The main issue is business is highly cyclical… I am working in the shipping industry for last 23 years ( presently Captain of large crude carriers ). Have seen many cycles of boom and bust in shipping… When things go downhill no one knows how long the negative sentiments will last…Shipping is an asset heavy industry with constant increasing of regulations and upgrade requirements. So if the market goes bad owners will still need to spend money to keep their fleet servicable. They will themselves not know for how long and only companies with very deep pockets survive. Have seen many big ship owners going bankrupt when times are difficult. These are possibly the reason why market do not tend to give high multiples to these earnings.

ship order is all time low, and still no one is buying new assets even when crazy prices on ton mile currently. if you look at stocks like Scorpio tankers, even they are clearing debts , but no addition of new ships…as you rightly pointed 40% EPS degrowth and still stock should make decent profits plus will be zero debt shipping company…

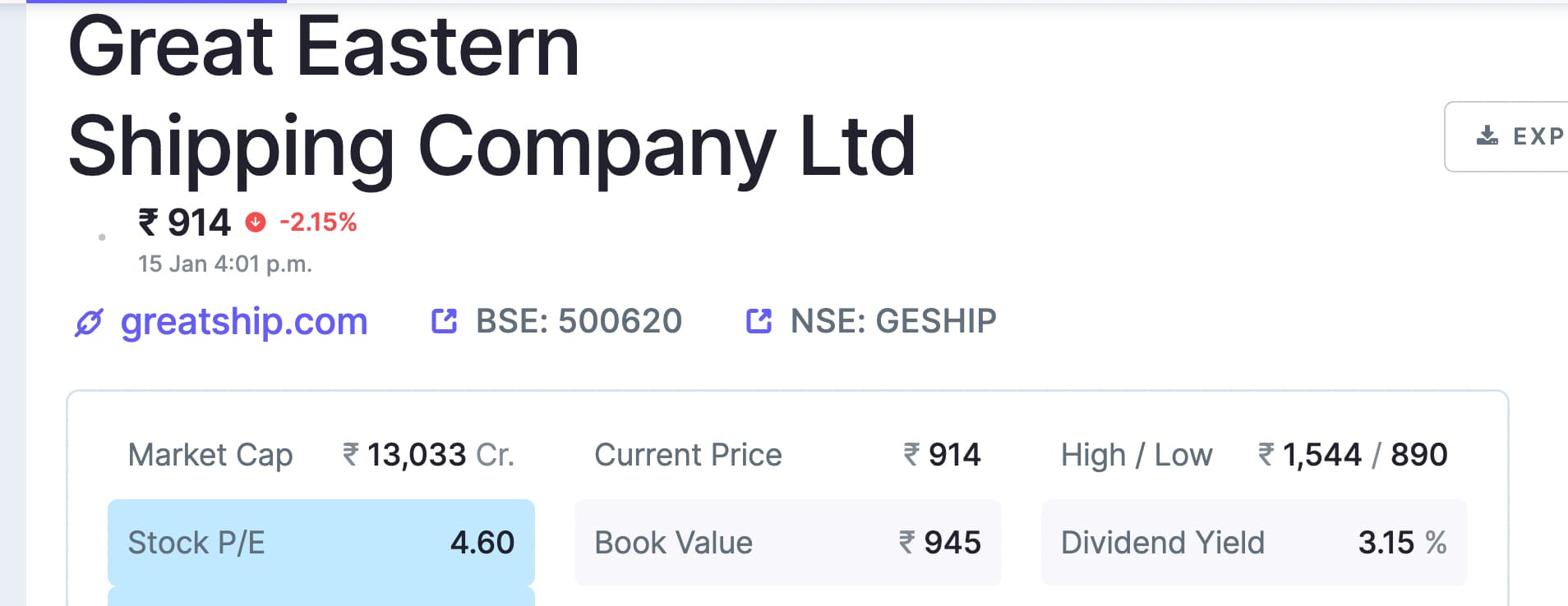

At PE of 6 With asset value at 14k cr and reserves at 9k cr along with good dividend yield , It looks no brainer investment at this stage as NAV is Consolidated at 1400/share…

Last 10 years , Median PE is around : 10 → Current PE : 6

Last 10 years , Median PBV is around : 1.1 → Current PBV : 1.4

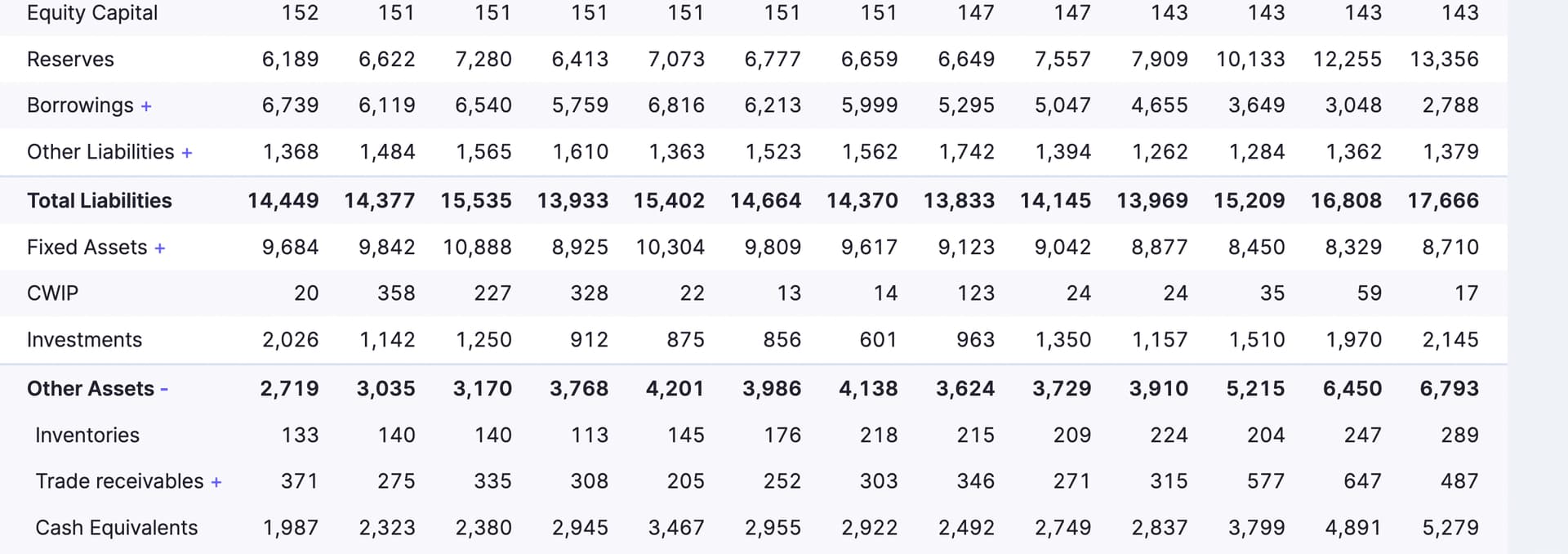

FY24 , other income has contributed 20-25% of PBT

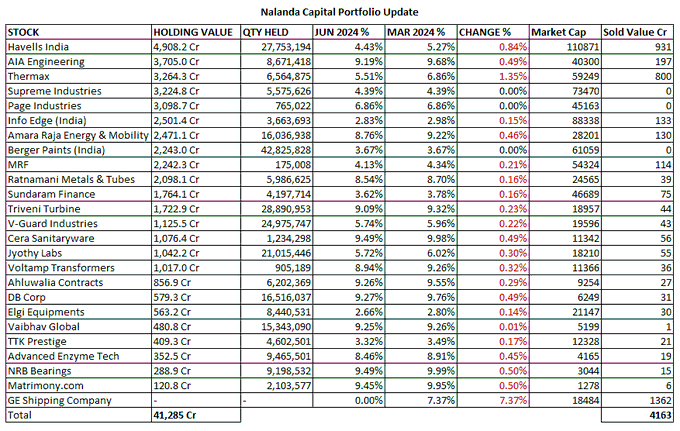

I follow this co. because it is part of Nalanda capital portfolio but I don’t think this co is currently undervalued or a ’ no brainer investment’.

Having said that I hardly know anything about the business and its growth prospects, my pov might not be right

other income is treasury (interest income) due to large cash in reserves. Company rerating may depend on ongoing upcycle in shipping industry, however downturn in share price currently is unlikely.

The old PE’s should not be considered as these shipping companies for first time is going to become debt free after many years just because upcycle has lasted bit longer this time… So their avg operating cost will be less than previous years…

I would be a bit skeptical about NAV consolidation at 1400 level, we are seeing a super cycle for shipping industry and it’s only matter of time before tides turn.

how can tides turn in short span when new ship orders are all time low?? any insight what could make tides turn, like war may end and sea routes may open, but shipping upcycle was prior to Israel war as well

Based on the forecasting by Value vessel we could see a surge in supply side of Tankers and LPG specifically VLGC. Given that GE is sitting on a huge cash reserve with minimal debt it would be interesting to see how they play this out. We can probably see further capacity expansion down the line.

Nalanda exited in किर्लोस्कर oil @ 125 two years back.

Now, the price of Kirloskar is ten times their exit price.

Henceforth, please do not make your entry or exit decision based on big funds…

I bought किर्लोस्कर after Nalanda exit and exited @3x of my buying price in less than one year.

Is this a good value stock? Available at 4.6 times earnings and 0.97 times book value. The Reserves+Cash Equivalents in the Balance Sheet (13356+5279) are significantly more than the entire Market cap (13033).

While it’s very near to its historic lows over past 30 years , it can go a little bit lower as it did during 2014 to 2016. In shipping things move slow …very slow. If you have patience and looking to accumulate for long term, it can be a good bet for multibagger returns but be aware that you may have to wait for years to see it .

It’s a cash rich company , and in this kind of low rates ,many ships would be in market to be sold …this is the time GE shipping would acquire ships for cheap which will come handy in next cycle.

Disc: Not invested . I do not have this much patience .

They are cyclical sellers if you see the past. They sell vessels at top of market and purchase when market is lower bound. If you see they have been selling vessels consistently last year, so they expect that market is at its peak.

So you will have to judge accordingly.

@Ghonarbochon

They do not majorly play on container side. They play more on dry and bulk and Oil ships.

Yes…the chart I gave is for Baltic dry .Had bought this one in 2021 at around 270 and sold out after a few months .Wish I had held it . I have already forgotten most of the knowledge I gathered then about the companies business details .