Thought I’d post an update for the benefit of anyone reading this thread. It’s difficult justifying how the stock has found itself at current levels.

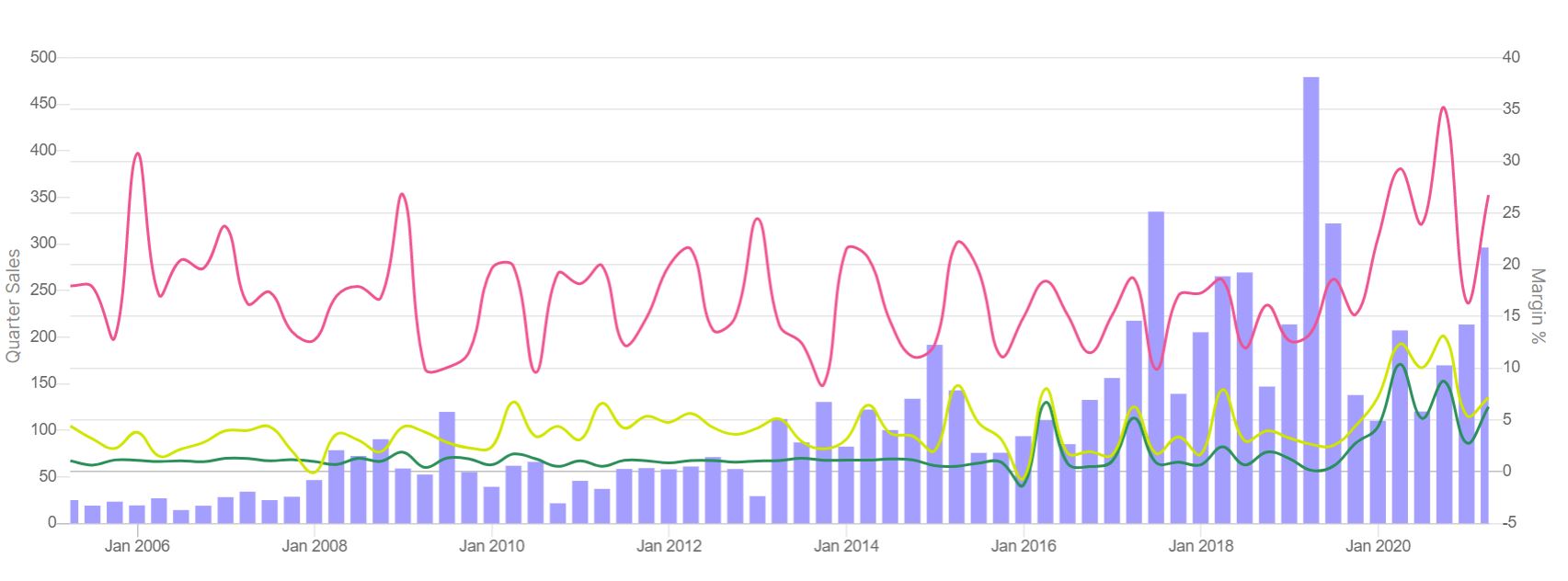

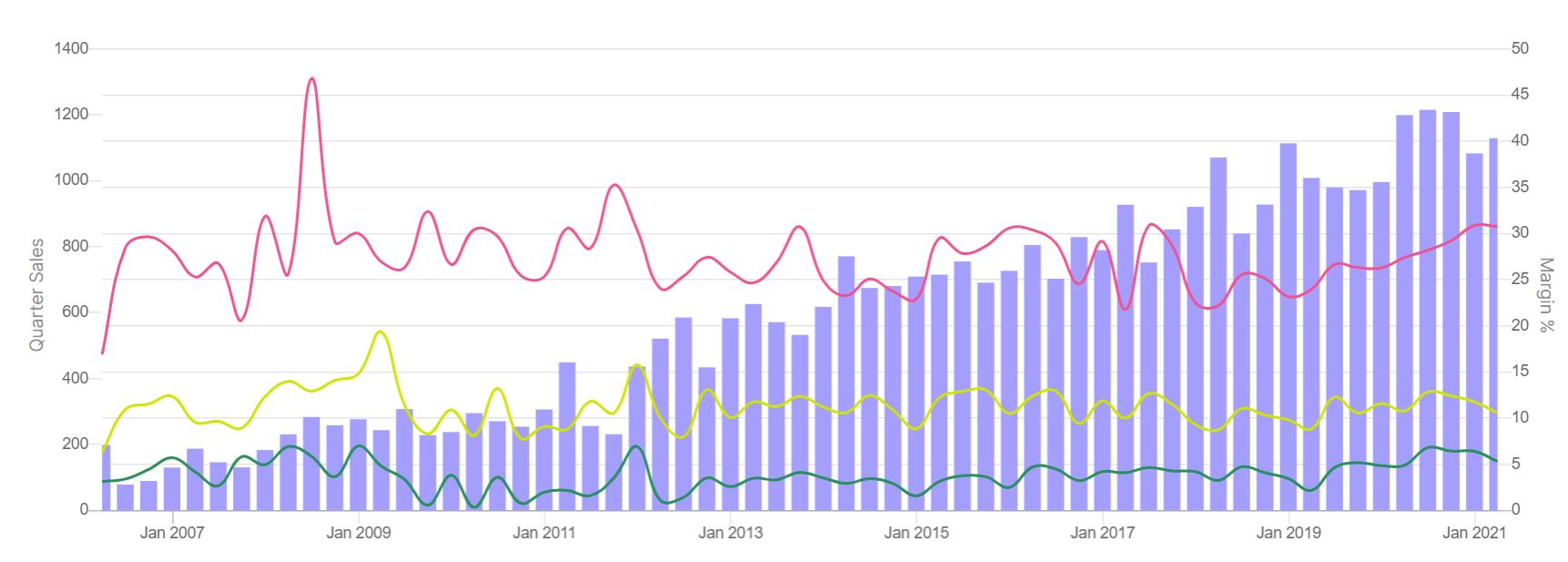

Sales have not improved since 2018:

This looks even worse compared to Daawat…

The valuations that were attractive last year have now become expensive, and GRM is currently trading at 8x its historic valuations.

This said, margins have expanded from 3-4% in 2018 to 7-8% presently. They have been repaying their debt steadily quarter after quarter. Metrics like RoCE and the inventory turnover ratio have improved from 11%/4.03 in 2018 to 19%/8.15 in 2021. Their asset turnover ratio is also 22, almost 4x higher than Daawat’s.

On the corporate action front, they announced a sizeable dividend of Rs. 20 / share earlier this year, and they’ve just announced a 2:1 bonus. They’ve ventured into spices as seen earlier in the thread, but these spices can’t be found on the internet or at any store, so I’d guess that they haven’t launched the products.

They’ve started selling in the domestic market, but they announced this in a very strange way - they said they’ve formed a partnership with JioMart, selling their rice in 45 distribution centres.

At the same time, there’s been some equity dilution this quarter:

The nicest thing about the company at the moment is its new website.

Edit: They’ve uploaded an investor presentation.

Disclosure: invested from lower levels, no recent transactions.