Good website to track the trends. (In US)

6 Likes

Sandeep Tandon from Quant Mutual Fund

- Valuations are rich but not expensive

- The easy phase of the bull market is over

- Churning is important in today’s world to generate alpha

- In the next 30 years, the relevance of the leverage economy will decline and the real economy will return.

- He already sold HDFC in Sep 2022

- They hold smaller banks like Karnataka Bank, RBL or J&K trading close to their book value.

- Pharma, metals and mining are in the neglected category and can perform well in the next 3 years

- PSU rally has still some legs left as people are still owning with hesitation.

- Overweight on Reliance

4 Likes

Could you please elaborate on this bit? Thanks.

He has not described it in detail. He said this will be covered in his upcoming book. Maybe what he meant was the concept of increasing the purchasing power of people through credit (leverage economy?) will decline. Banks are the biggest beneficiaries of this leverage economy. As per their thesis, they are also bearish on the US in the long term.

Time: 7:50

Sounds like a deeply contrarian view. If Credit/Leverage slows down (deleveraging – are we on a credit bubble?) GDP too will slow down, no?

His thesis seems to sectors of real economy (power, metals, manufacturing, commodities) will outperform financials over the next decade, and on the other hand, we have every other MF have highest allocation to Financials.

This PDF has good insights into the emerging trends in India.

4 Likes

Yeah. This part I also didnot understand. What I interpreted is , may be he is saying banking and credit companies will not prosper and ppl will take less leverage in future . But this is totally against what everybody says. Ppl and most economists say that high credit system is required for an economy to prosper. If some expert people can break this down for us, mortals pls

3 Likes

This seems to be happening. The stocks related to Steel, Iron Ore, Coal have already moved up from Below Book Value to P/B of 2.0 to 3.0.

No one was talking about this 2 years back.

This is reversion to mean which has happened.

Banking and Credit Business should continue to prosper for next decade as the habit of people can not change over time unless their are major calamities, wars and unpredictable situations. These situations could surface during 2024 and hence caution is needed at an individual level, but mostly broader trend of spending beyond your limits should continue.

Saving rates are already at the lowest so they may not go down but still Credit growth story looks intact.

This is my personal opinion and could be wrong.

3 Likes

So neglected that they are at or near all time highs? ![]()

4 Likes

A good report on fintechs by Elevation in partnership with McKinsey:-

2 Likes

Nicholas Sleep and his partner Qais ‘Zak’ Zakaria, two young analysts with strong opinions about the investment industry who started their own partnership, Nomad Investment Partners. The two partnered up (first under the Marathon umbrella) and, from 2001 to 2014, crushed the market.

They did what they loved: studying companies, talking to operators, reading broadly to accumulate worldly wisdom, and reflecting deeply on what they learned. They practiced their craft with a dedication to quality, curiosity, introspection, long-term focus, and ethical partnership with their investors.

5 Likes

Created a bias sanitization checklist using chatgpt Charlie Munger’s talk on human misjudgment and Robert Cialdini’s book Influence this is what I got.

-

Awareness of Decision-Making Process:

- Have I clearly outlined the steps in my decision-making process?

- Am I consciously reflecting on each stage to ensure objectivity?

-

Emotional Check:

- Have I assessed my emotional state and its potential impact on decision-making?

- Am I making decisions under stress, fear, or other emotional influences?

-

Information Gathering:

- Have I sought information from diverse and reliable sources?

- Am I actively avoiding information that confirms pre-existing beliefs?

-

Time Perspective:

- Have I considered both short-term and long-term consequences of the decision?

- Am I avoiding impulsive decisions without sufficient future-oriented thinking?

-

Framing and Language:

- Have I examined how the decision is framed and the language used to describe it?

- Could a different framing or language influence my perception of the decision?

-

Anchoring:

- Am I being unduly influenced by an initial piece of information or an anchor?

- Have I critically assessed whether the anchor is relevant and justified?

-

Cultural and Societal Influences:

- Have I considered how cultural and societal norms might be affecting my decision?

- Am I making decisions that align with personal values rather than succumbing to societal pressure?

-

Power Dynamics:

- Have I analyzed the power dynamics involved in the decision-making process?

- Am I aware of any potential biases introduced by hierarchical structures or authority figures?

-

Group Dynamics:

- If in a group decision, have I ensured that groupthink and conformity are minimized?

- Have I encouraged diverse perspectives and dissenting opinions?

-

Reflection on Past Decisions:

- Have I learned from past decision-making experiences and any associated biases?

- Am I applying lessons from previous mistakes to enhance the current decision-making process?

-

Alternative Scenarios:

- Have I considered alternative scenarios and potential outcomes?

- Am I open to adjusting my decision based on changing circumstances or new information?

-

Ethical Considerations:

- Have I thoroughly examined the ethical implications of the decision?

- Is the decision aligned with ethical standards and principles?

-

Feedback Seeking:

- Have I actively sought feedback from others to challenge my perspectives?

- Am I open to constructive criticism and differing viewpoints?

-

Decision Reversibility:

- Have I considered the reversibility of the decision?

- Can the decision be easily adjusted or reversed if necessary?

-

Systematic Review:

- Have I systematically reviewed all aspects of the decision-making process?

- Is there a structured framework in place to evaluate the decision comprehensively?

-

Lollapalooza Effect:

- Have I examined the decision for a potential convergence of multiple biases leading to an exaggerated impact?

- Is there a combination of psychological tendencies that might be influencing the decision?

-

Incentive-Caused Bias:

- Have I considered how personal incentives might be affecting my judgment?

- Am I making decisions based on the best interest of the situation rather than personal gain?

-

Contrast Misreaction:

- Have I evaluated the decision in absolute terms rather than comparing it to other unrelated situations?

- Is my judgment influenced by recent events or extreme comparisons?

-

Learning from Multiple Disciplines:

- Have I sought insights from various disciplines to broaden my perspective?

- Is my decision-making process informed by a multidisciplinary approach?

11 Likes

Great to read by Ashwini - VP beneficial. Not sure he is active or not here, I have some general questions and wishes to ask him…

6 Likes

Best 2024 Report to read.

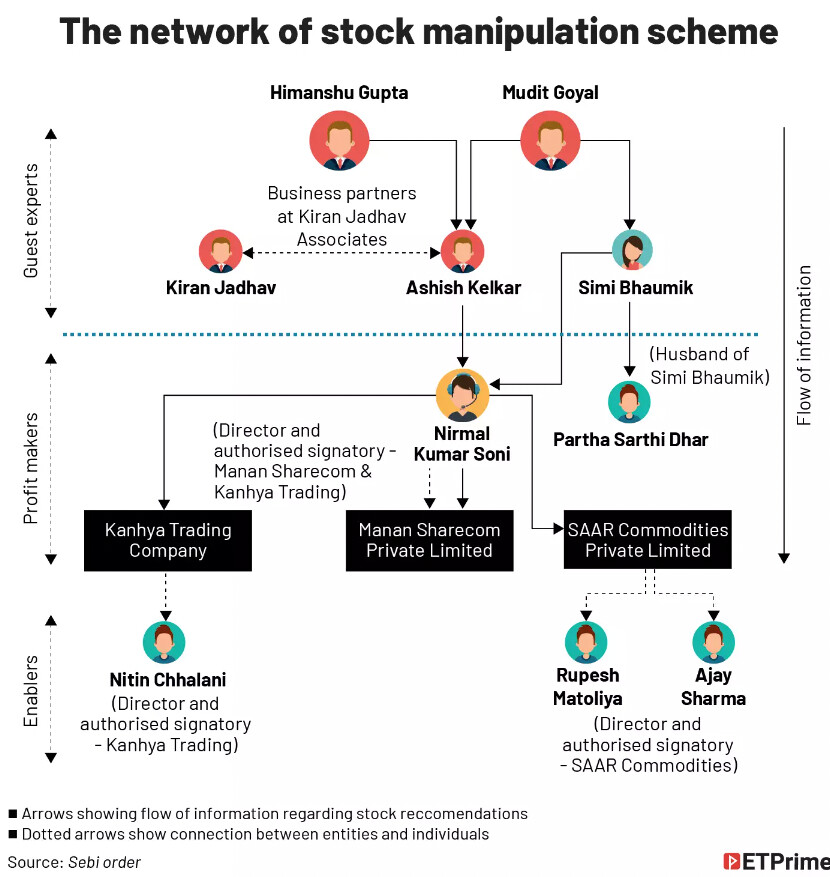

There is book titled as “what they don’t teach you at harvard business school”, same the sebi report of zee guest is like what investing book don’t teach you.

Every investor should read the report. How smart our agency (SEBI) is, they illustrated call, chat, relationships, trade details in great details.

6 Likes

A good Q&A with Ajay Tyagi who manages some of UTI’s largest funds. It’s from November 2023.

https://www.valueresearchonline.com/stories/53474/valuation-alone-never-excites-us-ajay-tyagi-of-uti-amc/

3 Likes

2 Likes

Have been reading this over the weekend. A lot of the thought process is completely opposite of how we retailers react and read.

A guide to navigating quarterly noise-flow (substack.com)

Pointing out couple of core paras rather than making my points, Below is taken verbatim from the essay.

View each quarter as one more datapoint in a continuing trajectory, not in isolation.

""Answer starts with making such pictures, so as to internalise inherent lumpiness of long-run trajectories of good businesses. And then incorporate the same into short-run expectations. Use business history, rather than strangers’ estimates, as our guide to analysis of quarterly financials. Realize that that even the act of producing precise quarterly estimates is as arrogant as it is futile. Over the long run, good business invariably do fine, while following a path that is assuredly and extremely volatile. To borrow Pulak’s quote, “Nothing goes up in a straight line”.

Since all trajectories are bumpy, keep wide bands.

Awareness of long-run trajectory makes a compelling case for banning ‘basis points’ as unit of financial analysis. Plus or minus 25% swings in typically tracked metrics (revenue growth, EBITDA margin %) are a feature not a bug. For a company with 15% long-run average margin, a 12% or 18% quarter is normal, not exceptional. Ditto for revenue growth or working capital intensity. Explanations for deviations sound plausible but are actually made-up, usually to fob off pesky questioners on conference calls.

Approach financial results with wide error bands around a general long-term trend. Swings within this band generally merit a shrug of the shoulders, not activation of neurons.

Focus on controllables: relative over absolute performance, balance sheet over P&L.

Companies have little control over the metrics we obsess over – revenue and profit growth – at least over the short run. These are determined by industry growth, stage of business cycle, commodity inflation, exchange rates and base-period. Often, these effects are extreme.

6 Likes

Its behind a paywall…not able to access.