This is strictly for those who own Grindwell Norton stock, and intend to keep it for the next couple of months.

Saint Gobain Sekurit will merge with Grindwell Norton. 17 shares of Saint Gobain will be eligible for 1 share of Grindwell Norton.

Saint Gobain shares are available on BSE at around 14.20 Rs. Grindwell Norton Shares are currently selling around Rs. 255-258.

If you own Grindwell Norton Shares, you could buy Saint Gobain Shares at 14.20 (meaning the price of 1 GN share is then 14.2*17=241 Rs.), and sell Grindwell Norton at 255, which would give you a 14 Rs. profit within a couple of months, once the Saint Gobain Shares are exchanged. This works out to over 5% return, after transaction fees.

Unfortunately, both shares are thinly traded. And no futures to exploit. If you own GN shares for sure, then makes sense to do this (unless considerations of ST capital gains are prevalent).

1 Like

Thanks, Hemant for the timely warning. Luckily, I just saw your message, and got rid of the Saint Gobain Shares I owned immediately, with little or no damage.

Regards

Samir

I am pretty impress by recent result announced by Grindwell Norton. I need to understand the business better. So, can anyone help me with it?

Thank you in advance.

1 Like

Is there any separate thread on Grindwell Norton.

Members pls suggest

i think u can use this thread for Grindwell norton alone.

1 Like

Can anyone tell, why there is no interest in this company on valuepickr?

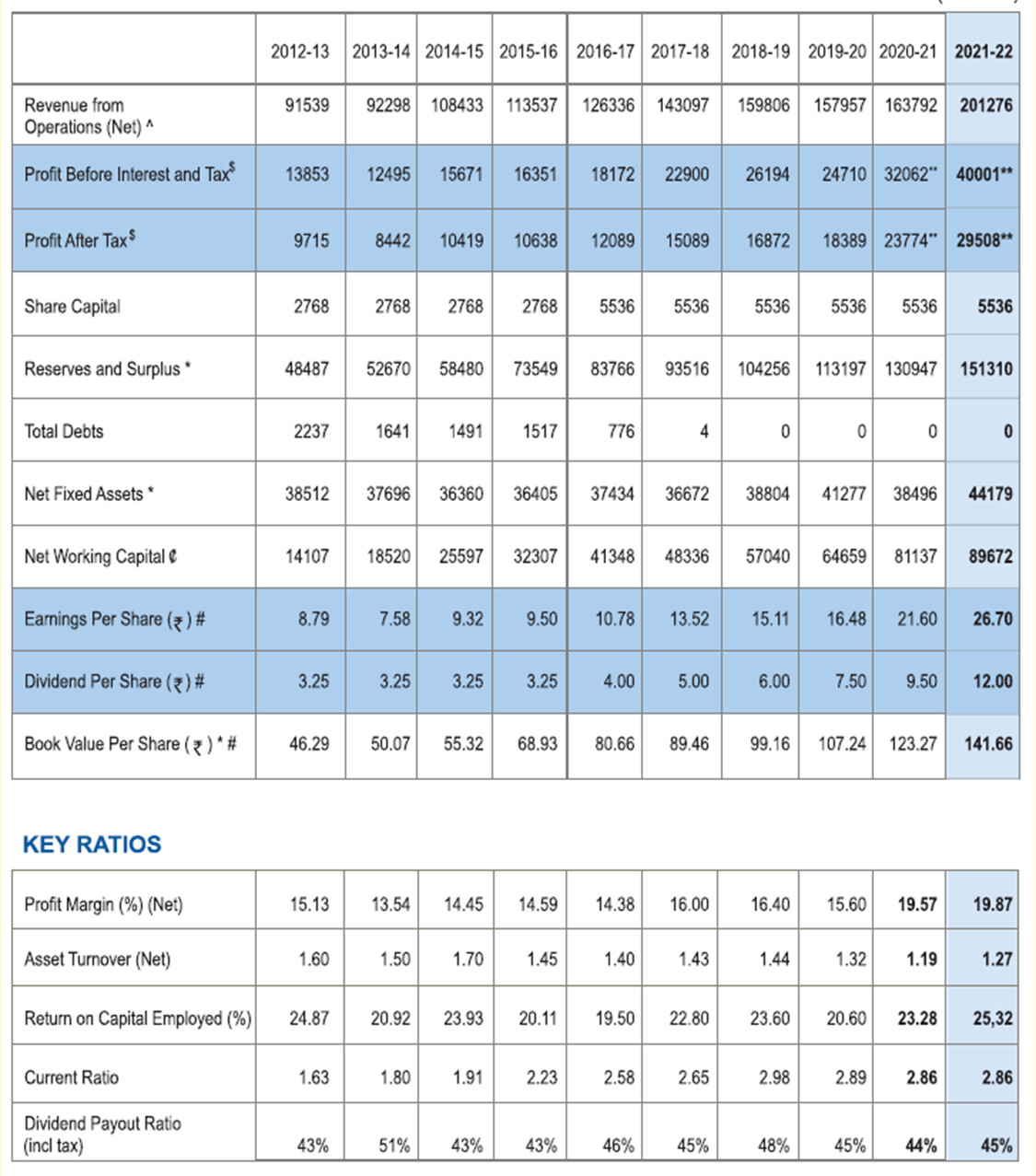

2021- 2022

Observations:

- Revenue, PBT, PAT, Reserves, Fixed assets, EPS, Dividend, ROCE exploded.

- NPM increased considerably.

OPERATIONS

The recovery of growth of the Indian economy started in the second half of the financial year 2020-21 and continued during the financial year 2021-22. With ease of Covid restrictions and supply disruptions post the second wave of Covid, the output levels reached the pre-pandemic levels. India’s GDP for the financial year 2021-22 is likely to end with a growth of 8.7% compared to a contraction of 7.3% witnessed in the financial year 2020-21. Third wave of COVID-19 and Russia-Ukraine conflict that started in last quarter of financial year had limited impact. The Industrial activity has remained positive during the financial year. The Index of Industrial Production (IIP), witnessed a growth of 12% in the financial year. The industrial recovery was fairly widespread. Reflecting this your Company’s consolidated revenue from operations and operating profit increased by, 22.9% and 25.0% respectively.

Abrasives

The overall performance of the Abrasive business for the financial year 2021-22 was good. The business faced challenges in the first quarter due to disruptions caused by the second wave of Covid. The second and third quarter witnessed significant increase in input costs and the supply chain disruptions. Even though the availability of raw material eased during the last quarter of financial year the inflationary pressure continued. The improved price realization**, gain in market share and continued control over costs helped the business grow the sales and operating profit by 22% and 39% respectively.**

Ceramics and Plastics

The Performance Refractory business witnessed 35% increase in sales over 2020-21 mainly due to the increased demand from the end user industry. The substantial increase in profit was mainly due to improved realization and improved plant efficiencies. The Performance Plastics business had an excellent year with a significant increase in sales (domestic and, in particular, exports) and operating profit. This was mainly due to the outstanding results of the Life Sciences segment. The revival of automotive business and the construction sector resulting in higher sales of bearings and composites. The SiC business witnessed significant growth in sales and operating profit mainly due to improved domestic demand led by the refractory industry. The inflationary pressure on the input cost was more than offset by the improved realization. The operations of your Company’s subsidiary in Bhutan were

continued to be impacted by the restrictions imposed by the Government to control COVID-19 and, as a result, there was a decline in production. Overall on a consolidated basis, the sales and operating profit of the Ceramics & Plastics segment increased by 31% and 36% respectively.

Shareholding pattern:

|

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

| Promoters: Foreign |

51.33 |

51.33 |

51.33 |

51.33 |

51.33 |

51.33 |

51.33 |

| Promoters:Indian |

7.70 |

7.57 |

7.03 |

7.00 |

7.00 |

7.00 |

6.75 |

| Insurance Companies & Banks |

0.01 |

0.01 |

0.01 |

0.01 |

0.30 |

1.43 |

0.71 |

| UTI & Mutual Funds |

13.13 |

14.00 |

14.49 |

15.05 |

16.27 |

15.92 |

14.61 |

| NRIs, OCBs FIIs and FPI |

4.94 |

4.95 |

5.21 |

5.10 |

4.75 |

4.73 |

7.91 |

| Domestic Companies and Trusts |

5.30 |

4.11 |

4.18 |

4.45 |

4.60 |

4.43 |

4.44 |

| Resident Individuals |

17.59 |

18.03 |

17.75 |

17.05 |

15.77 |

15.18 |

14.25 |

Foreign exchange earnings and outgo:

| Year |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

| Inflow |

138.05 |

180.78 |

185.19 |

195.29 |

242.69 |

292.68 |

332.10 |

360.12 |

356.08 |

| Outflow |

315.99 |

342.46 |

355.53 |

386.63 |

505.70 |

515.72 |

376.73 |

375.37 |

630.88 |

| Inflow/Outflow |

43 |

52 |

52 |

50 |

47 |

56 |

88 |

95 |

56 |

| Abrasives % of turnover |

NA |

70.8% |

66.9% |

67.62% |

63.5% |

62.8% |

60% |

NA |

NA |

2 Likes

Grindwell Norton

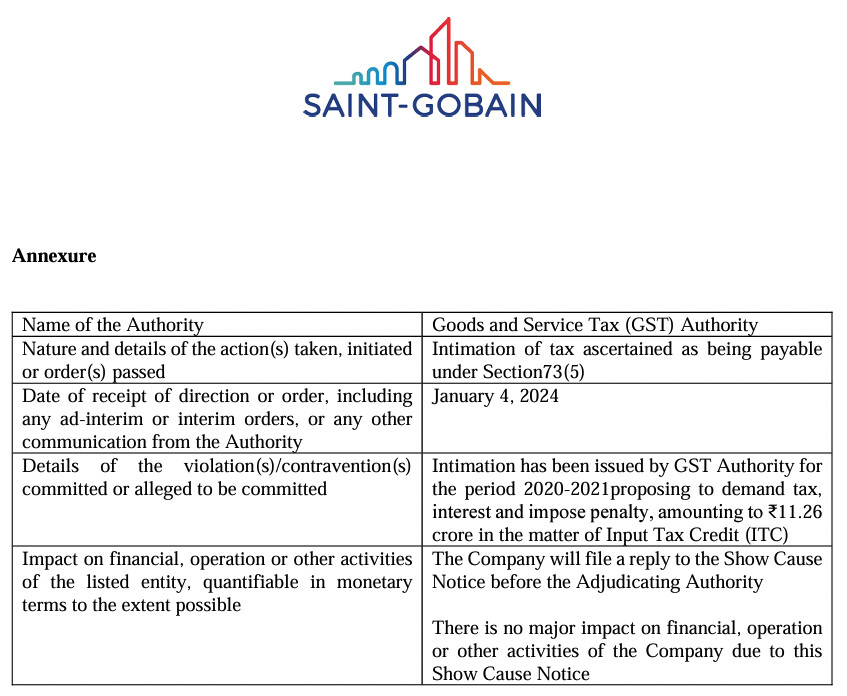

Company has received intimation from the GST Authority : amounting to ₹11.26 crore : As per company : No major impact

Is this the good time to pick up the shares

Being a beginner seeking advices.

Thankyou