This is my first post so I request you all to please ignore if you find anything silly. I would love to read your comments. Company Background

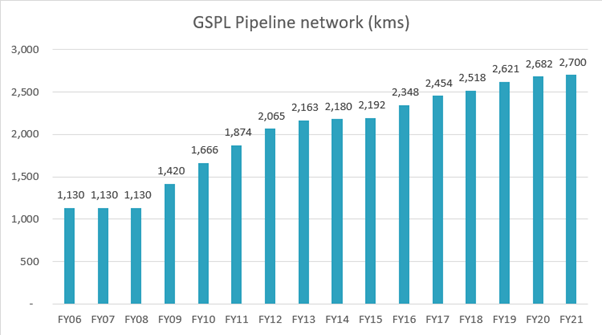

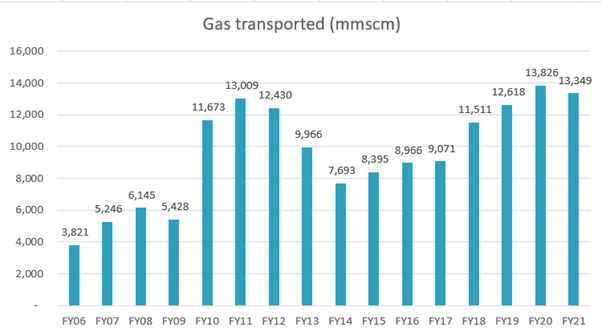

Gujarat State Petronet Limited (GSPL) was set up to complement the efforts of GSPC. While GSPC harnesses and procures natural gas, GSPL is building the infrastructure that transmits the gas across the state of Gujarat and ultimately allows last-mile linkage to the end-user. GSPL is laying a gas grid, to facilitate gas transmission from supply points to demand centers. GSPL has already put in place a pipeline network of about 2700 km and further extension of the pipeline network is going on. The company has signed gas transmission agreements with various industries for the transportation of natural gas from various supply sources in Gujarat. Presently, the company transmits over 37 MMSCMD of natural gas.

The main thing to note here is that the parent company is a State company and they project themselves as Integrated Energy Companies as they have a presence in all 3 segments of Energy transmission (Upstream - GSPC, Midstream - GSPL, 2-3 SPVs specific to transmission, Downstream - CGD business of Guj Gas and Sabarmati gas) Revenue Streams

Gas Transmission - Earns Revenue through transportation of gas from extraction sources and import terminals to different areas of Gujarat. Caters to City Gas distribution networks, Power Companies, and other two sectors. Below is the screenshot of the historical volume of transmitted gas and revenue earned through Transmission.

CGD Business: - Owns ~52% of Gujarat Gas Ltd. (it’s a complex ownership with parent company GSPC also having part of it)

Wind Power generations - Small percentage of revenue from this. Can be ignored for the sake of discussion

Investment Thesis

Building of LNG import terminals in Gujarat will lead to increased transmission of gas

LNG demand may rise as there is a push from the government to adopt cleaner fuels by industries.

in one of the analyst reports it was said that the company is having 100% utilization of its pipeline and company is increasing its transmission capacity

Procured licenses to lay cross-country pipelines (along with consortiums companies). Below are the details

4.1 GSPL India Gasnet Limited (GIGL) for development of Mehsana – Bhatinda (approx

1834 Kms) and Bhatinda – Jammu -Srinagar (approx 740 Kms) Pipeline Projects

4.2 GSPL India Transco Limited (GITL) for development of Mallavaram - Bhopal –

Bhilwara – Vijaipur (approx. 1881 Kms) Pipeline Project.

Industry to grow by 7% and company to grow by 10-12% as per Management

you get ownership of Gujarat gas ltd. (P/E: 25) at a cheap price (GSPL P/E: ~10)

Risks

Adoption of LNG - Availability of cheaper fuels is the main threat to the adoption of LNG.

Transmission revenue is inversely proportional to LNG price. since the price of LNG is increasing, it will be difficult for companies to switch to LNG

Company has Contingent liabilities

Did not calculate the pension obligation but not so huge

Frequent dilution of equity through ESOPs

Some Doubts

How can I get information on Capacity utilization

I was not able to understand how do they charge customers? The reason is that the implied tariff is fluctuating, so I want to know the reason as to why it has such a behavior.

How much more capacity will they be adding?

in some years the drop in sales was accounted to lower production of LNG in domestic fields. so I want to understand how do they source Imported LNG? do they have to Buy the gas? Do they have any kind of agreement?

Their OPM (standalone) is decreasing because of increasing ‘Gas Transmission expense’. Management does not provide any commentary on why it is increasing at a higher rate.

I think Con calls and research Reports will help to find about the capacity utilization and stuff.

Being your first post, I should say your post is quite clear to understand. It won’t waste your time to read it, it seemed very simple to read and understand the business.

Like Peter Lynch used to say don’t invest in a business that you can’t explain to two years old. (Actual saying may be different from this), Cheers!

Thanks @Harshad_Bhagwan . The problem is, I am not able to find any con call on the internet and annual reports are not filled with information. The management does not provide any commentary around the reasons for volume or other expenses moving up or down. I was able to get good info from the analyst reports but they all talk more about the projections.

I have invested in GSPL too. The only info I lack nonfinancially, is how many gas pipeline km is owned by each entity like GSPL,GAIL, HPCL,BPCL. I will be better informed of who owns how much and how much gas is pumped in those kms in MCM

But in one of the reports, it was said that 85% of the LNG imports will flow through Gujrat. So if that is true, wouldn’t it benefit the company in a huge way given that it has exclusivity of transmitting gas in and through Gujarat? Am I missing something here? How does GAIL source gas?

they dont have to use only gujarat. They make gas imports as well transmission fees. Others can import but can move it through their franchise network. Usually, GAIL and IOC for e.g. will put in joint money to move from Mumbai to Surat or Delhi etc.

Leadership position in natural gas transmission business

GAIL is the market leader in the transmission of natural gas in the country with over 12,400 Km of pipeline network, out of total pipeline network in India of ~17,500 Km (i.e. 70.86% of country’s pipeline) as on March 31, 2020 with natural gas handling capacity of 253 Million Metric Standard Cubic Meter Per Day (MMSCMD). Further, pipeline of around 6,700 Km is under construction & approved by GAIL out of total under construction & approved pipe line being laid in India of around 17000 km. Further, company earns stable cash flows from transmission business, though it accounts only around 7% of total revenue in FY20. However, the PBIT margin during FY20 for the segment stood at high of 58% against 55% during FY19. GAIL gets around 12% internal rate of return (IRR) for its transmission business on back of regular tariff hikes for its pipelines. GAIL’s integrated pipeline network of HVJ, Dahej-Vijaipur (DVPL) and Vijaipur-Dadri (GREP) accounts for over 65 per cent of the its’s gas transmission volume.

LNG import tie-up in USA, Russia and Qatar

Over the years, GAIL has developed adequate tie ups for supply of natural gas both domestically and internationally. The company sourced around 50% of its total gas requirement through domestic sources which include ONGC (Administrative Price Mechanism (APM) & Non APM), Panna-Mukta and Tapti (PMT) at APM & Production Sharing Contracts (PSC) prices, Ravva, Ravva satellite, etc. The remaining ~50% gas requirement is sourced through imported gas - Regasified Liquefied Natural Gas (RLNG) (Long-term RLNG, Mid Term RLNG and Spot). GAIL has long term LNG contract of around 14 Million Metric Tonne Per Annum (MMTPA) from USA, Russia and Qatar. GAIL has long term contract to buy 5.8 MMTPA of LNG from the U.S. and up to 2.5 MMTPA of LNG annually on a delivered basis from Russia’s Gazprom while another 5 MMTPA from RasGas Company Limited (RasGas), Qatar. Going forward, capacity utilisation of the company is not only dependent on the company’s ability to market the available gas but securing the additional gas supply for its increasing pipeline infrastructure would also be important.

Got it, so If I understand this correctly, GSPL will be only serving customers where it has CDG business and other Industrial customers in Gujarat. Right? Can you share your investment thesis of this company?

Err…I used the fact the LNG and CDG for a energy import intensive country like ours, I picked all major listed gas companies and bought into them. Worked out well so far. and upping my stakes whenever the price falls.

Here is a business with strong entry barriers, zero competition, runs an essential service as part of critical national infrastructure. Owns 2,700 km of gas pipeline worth Rs.3000+ crore. Has annual revenues of around Rs.2,000 crore, 70 % Operating margin, 50 % PAT margin and long term revenue growth rate of 15%. Debt Equity ratio is just 0.15. Outstanding debt of Rs.750-odd crore against annual operating cash flows in excess of Rs.1,0000 crore. In the next few months, company can be debt free. Another pipeline Mehsana Bhatinda 1670 km is on the verge of completion after which the total capacity will go up 50%.

How much should one pay for such a company? GSPL is available at a market cap of Rs.18,000 crore. Even on a standalone basis, GSPL looks a bargain, not to mention the 54% stake in Gujarat Gas which is worth more than Rs.20,000 crore, which means the core business is free.

Agreed there is a PSU discount, but Gujarat Gas gets premium valuation. Many PSUs are run by corrupt bureaucrats, indulge in populism and run losses. But GSPL has largely been free of any such problems. Contingent Liabilities are also not serious. There is a regulatory risk, but still the undervaluation seems extreme. Financial history of the company is impeccable. Are there any other issues?

What’s the current capacity usage and How the same will increase further? I recall, while studying GGL, that only CGD vertical has increased gas consumption in the last 5 yrs. Per latest Qtr results, CGD contributes only 35% to revenue and rest comes from others (Refineries, Power, Fertilizer, etc.)

Pricing Power - I assume that it’s capped by PNGRB. Is it so?

Future Growth Avenues - What after this last leg of lines are active?

What’s their long term plan to distribute the cash generated by the business?

The only issue I read somewhere was that the prices are capped by the regulatory body (PNGRB) and which makes it unattractive to the investor as there would be no high growth possibility. In Indian markets, only the high-growth companies are rewarded.

Simarjeet - It’s true that prices are regulated by PNGRB. However, the methodology adopted by PNGRB assures 12% post tax ROCE and is revised every 5 years. Last revision for GSPL was in 2018.