GSM Foils Limited – Equity Research Report by R Sawkar (on X @valuevzard)

Initiation Coverage | July 6, 2025

Ticker: GSMFOILS | Sector: Packaging Foil / Pharma Ancillary | Exchange: NSE EMERGE

Company Overview

GSM Foils Limited, incorporated in 2023, is engaged in the manufacturing of aluminium-based pharmaceutical packaging materials, particularly aluminium foil and aluminium blister foil. The company operates out of its registered facility at Diamond Industrial Estate, Vasai (East), Palghar district in Maharashtra.

Though young, GSM Foils is positioning itself as a critical backend player in the pharmaceutical supply chain, serving India’s expanding formulations and generics market. It aims to benefit from the growing compliance standards and increasing penetration of blister packaging, especially for export-driven pharma companies.

- CIN: U43303MH2023PLC405459

- Website: www.gsmfoils.com

- NSE EMERGE Code: GSMFOILS

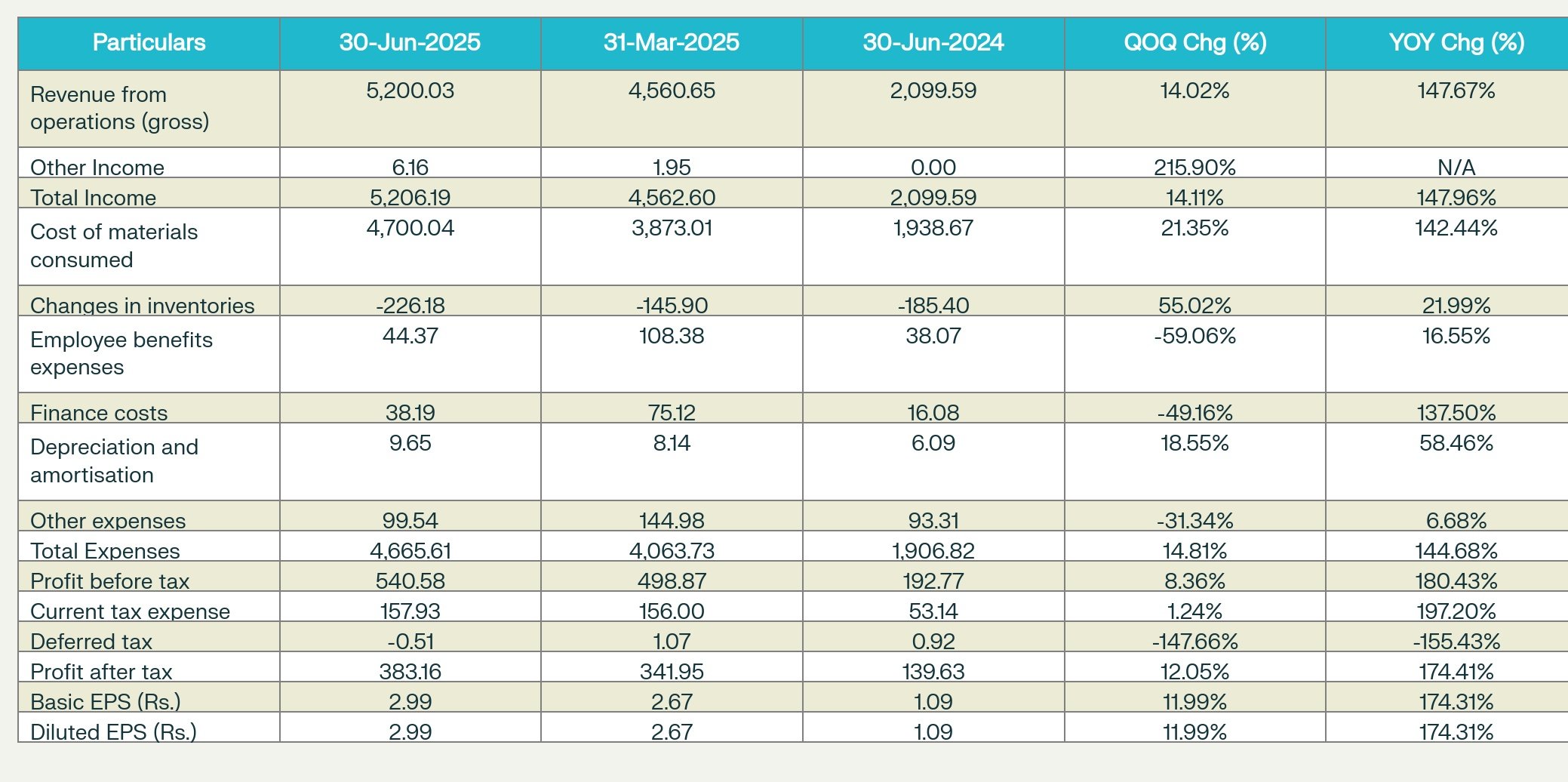

Key Operational Update – June 2025

As per the disclosure to NSE dated July 5, 2025, under Regulation 30 of SEBI LODR, the company has reported the following:

| Period | Net Sales (₹) | YoY Growth (%) |

|---|---|---|

| June 2025 | 18.18 Cr | 88.50% |

| June 2024 | 9.64 Cr | — |

| Q1 FY26 (Apr–Jun) | ₹51.99 Cr | — |

- The YoY revenue growth of 88.5% for June is a strong signal of rapid business expansion.

- Quarterly sales crossed ₹50 Cr in just the company’s second full year of operations – highlighting scale-up in customer onboarding and order execution capabilities.

Industry Tailwinds

- Pharma Packaging Boom: The Indian pharmaceutical industry is growing at ~9–10% annually, with blister packaging demand rising faster due to export compliance.

- Import Substitution: The Indian government’s thrust on domestic manufacturing and PLI schemes benefits backward linkages like GSM Foils.

- ESG & Safety Compliance: Blister foil provides improved shelf life, hygiene, and tamper resistance — making it the packaging of choice.

Key Risks

- Client Concentration: As a newer player, GSM may have exposure to a few large clients, risking revenue lumpiness.

- Aluminium Price Volatility: As a major input, price swings can compress margins unless covered via pass-through clauses.

- Scale vs. Profitability Trade-off: While sales are growing fast, visibility on EBITDA margins and working capital efficiency is limited at this early stage.

Valuation Outlook

Although full financial statements are yet to be released on NSE post listing, the sales traction in Q1 FY26 (₹51.99 Cr) implies an annualised run-rate of ~₹208 Cr, suggesting a strong revenue trajectory. If the company maintains gross margins above 20%, it could deliver operating profitability within FY26, making it a candidate for institutional radar post SME-to-Main Board migration.

Conclusion

GSM Foils Limited is showcasing the early signs of being a promising B2B manufacturing story in the high-growth pharmaceutical packaging ecosystem. With a sharp 88.5% YoY sales jump in June and a robust ₹52 Cr Q1 performance, the company seems to be on an accelerated path of scale-up. However, further disclosures around profitability, order book, and margin profile are needed before making a definitive investment view.

Watchlist Candidate for GARP-style investors tracking emerging B2B manufacturing plays.

Do your study, due diligence , not a buy or sell recommendation.

Your views are welcome.

please follow me. Thank you.