I understand that you’re much older than me so please behave like it and refrain from unnecessary name calling like this on a public forum from next time.

Anyway, thanks for sharing your thoughts on this topic, it made me delve into the whole situation and left me dumbfounded how misinformation is being spread across media.

-

First off, your argument that if you can exchange currency for something of value, then it certainly has value. This is a fundamental misunderstanding of the concept of intrinsic value versus perceived value. Unlike in the past, when currencies were linked to gold, they now lack innate value and are worth something because people think they’re worth something. (Even gold prices, as you rightly noted, are subject to market opinions and is not immune to speculative price shifts). This doesn’t mean currency has no value or that your bank balance is useless, but that its value isn’t based on a physical commodity but on market forces and trust. You’re confusing usefulness with inherent worth, a basic error.

The value of fiat currencies is entirely perception-based, stemming from trust in the issuing government and central bank. Hypothetically, if tomorrow confidence in a nation’s economy collapses (e.g., a hyperinflation scenario like Zimbabwe or Venezuela), the currency’s purchasing power evaporates regardless of whether it can still technically “buy” something. -

Now, coming onto your stance on imports, exports and inflation due to depreciation… Japanese yen has depreciated by nearly 25% since 2021, while the rupee has fallen by only ~10% in the same period. In this sense, RBI’s actions have protected Indian consumers and businesses from more severe inflationary shocks.

Yes, a weaker rupee raises import costs, particularly for oil. However, this must be weighed against the benefits of maintaining a competitive exchange rate for exporters. If the rupee were allowed to appreciate significantly (say, to ₹70/dollar), India’s export-driven industries—IT services, pharmaceuticals, textiles—would lose their pricing advantage. This would worsen the trade deficit, undermining economic growth.

Hypothetically, consider a scenario where RBI abandons interventions entirely. The rupee might depreciate to ₹95 or ₹100 per dollar due to speculative pressures or global uncertainties, leading to rampant imported inflation. Conversely, if RBI aggressively propped up the rupee to ₹75, exports would collapse, hurting GDP. Stability—not extremes—is the goal.

Also, the interpretation of sale of Foreign reserves by RBI as Foreign reserves being “lost” is very laughable. RBI deliberately sold it to keep the currency stable, it did not evaporate into thin air. Reports suggest that RBI may pay ₹2 trillion in dividends to the government due to profits from dollar sales at favorable rates—an indication that their strategy is yielding tangible benefits for the economy.

Additionally, Dr. Subramanian’s assumption that a freer-floating rupee would have spurred export growth ignores global headwinds such as slowing demand in key markets like Europe and China.

Moreover, you mention that companies with significant imports will suffer from reduced margins. While this is true for some sectors, it’s essential to recognize that many companies hedge against currency fluctuations through financial instruments. The idea that large corporations like Reliance or Tata do not manage their forex risks effectively is simply incorrect. They employ sophisticated treasury operations to mitigate such risks, ensuring their operations remain resilient even in volatile currency environments.

A knee-jerk reaction against RBI’s measures may reflect a pessimistic outlook rather than an informed understanding of India’s potential trajectory.

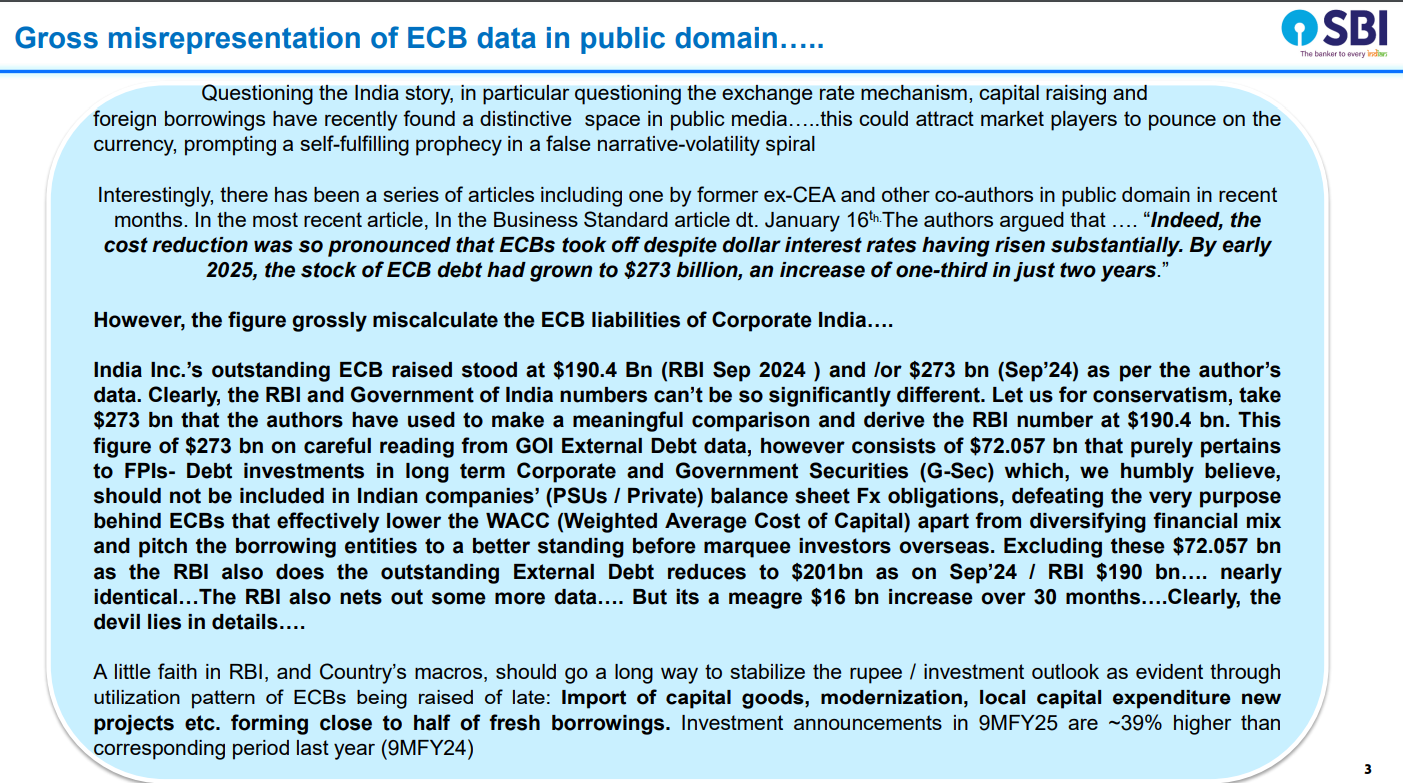

The context regarding ECB and high interest payments shared by Dr. Subramaniam (that you deleted later on ![]() ) is highly inaccurate and misinterpreted, showing Dr. Subramaniam’s unethical publications which are even addressed by SBI directly in their recent circular.

) is highly inaccurate and misinterpreted, showing Dr. Subramaniam’s unethical publications which are even addressed by SBI directly in their recent circular.

Most of the ECBs and FCTL loans are hedged whenever they are taken. Bank won’t allows the loan at all. Reliance Tata or Vedanta have big treasury they do hedge their risk, don’t spread wrong knowledge about the forex market. Please read this circular on ECB AND FCTL LOAN from RBI, Dr. Subramaniam is sharing inaccurate data just to make the headlines, according to him India is a lost cause now.

I stand by my original post that the RBI is taking the right steps to handle the value of the Rupee and I urge everyone to not get swayed by negative sentiments and stay confident about the growth story of India and its economy.

SBI report -

SBI report.pdf (899.1 KB)

I haven’t deleted any point related to ECB, in fact emphasised that the rupee dollar peg created ECBs that are going to create more problems as Re depreciated.

I edit my posts multiple times for clarity, so not sure what deletion you are referring to.

FCO to EBITDA a good tool to use for bottom picking in ![]() Market?

Market?

AVOID MACRO-TOURISM - highlight from today’s The Daily Brief

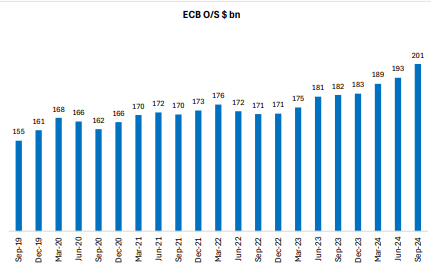

India’s foreign borrowings are not at all skyrocketing as claimed by Subramanian. Instead, they’ve went up by a mere $16 billion over 30 months. That’s far more normal.

India borrowed a lot more from abroad before the COVID-19 pandemic than it does today. In Fiscal 2020, ECBs made up 1.9% of our GDP. That number fell to 1.2% in Fiscal 2024. This could all be a simple matter of things returning to the pre-pandemic trend.

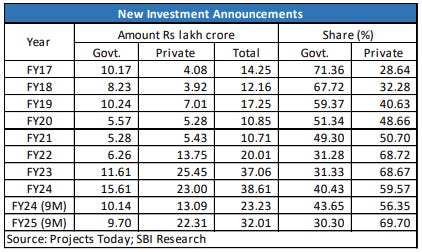

There’s another way of looking at things: Indian corporates may be borrowing more from abroad because they’re finally investing more in India.

For many years, India’s private sector held back from investing in the country. This has worried economists and policy-makers for many years.

But there are hints that this investment drought might be receding. According to SBI Research, there’s been a noticeable increase in the investments announced over the last few years. Much of this investment is led by the private sector, rather than the government. The first nine months of this year, for instance, saw investment proposals of Rs. 32 lakh crore — over 70% of which were private. This is well above pre-pandemic levels.

In Fiscal 2023, private gross capital formation reached its highest point since Fiscal 2016 — at 11.6% of our GDP. While data for Fiscal 2024 isn’t yet available, chances are, it’s increased even further.

It’s not just SBI Research, by the way. Late last year, Care Edge Ratings pointed to how capital goods companies have seen a large surge in orders in Fiscal 2024, which might be another positive signal.

The lesson? Avoid macro-tourism.

A number only has meaning when you attach a narrative to it. That narrative distorts the insight a number gives you. Economists at the pinnacle of their careers, too, have long, heated battles on individual numbers and what they mean. This is just one such battle. Lay people should expect to be confused by the mess of it all.

Many investors are drawn to macro-tourism. They make investment decisions by looking at high-level economic statistics and trends and using them to create hypotheses about an entire economy. Unfortunately, this is a terrible strategy — especially if you’re not used to digging deeper. All numbers have layers of context. If you don’t look for context, you’ll probably miss it. If you’re not aware of how exactly the nuances play out, you can end up going very, very wrong.

My thoughts

This piece is a bit harsh but hits uncomfortably close to home. While I’m optimistic about India’s long-term story, I remind myself of Howard Marks wisdom occasionally.

No asset is so good that it can’t be overpriced

Let’s focus on hard facts:

- Market Structure

- 8+ crore investors have never experienced a bear market

- MTF (Margin Trading Funding) at ₹80,000 crores

vs ₹8,000 crores in 2020

vs ₹8,000 crores in 2020 - Small & midcap valuations are above 2+ standard deviations median/mean

- SME Reality

- 90%+ businesses fail historically. Small businesses even more prone to failure, Yet SME valuations suggest near zero risk

- Current prices assume numerous small business will be future giants

- Basic probability suggests otherwise

- Narrative vs Numbers

- Growth stories are real, but not for everyone

- Current valuations assume success for all

- Historical data shows this never happens

- Momentum has overtaken mathematics

Looking Back:

Every time MTF peaked and small/midcap valuations crossed +2SD, markets taught expensive lessons. Not fear-mongering - just history.

This isn’t about being bearish. It’s about being realistic. True wealth creation happens when you survive the full cycle, not just the euphoric phase.

Navigating the Stock Market During Heavy Corrections: Lessons from the Greats

The stock market is a roller coaster—an exhilarating ride during the bull phase but equally terrifying when the inevitable correction sets in. Heavy market corrections can test the resolve of even the most seasoned investors. However, it is in these challenging times that some of the most valuable investing lessons come to light. Let’s explore the wisdom of legendary investors and their books to help us navigate these turbulent waters.

1. “Be Fearful When Others Are Greedy, and Greedy When Others Are Fearful” — Warren Buffett

Warren Buffett’s timeless advice emphasizes contrarian thinking. Corrections create panic, leading to irrational selling and undervalued opportunities. Buffett’s strategy of buying quality businesses during periods of market fear is well-documented in his annual shareholder letters and in the book “The Essays of Warren Buffett.”

Key Takeaway: Look for fundamentally strong companies with proven business models, competitive moats, and solid cash flows. Corrections often provide these gems at a discount.

2. “The Stock Market Is a Device for Transferring Money from the Impatient to the Patient” — Benjamin Graham

Known as the father of value investing, Benjamin Graham’s teachings in “The Intelligent Investor” highlight the importance of emotional discipline. Graham advises focusing on intrinsic value rather than short-term market noise.

Key Takeaway: Use corrections as an opportunity to revisit your long-term goals. Stick to your investment thesis and focus on buying undervalued stocks, not following the crowd.

3. “In the Short Run, the Market Is a Voting Machine but in the Long Run, It Is a Weighing Machine” — Benjamin Graham

This quote serves as a reminder that short-term price movements are driven by sentiment, while long-term prices reflect fundamentals. Corrections amplify this disparity, creating opportunities for savvy investors.

Key Takeaway: Separate short-term noise from long-term potential. If the fundamentals of a stock remain intact, a price drop could signify a buying opportunity.

4. “Investing Isn’t About Beating Others at Their Game. It’s About Controlling Yourself at Your Own Game” — Jason Zweig

Jason Zweig’s commentary in the updated edition of “The Intelligent Investor” stresses the importance of self-control. During corrections, emotions like fear and greed can cloud judgment.

Key Takeaway: Avoid impulsive decisions. Develop a disciplined investment process and stick to your strategy regardless of market volatility.

5. “The Four Most Dangerous Words in Investing Are: ‘This Time It’s Different’” — Sir John Templeton

Corrections often come with narratives suggesting that market conditions are unprecedented. Templeton’s wisdom, documented in “Investing the Templeton Way,” teaches us to recognize and resist such hyperbole.

Key Takeaway: Historical patterns often repeat. Market downturns have always been followed by recoveries. Use history as a guide to stay grounded.

6. “You Make Most of Your Money in a Bear Market; You Just Don’t Realize It at the Time” — Shelby Cullom Davis

Davis’s insight underscores the idea that the seeds of wealth are sown during market downturns. By buying undervalued stocks during corrections, investors position themselves for significant gains when markets recover.

Key Takeaway: Heavy corrections are an opportunity to build wealth. Maintain liquidity to capitalize on attractive valuations.

7. “Risk Comes from Not Knowing What You Are Doing” — Warren Buffett

Understanding what you invest in is crucial, especially during corrections. As Buffett often advises, avoid complex investments you don’t fully understand.

Key Takeaway: Stick to industries and companies you’re familiar with. This knowledge will give you confidence to hold or buy during volatile phases.

Actionable Steps During Corrections:

- Reassess Your Portfolio: Check if your holdings align with your long-term goals. Trim positions in over-leveraged or fundamentally weak companies.

- Stick to an Asset Allocation Plan: Diversify across asset classes to mitigate risk.

- Focus on Cash Flows: Invest in companies with strong balance sheets and consistent cash flows that can weather downturns.

- Maintain a Watchlist: List stocks you’ve always wanted to buy and take advantage of correction-driven discounts.

- Control Your Emotions: Use a checklist to guide your decisions and avoid panic selling.

Closing Thoughts

Heavy corrections are a test of patience, discipline, and conviction. By leaning on the wisdom of investing legends and focusing on fundamentals, you can turn these challenging phases into opportunities. Remember, every correction lays the groundwork for the next bull market—the key is to stay prepared and stay invested.

Things are changing too fast

we are trying to do 60 year missing infrastructure development in 15 years, it will be skewed. And these are capital intensive upfront costs. The entire stock market boom is predicated on infrastructure development, secular in nature i.e. across all fronts air, water, road, rail, power and mining. I don’t know who the guy is in the interview but he’s incorrect in the assessment and solution.

It appears that most orgs don;t believe in climate change and are doing lip service on that front with rumours of blackrock exiting netzero committments and the US Gov coming out of Paris accords.

Remember, whatever we do in solar, we are also planning to double coal output to 2B tonnes from the current 1B tonnes by 2030/35.

In short, the article doesn’t add value to how the economy should be directed

Has there been an article that was positive about the Indian stockmarket? I find SS post weird in the sense, that retail did the right thing in going through mutual funds to minimize their risks relative to direct investing.

Now to call them stupid is not a winning move even if you assume rampant misselling by AMFI.

Markets go in all directions and this is the first time I’ve seen MF funding still steady after 3-4 months of downturn. People are sticking to it and he has a problem with it?

All posts here are about staying the course and all the high advice but when you see an article saying you are stupid to stick to it, people agree to it?

Why?

so what’s the filter to put in screener to identify such companies, then?

Good article of the impact of DeepSeek on NVIDIA. Per this, even with the break of scaling law NVIDIA will thrive as the adoption of inference models will positively impact NVIDIA. This might have a positive rub off effect on the likes of E2E , Netweb and Yotta.

Even on training side, lot of new breakthroughs need to happen. What deepseek did was optimising for cost. The state of the art quality is still in similar levels as before, but the kind of models that are needed for AGI are still not in sight. So there is lot of work left to be done and AI ancillary demand depends on that as well.

The Art of Selling | Kuntal Shah | Oaklane Capital Management LLP | Co-founder - Needl.ai

Understanding the Payments Ecosystem