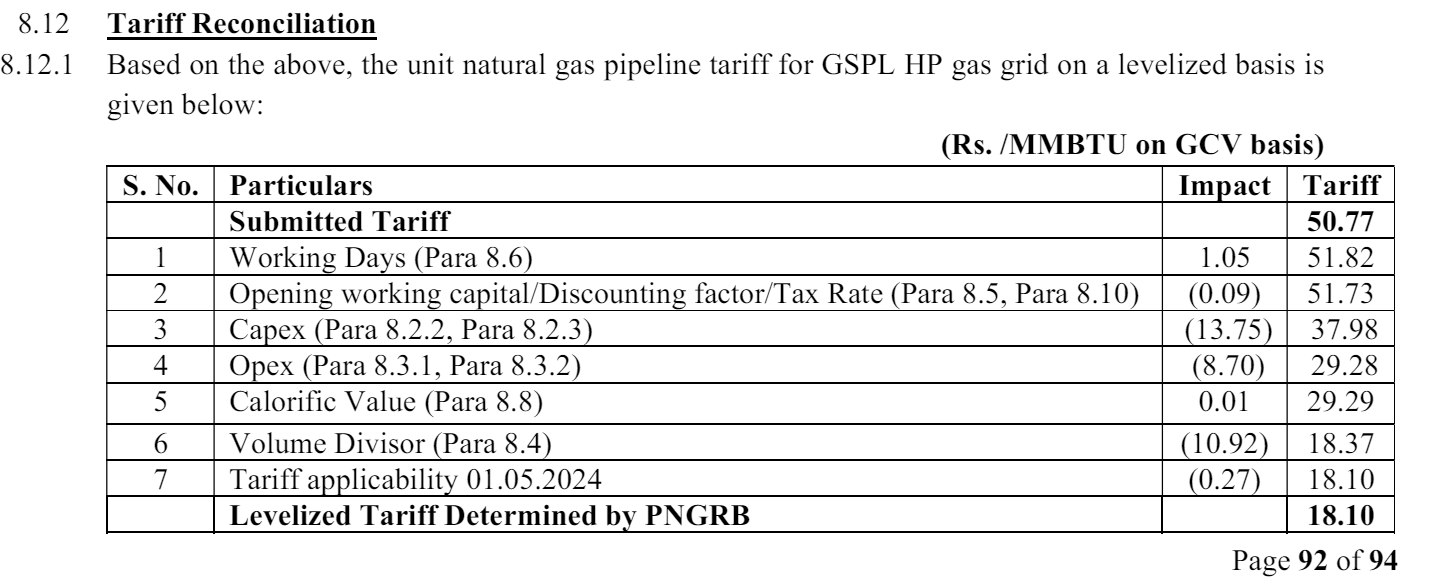

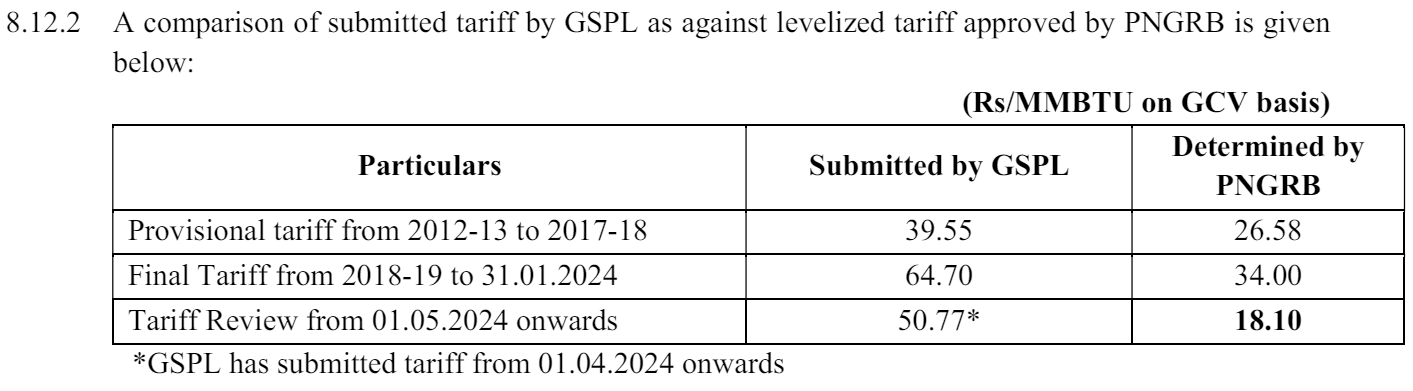

The tariff for the High Pressure Gas grid of GSPL has been reduced to Rs.18.10/MMBTU (for 01.05.2024 onwards) from Rs. 34/MMBTU (for 2018 to 31.01.2024). This is a sharp reduction of around 46% from previous tariff. The company had proposed a tariff of Rs. 50.77/MMBTU and the final approved tariff is Rs. 18.10/MMBTU by PNGRB. Historically also the approved tariff by PNGRB has been lower than the submitted tariff by GSPL.

This reduction can lead to big drop in standalone revenues and profitability of GSPL.

The order also mentions a possible revision in tariff next year if actual volume is very different from the expected volume considered by PNGRB (31.67 MMSCMD). The company while proposing 50.77/MMBTU has considered 26 MMSCMD.

This is a serious setback. Even if tariff gets revised this action from PNGRB will remain an overhang which means stock will take a very long time to recover.

GSPL’s expectation was ~Rs 50/MMBTU. However, PNGRB has proposed ~ INR 18/MMBTU which is even lower than the current tariff of Rs 34/MMBTU. Hence, the reason for steep fall in stock price

My understanding in that tariff decline by ~50% (Rs 34 to Rs18) will completely wipe out profitibility of GSPL.

From PNGRB perspective, its clear that their incentive to provide customer services at cheapest tariffs, and as long as GSPL survives/does not break , they are fine.

Something that I am trying to understand here:

What incentive do GSPL management has to fight with low tariff order by PNGRB? My understanding is that , with largely fixed compensation, enhancing profitibility of GSPL will not be driving force for GSPL management.

The promoter of GSPL is again governed by government of Gujarat, with hardly any incentive to drive profitibility of GSPL. As long as GSPL continue to discharge its tasks (maintining pipepline) and does not break, the promoter should be fine.

So, who is going to fight any adverse impact on GSPL when promoter and management do not have any incentive to do so. Is there any other influential shareholder (Institutional shareholder) who has high stake in GSPL and hence the incentive to influence management and government and take steps to fight PNGRB orders?

Regulation risk is always there in such companies. PSE companies don’t care much about investors unless they want to divest, that’s the only time share price matters to them.

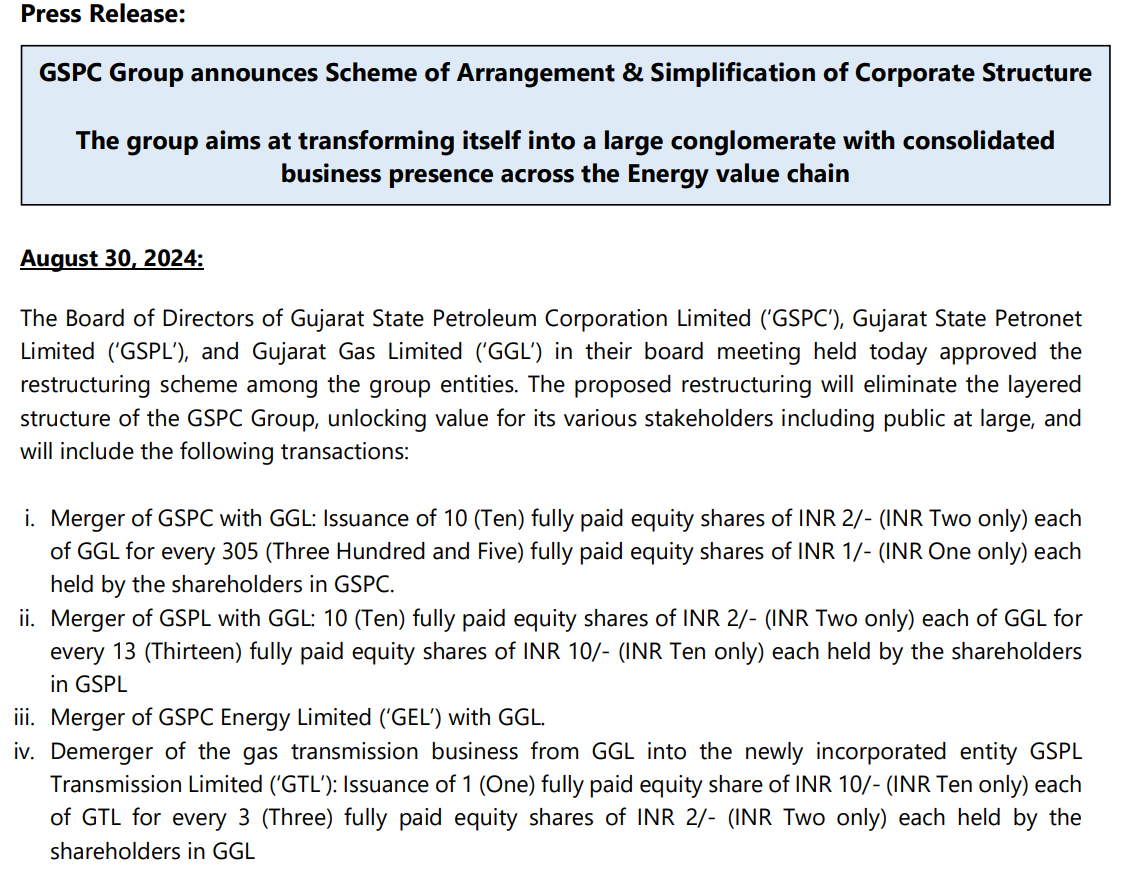

Merger of GSPL with Gujrat Gas Ltd.(GGL)

Shareholders will be allotted 10 shares of GGL for every 13 shares held of GSPL. GSPL owns about 54% stake in GGL. Gujarat State Petroleum Corporation Limited(GSPC) which owns 37% in GSPL will also be merged in GGL.

Transmission business of GSPL will be finally demerged into GSPL Transmission Limited (GTL) which will be subsequently listed on the stock exchange. Shareholders will be given 1 share of GTL for every 3 held in GGL.

Stock of GSPL has already run up 30% in last week, now it is almost priced ideally for the 10 to 13 swap ratio. Assuming GGL at 600 per share, GSPL should be priced at 461 per share, current price of GSPL is 443 per share.

There is a investor call at 3.00 pm on 31st August to discuss this restructuring.

Valuation of GSPL Based on the Amalgamation Scheme

The current valuation of GSPL is calculated as: (10/13) × GGL Price (₹462) ≈ ₹355.

This valuation is based on the current GGL entity. However, after the merger, the merged GGL will effectively double in size, incorporating the revenues, net worth, and potential earnings of GSPL, GSPC, and GEL. Therefore, it may not be appropriate to base valuations solely on the current GGL numbers. Let’s consider the financials of the merged entity.

Valuations Overview

Revenues (Turnover)

Current GGL Turnover: ₹16,292.97 crore

Merged GGL Turnover (Estimated): ₹36,809.09 crore

This is the combined turnover of:

GGL: ₹16,292.97 crore

GSPC: ₹18,452.74 crore

GSPL: ₹2,031.54 crore

GEL: ₹131.84 crore

Assumption: No significant operational changes occur before the merger.

Net Worth

Current GGL Net Worth: ₹6,931.43 crore

Merged GGL Net Worth (Estimated): ₹22,321.38 crore

Contributions from:

GGL: ₹6,931.43 crore

GSPC: ₹5,124.42 crore

GSPL: ₹10,263.87 crore

GEL: ₹1.66 crore

Profitability (EPS Estimates for FY 2025)

GSPL (Standalone): EPS of ₹20 (35% reduction due to PNGRB tariff changes).

GGL (Standalone): EPS of ₹15 (10% reduction due to APM allocation changes).