Gujarat Terce Laboratories is a pharmaceutical company into manufacturing and marketing of branded generics. They are also doing in-licensing and CRAMS. The company has a basket of 50 Brands (180 products over 10 therapeutic areas) with 180 SKUs, covering multiple dosage forms like Tablets, Capsules, Oral Liquids, Ointments and Injectables.

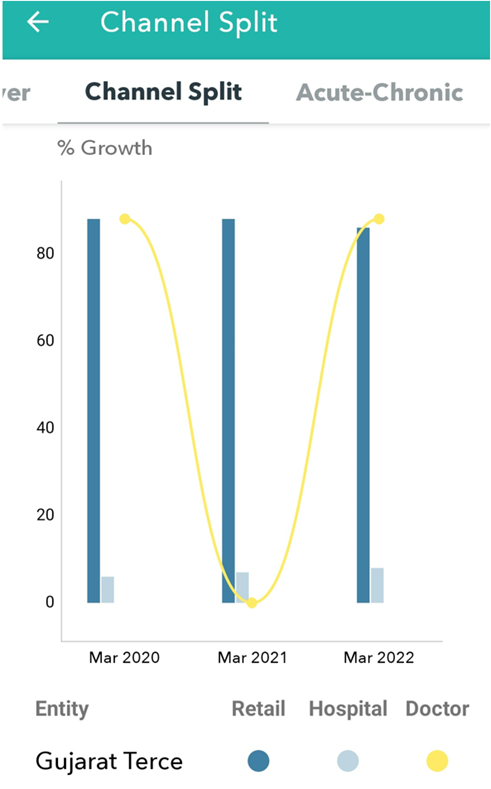

They are available at a network of 43500 + Chemists. The distribution channel split is 86% from retail, 8% from hospitals and 6% from doctors.

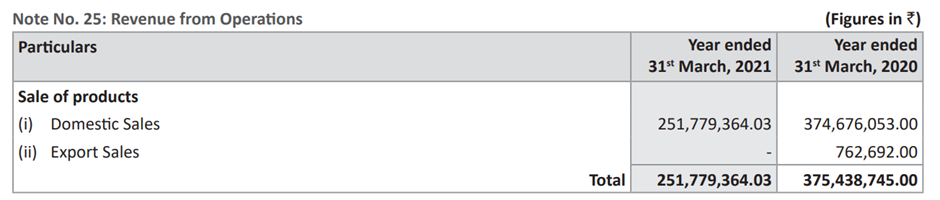

They have a fully automated manufacturing facility at Chhatral in Gandhinagar, Gujarat. Most of the revenue is from domestic sales; export is negligible.

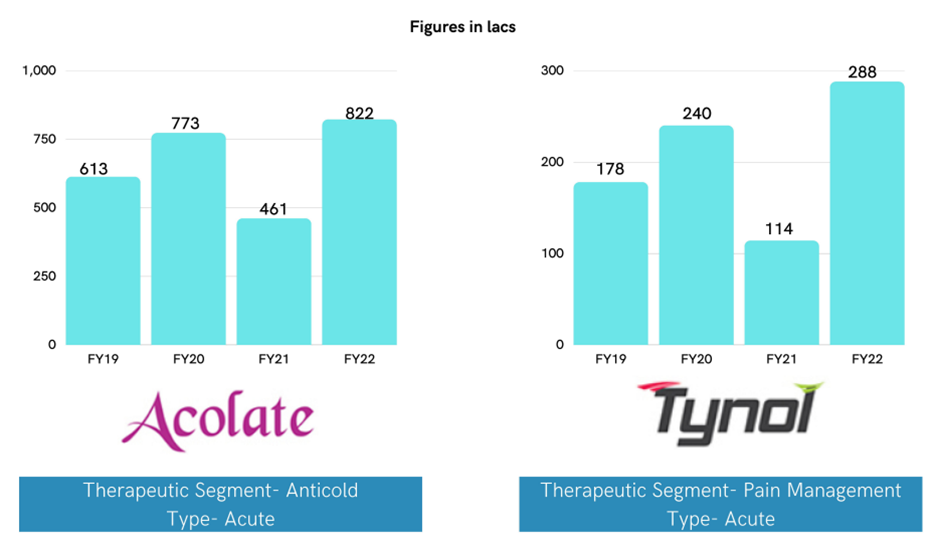

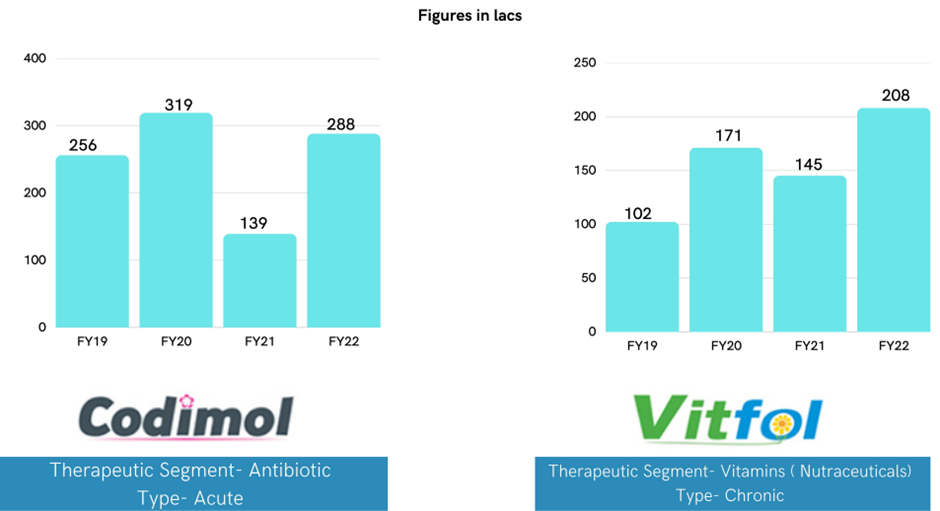

Some of their brands are:

Aziter and Ferlit are also their brands. Some of their brands are among the top 10 in their respective segments.

They have two segments- acute (around 80% of revenue) and chronic (around 20% of revenue). Acute diseases are those that occur suddenly and last for a short time, while chronic diseases are those that occur over a period of time and last longer. Rising share of chronic (potentially) could be a thesis pointer, as one generally observes repeat sales (recurring revenue) since patients need to consume these medicines repeatedly for a long time.

Out of their top 4 brands, 3 are in acute segment while one is in chronic.

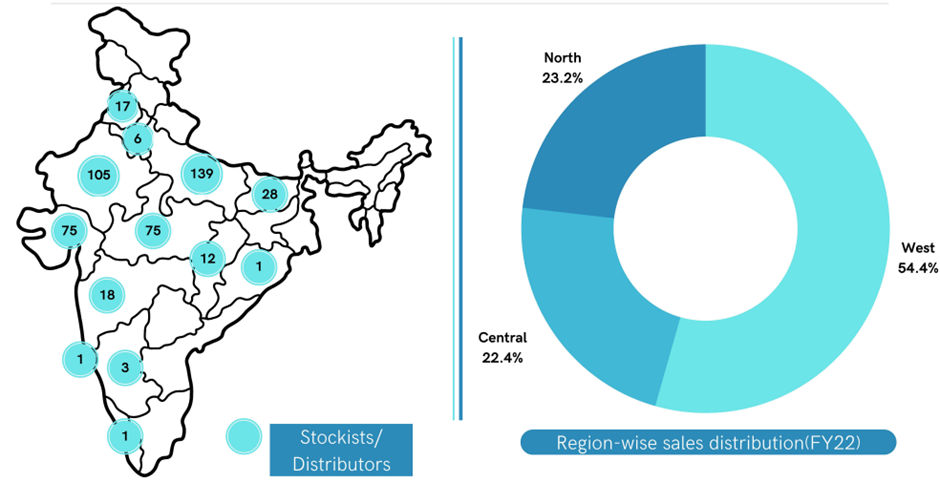

Geography wise data:

The company is among the top 200 pharma companies in India, and are aspiring to reach within top 100.

In FY20, they also launched healthcare and wellness products, which saw a good response from consumers.

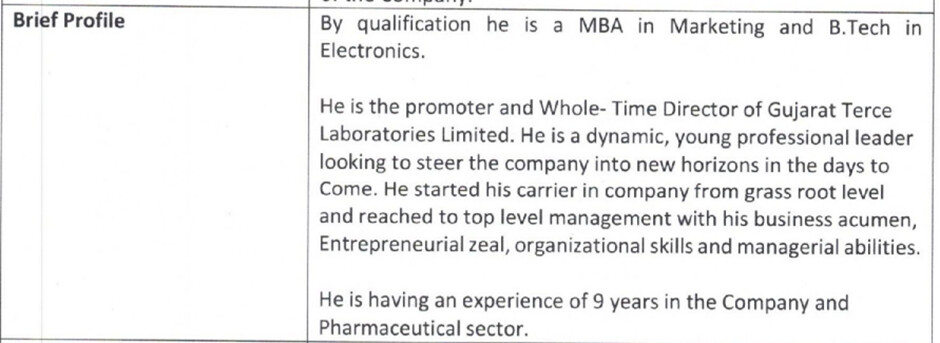

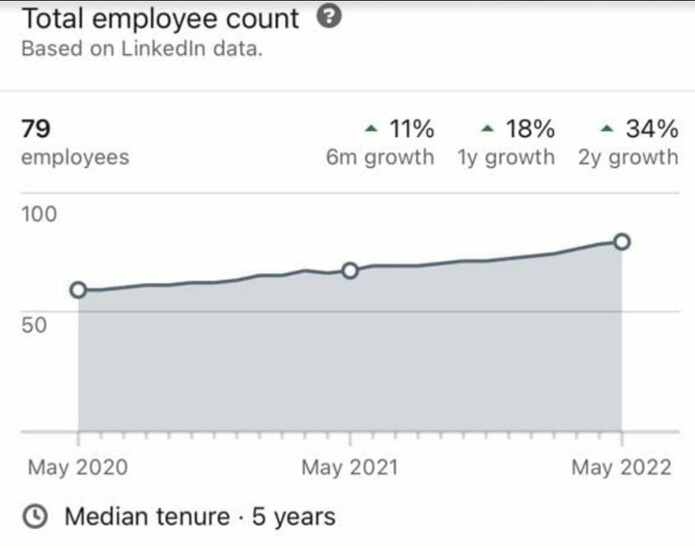

On 28th October 2021, Mr. Aalap Prajapati (next generation) took over position of MD and CEO from his father Mr. Natwarbhai Prajapati, who became company chairman. They have started uploading investor presentations since then.

They also did their first-ever investor meeting.

He is 34 years old.

He also bought shares in the open market.

They are planning to enter new geographies, and launch new brands (especially in chronic segment).

They are also focused on improving productivity (per capita per month sales).

They are also hiring experienced professionals.

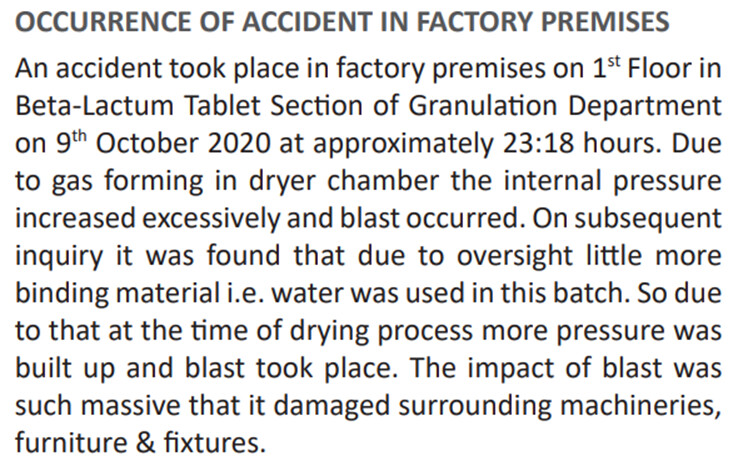

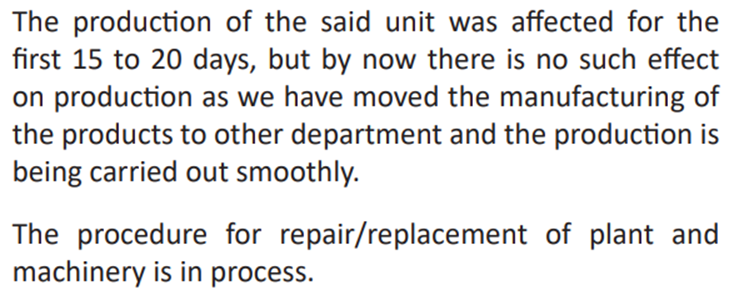

An accident had occurred in the factory in 2020

They earlier had a metal division which was discontinued

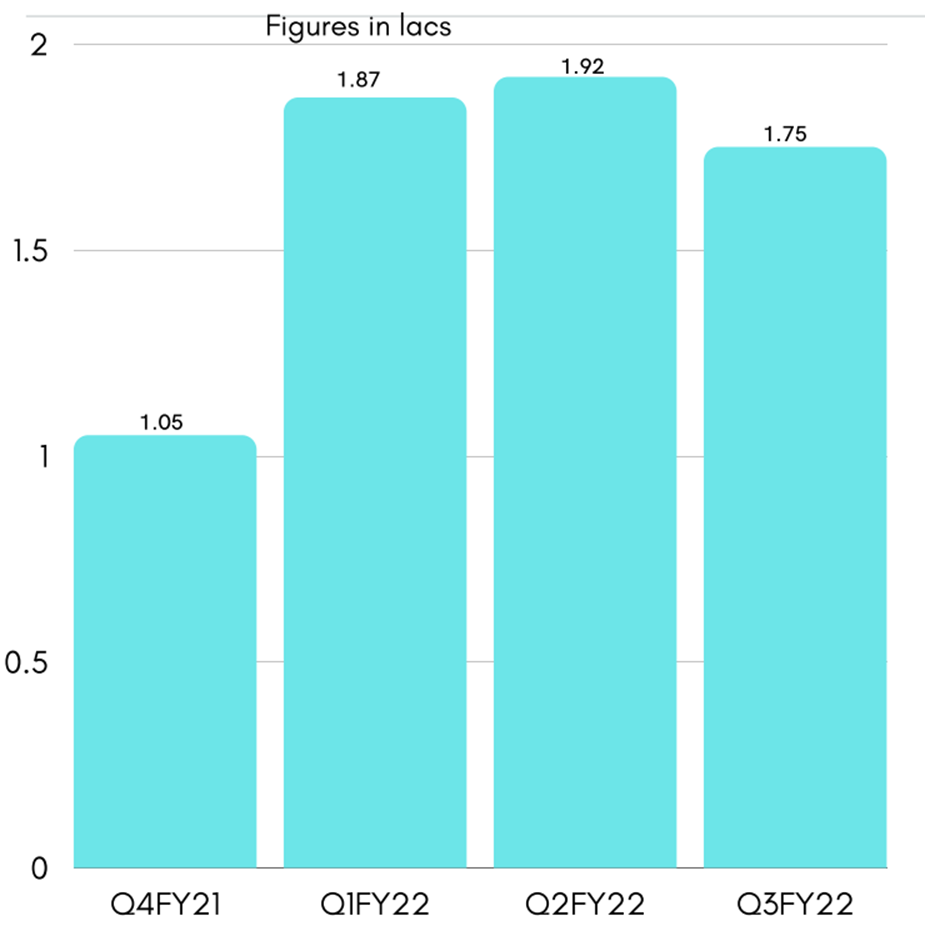

The annualized RoCE for Q2 and Q3 FY22 was 15.8% and 18.4% respectively.

Key anti-thesis as per me is that it might be difficult for them to create a brand recall, and getting doctors to prescribe their brand (given that they operate in highly competitive segments) may be a challenge. Also low promoter holding (36.2%)

My thoughts: 1) This level and granularity of disclosures in investor presentations from such a small company is quite unique; 2) Gross margin of 62% for FY22 suggests there might be something unique

Disc- I have a small tracking position