Hi everyone creating a thread for companies which have great management .the definition for great is execution plus corporate governance.i think 90 percent of a stock returns are due to management quality.

Listing the companies where I like management

- sona comstar — excellent execution and uniquely spends very high amount in r&d compared to peers.

2)nh-clean governance one has to read concalls during Covid for this to really understand.

3)windlas–very direct and honest management.

4)sjs— excellent execution and although were trolled initially now it is a insane execution case.

5)kims—no other hospital is expanding faster than kims geographically and breakevens faster compared to peers.

6)rainbow-- no debt intends to grow mostly through internal accruals that too in a asset heavy business.

Disclaimer)I may or may not own some of the above companies.none of the above are financial advice.

Did not get time all this while so starting a detailed thread on great management again by the proof of execution in business.

Lets start with Sjs enterprises:

Firstly i was analysing diff auto ancs and when arranged based on opm it is in top 4(main) players along with sona.So started reading this comp in 2024 feb.At this point of time company was not growing this fast and they have gone and acquired Walter Pack India (90.1% stake) in 2023 the reason was WPI’s expertise in advanced in-mold technologies complements SJS’s portfolio .pasting the MD comments here — *Our primary driver of interest in Walter Pack is its complementary and adjacent technologies of IMF, IMD and IME. IMF [In-Mold Forming] in Walter Pack’s core business. This technique is used to produce high-quality 3-dimensional plastic parts with decorative finishes, which are robust and resilient to abrasion and wear .

this gave them oppurtunity to grow in consumer division very well as well and also passenger vehicles. this acquisition helped them to cross sell from their core portfolio as well.walterpack india revenue for FY23 revenue ~INR 1,200 Mn which explains the bump up in revenue after the subsequent quarters.

One more Acquisition in 2021 was this:

SJS Decoplast Private Limited,adding chrome plating and painting capabilities

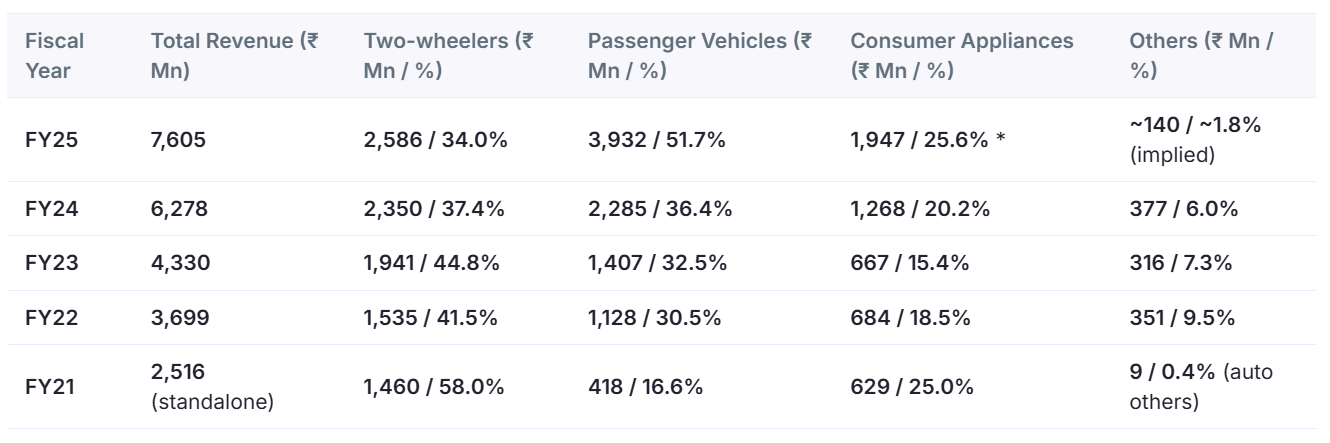

this is how the revenue by end segment look like for last 5 years:

Used AI here might be little deviation in actual.

So basically the passenger vehicle revenue grew very good 41 crore to 393 crore and their consumer appliance division grew from 62 crores to 194 crore.these growth rates are mainly driven by acquisitions.in my view they have excuted very good on inorganic acquisition part and also the fundamental reason for acquistion is they were previously highly dependent on two wheelers in fy21 which contributed to 58 percent and in two wheelers what you see is what you get there are no high value aesthetic parts and thats why they targeted companies which can help them grow the pv,consumer division and in last five years we can see how they have grew in these divisions.PV is the area where the major growth in future can come from as that is where aesthetics have upside .

So from this their inorganic strategy is very good as of now!!

Now the management is very upbeat on exports and optical lens oppurtinity as it is a high value thing and this will increase the kit value significantly and every car has a screen now.plus they entered into an agreement with BOE Varitronix to help them in tech know how for this.Exports have been a main goal for them which reflects in their new order wins as well because of cost arbitrage.

So far they have executed well due to auto upcycle and their outperformance of market growth.But i feel exports once picked will be a major driver of growth.

few orders which might push exports up:

1)SJS has secured a global order from Stellantis,

to supply across North America, Latin America

and Europe

2)SJS won a major order from Whirlpool US, marking

our entry into the dishwasher market

3)FY25 highlights for exports :

any of these ramping up will give good upside in exports especially US orders.

This is their aim for exports ------we aim for exports

to contribute around 14-15% of consolidated sales by

FY28.

In summary i like their capital allocation very much as incremental profits ar e being used into the business mostly .155 cr is in investments on balance sheet.I feel they will further acquire some companies in future as well.They have sufficient gun powder as well to do so.

One more imp point is they have cracked hero this year as well.

Downsides:

1)auto cycle turning negatively.

2)exports slowing down.

Disclaimer:Not a financial advise only for education purpose.