Hi, here are my views/notes on the company which i had prepared a fortnight back. In my opinion, past history has resulted in depressed valuations and if a new investor comes in, it can result in valuation rerating as well as improved business performance.

GTL infra – CMP – Rs6.2; Mkt Cap Rs2667cr

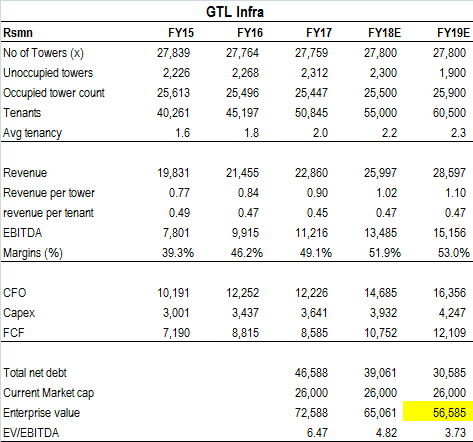

GTL infra is a beneficiary of the ongoing consolidation in the telecom as well as telecom tower business in India. The company has 27800 towers in 22 telecom circles in India. It went into CDR in year 2011 and last year it was referred to SDR. It has recently completed merger with CNIL as a part of SDR process, and post which total debt stands at Rs4800cr with FY17 EBITDA of Rs1200crs. The company is looking to refinance its debt which may result in lower interest outgo to the tune of Rs100-150cr going foward.

Debt reduction journey: In the tower business, the debt (on a combined basis of GTL Infrastructure Limited and Chennai Network Infrastructure Limited) has come down from a peak level of Rs13,318 crores (US$ 2054 Mn.) at the time of CDR to Rs4,841 crores (US$ 747 Mn.) in April 2017. It is expected to further go down to ` 3,840 crores (US$ 592 Mn.) by 2019. This represents a staggering reduction of 71% on an absolute basis. The company achieved this by reducing promoter shareholding in combined entity from 80% down to 20% post SDR (assuming full conversion of Convertible Bonds). Currently, the company is looking at finding a suitor which can buy controlling stake in the company.

Recent deal in telecom tower space: ATC bought 20000 towers of Vodafone Idea for US$1.2bn, valuing the company at Rs39lakh per tower with tenancy ratio of 1.4. GTL has a much better tenancy ratio at 2.0x and hence we expect the company to get much higher valuation for its towers.

Key drivers: Given higher competition in the industry to expand its 4G reach and expected 5G rollout, I believe that the requirement for towers is likely to increase manifold. Reliance JIO has mentioned earlier that they will require 1 lakh towers for its subscribers. Moreover, very high free cash flows will ensure faster debt reduction for the company and the management has envisaged that the company will be debt free in 3-4 years.

Industry dynamics: According to media reports, India has a little over 4.5 lakh towers — expected to grow 3-5 per cent on year — with Indus Towers with nearly 1,23,000 the leader followed by Bharti Infratel with about 91,000, state-run Bharat Sanchar Nigam with 65,000, ATC with 58,000, GTL Infrastructure nearly 28,000, Reliance Infratel, 43,600, Tower Vision India 9,000 and Ascend Telecom Infra.

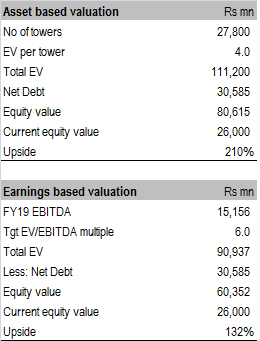

Valuation: the stock is currently trading at 3.7x FY19 EV/EBITDA. I have done the valuation based on asset based as well as earnings based method. I am getting upside of 130%-210% in this stock assuming conservative estimates. If a new buyer is coming in, it can have substantial rerating in my opinion. I am attaching a picture of financials along with this msg.