethenol Prices is GoI or OMCs or National/International Demand/Supply?

-

Is there any feasibilty if this Ethenol purachsing programme are abondend by GoI for particular period of time or for any reason, can they able to Sell Same Grain based Ethenol to Liquor companies which obviously has higher margins?

-

At what pricing Gulshan procures its Raw Material compared to its peers like BCL and others, in Q3FY25?

-

How has been their Operating Cost variations over the last 3 years and where they are finding it diffulty to maintain Good Operating Margins?

-

What about capacity utilization programme, are they going to use 100% capacity utilzation across all the Ethenol plants, be it, MP or Assam plant, because in past they were using only 50% of MP plant to supply MOCs?