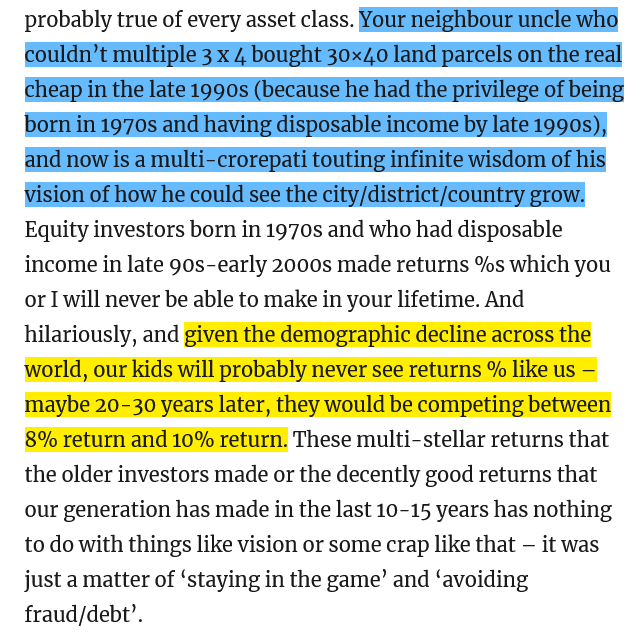

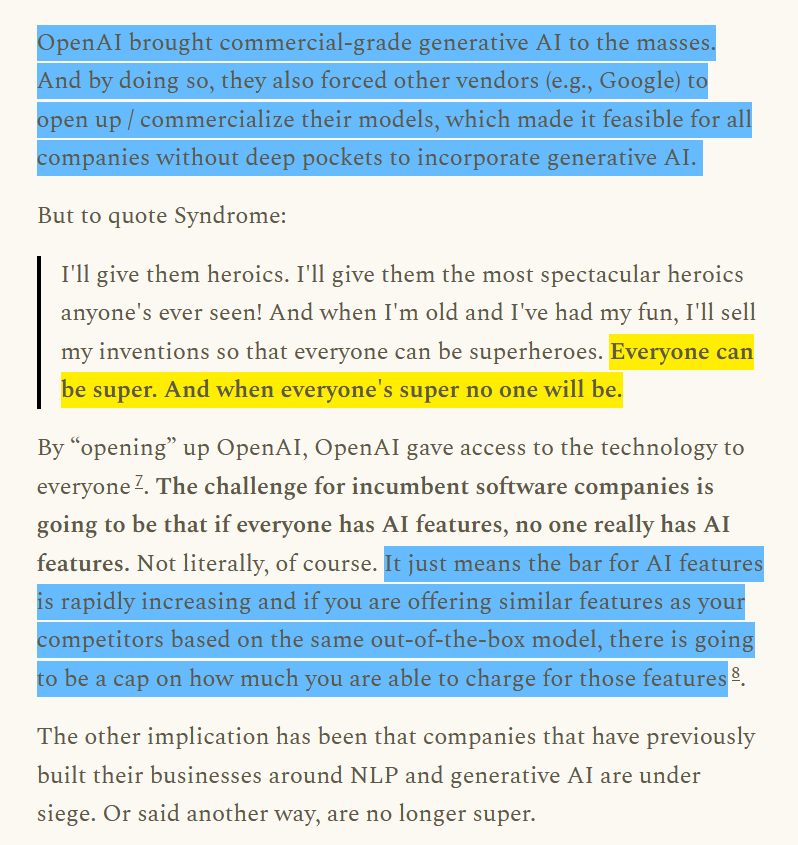

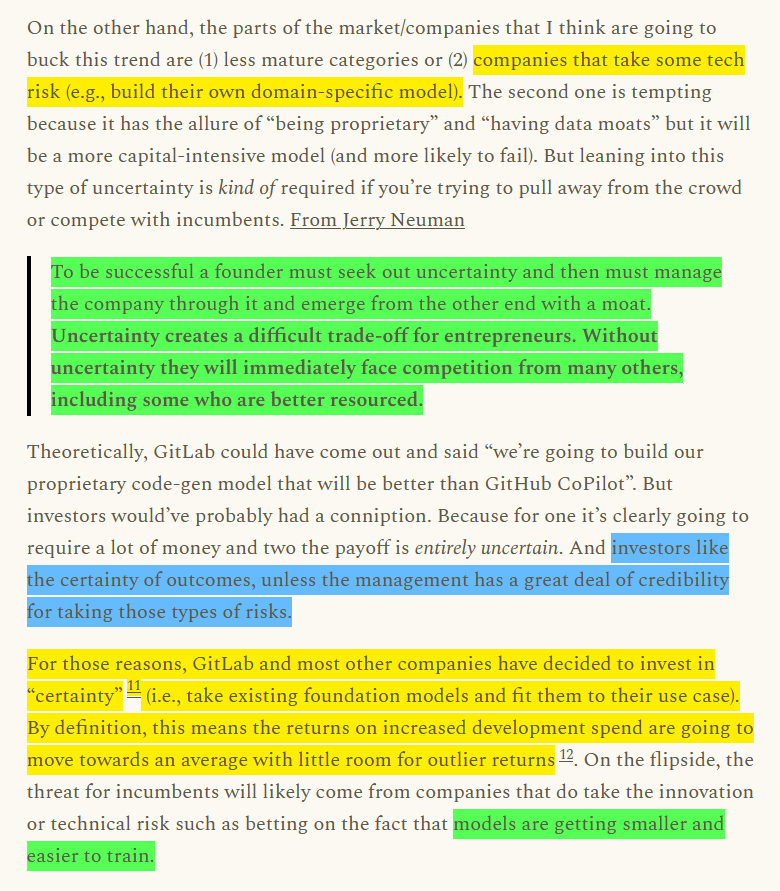

Investment Masters' wisdom")

2 Likes

- Investment Master's Wisdom Series")

5 Likes

Good global and Indian overview is given in the paper “Road Less travelled”.

PC_-GV_monthly_newsletter-_Apr_2023_20230428101145.pdf|attachment (949.2 KB)

3 Likes

Detergent dilemmas

Surfactant manufacturers don’t seem very happy these days. Surfactants are active ingredients used in cleaning detergents.

.

And recently, the government’s been mulling over discouraging foreign raw materials to protect the local industry. But this good gesture is giving them nightmares.

.

What’s going on, you ask?

.

Well, saturated fatty alcohol or SFA is a kind of surfactant that commonly goes into making detergents. And most of it is imported because India doesn’t produce enough of it to cater to the large surfactant-absorbing industry which includes personal care products like soaps, skin cleansers, shampoos, stain removers and more.

.

And India’s needy surfactant industry is almost like a golden opportunity for other countries that produce low-cost SFAs and send them over. In other words, they just dump their cheap products in India.

.

In 2017, the government started looking into the alleged dumping of SFAs from Indonesia, Malaysia, Thailand and Saudi Arabia. These imports were actually leaving harmful residues that polluted local land and water. And because they had sufficient evidence to prove their speculations, the commerce ministry’s investigation arm thought of choking such hazardous imports with anti-dumping duties.

.

And folks in the surfactant industry never okayed this move because discouraging imports meant having to procure SFAs locally. But since there isn’t enough potential to meet all this demand, production costs will naturally rise. And eventually, trickle down into pricier detergents and shampoos for consumers.

.

Another trouble could be with importing something called SLS (Sodium Lauryl Sulfate) which is a byproduct of SFA. If duties are imposed only on SFAs and not on other surfactants like SLS, it will make the local surfactant industry uncompetitive. Because some detergent manufacturers might simply resort to importing cheaper SLS as a workaround, bypassing buying SFAs from Indian surfactant makers altogether. This could compel them to resort to cutting back on expenses triggering layoffs. That could threaten the jobs of nearly 9,000 people employed in the industry too.

.

And that’s more or less why folks in the domestic industry are urging the government not to make this backfiring move.

Via Finshots

7 Likes

The CPU hack to stop wasting money

Hey! Do you often find yourself spending on stuff that you don’t need?

.

Fret not. Here’s a fab idea to get you out of the money-wasting loop. It’s called the CPU rule. And that just means cost-per-use or understanding how much something actually costs you every time you use it.

.

Let’s break it down for you.

.

Imagine you saw a cool pair of sneakers at a store. And because you recently got a pay hike, you go for it without a second thought. But you can’t wear them every day because they just aren’t that kind of footwear. Maybe you could wear it for casual outings. And you do that just twice a month. Which means you’ll only wear them 24 times a year.

.

Now if the sneakers cost ₹8,400, that’ll mean that every time you wear them you’ve spent about ₹350. But what if you had bought a more comfortable daily wear kind of footwear that you could pretty much wear all the time?

.

It would obviously cost you less. But just for the sake of comparison, even if it cost the same as that fancy pair of sneakers, you’d still have worn them at least 4 times a week. Meaning, 208 times a year. How much would the cost per use be then?

.

Just about 40 bucks!

.

How does that make you feel?

.

If it blew your mind away, then try using this analysis every time you’re lured into buying things that may not actually be financially beneficial. It could go a long in helping you cut down on your money-wasting vice.

Via Finshots

7 Likes

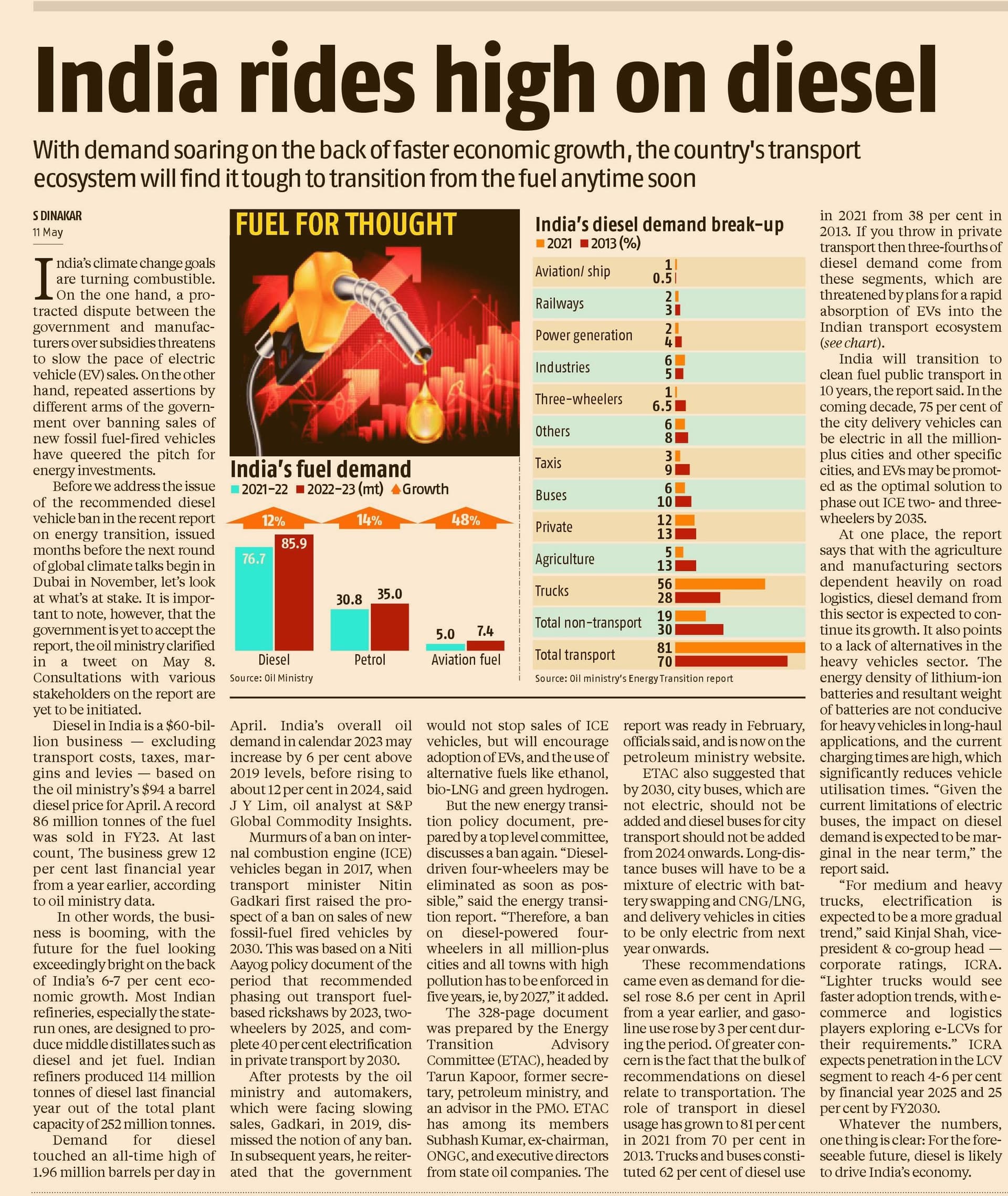

How India Become an Oil Exporting Nation after Russia Oil Cap Sanctions , Source: Trendlyne

Over the past few decades, major geopolitical events usually led to sharp fluctuations in oil prices – the US invasion of Iraq (which triggered a 49% jump in oil prices from March 2003 to March 2004), the Afghanistan crisis (58% up from September 2001 to September 2002), and sanctions on Iran (43% up from September 2010 to September 2011).

Each of these events disrupted the crude oil supply chain. The usual pattern was this: developed nations would impose sanctions on an oil producer, and developing economies would struggle with high oil prices, and rising fiscal deficits.

The ongoing Russia-Ukraine conflict is the latest example, where many analysts expected $100 oil after the US and Europe stopped energy purchases from Russia.

But instead of the usual blanket ban, this time the G7 countries took a softer stand by capping the Russian oil price at USD 60 per barrel. The sanctions are meant to ensure lower revenues for Russia, without hampering the oil supply chain.

Many countries are also not complying with the price cap:

By continuing to buy Russian oil despite EU and US boycotts, India and China have become major refined oil exporters.

In this week’s Analyticks:

![]() Oil politics: India is on the winning side of oil politics, for a change

Oil politics: India is on the winning side of oil politics, for a change

![]() Screener: Stocks that beat analyst estimates for revenue and net profit in Q4FY23

Screener: Stocks that beat analyst estimates for revenue and net profit in Q4FY23

Let’s get into it.

India’s deep thirst for cheap Russian oil

The price cap on Russian oil has caused its Ural crude to trade at 40% below the international benchmark, Brent crude. In the first quarter of 2023, Russian Ural oil averaged USD 51.05 per barrel, while Brent crude oil was priced around USD 81.91.

India’s economy is highly susceptible to oil price fluctuations. A report by Edelweiss suggests that a 10 dollar increase in oil prices causes a current account deficit of 0.5% of India’s GDP. If India were to replace its entire import crude basket with Russian Ural, its current account deficit could contract by 1.6%-1.7% of GDP.

The landing cost (including freight and insurance) of Russian Ural for India was roughly USD 70 in March. India and China are snapping up cheap Russian crude in large quantities - Russia currently accounts for nearly 40% of India’s crude imports, while China has increased its Russian oil imports by 22%.

The Middle East’s oil producers have been at the receiving end of this, and saw their share of Indian oil imports drop sharply.

Sooner or later, Middle Eastern refiners may need to revise their official selling price to compete with Russia.

The increased demand for cheaper Russian Ural has pushed its prices past the $60/barrel cap imposed by the G7, and the price differential between Russian Ural and Brent had narrowed to 20% by the end of April 2023. Finance Minister Nirmala Sitharaman has said that India is going to keep buying Russian oil past the price cap, as long as it remains cheaper than Brent crude.

Can India increase Russian oil imports?

India increased its Russian imports from 67,500 barrels/day in January 2022 to 2.1 million barrels/day by the end of April 2023. Russia is now India’s single major source of oil supply. Whether India can increase its Russian oil imports further is a complex question.

India has struggled to find an alternative currency to the US dollar for purchasing Russian crude oil. Russia’s removal from the international SWIFT payment system has made dollar transactions difficult, and exposes India to potential sanctions. Trading in INR is impractical, as Russia is a net exporter to India; receiving rupee payments would leave Russia with an excess of rupees and no way to spend them.

For now, Russia and India are trading in UAE Dirhams, which helps to a certain extent as it is pegged to the dollar. But this does not completely solve the INR depreciation issue. UAE is a net exporter to India, so India buying more Dirhams for Russian trade will cause the INR to depreciate against the Dirham.

India also cannot stockpile much Ural oil due to its limited strategic petroleum reserve of 5.33 MMT, which covers only about 9.5 days of national demand. In contrast, countries like China have significant reserves that can meet nearly 50 days of their national demand.

A potential solution for India is to rapidly refine and export more Russian oil. But Indian oil refineries are operating at full capacity, with overall capacity utilization exceeding 100% since May 2022. In January 2023, capacity utilization reached 106.9%, and state-run firms like Indian Oil Corporation reported even higher figures at 110%. India cannot increase oil exports without investing in additional capacity expansion projects.

Russian oil wears an Indian disguise, as India becomes the top fuel exporter to Europe

The European Union banned seaborne crude imports from Russia starting from February 2023. At the time, Russia accounted for nearly 30% of European crude imports.

While the US has increased its crude oil exports to Europe by more than 70%, it is unable to meet all of Europe’s needs. So Moscow is rerouting Russian oil to Europe via refineries in India, China, Africa and the Middle East. India has become the hub for sending Russian Ural to Europe as refined oil.

India’s oil refineries are processing and exporting Russian crude to Europe. India supplied roughly 3,65,000 barrels per day to Europe in April 2023, an increase of 187% since the start of the Russia-Ukraine war in February 2022.

Data Source: Kpler and Bloomberg

Data Source: Kpler and Bloomberg

However, India cannot completely substitute Russian oil exports to Europe, which averaged around 1.1 million barrels per day before the start of the conflict. India is limited here by its refining infrastructure.

The idea behind the sanctions was to cripple Russia’s revenue source without completely cutting off the global oil supply. The plan has worked, but it’s not been foolproof. Russia is still making money, just not as much. Oil supply to Europe has continued, but routed through India and China. For the first time, countries like India and China, which used to be victims of international oil politics, are gaining from this oil war.

14 Likes

One can sense a change in the direction of American economy.

some excerpts:

There was one assumption at the heart of all of this policy: that markets always allocate capital productively and efficiently—no matter what our competitors did, no matter how big our shared challenges grew, and no matter how many guardrails we took down.

Now, no one—certainly not me—is discounting the power of markets. But in the name of oversimplified market efficiency, entire supply chains of strategic goods—along with the industries and jobs that made them—moved overseas. And the postulate that deep trade liberalization would help America export goods, not jobs and capacity, was a promise made but not kept.

It’s about making long-term investments in sectors vital to our national wellbeing—not picking winners and losers.

The Financial Times has reported that large-scale investments in semiconductor and clean-energy production have already surged 20-fold since 2019, and a third of the investments announced since August involve a foreign investor investing here in the United States.

We’ve estimated that the total public capital and private investment from President Biden’s agenda will amount to some $3.5 trillion over the next decade.

Or consider critical minerals—the backbone of the clean-energy future. Today, the United States produces only 4 percent of the lithium, 13 percent of the cobalt, 0 percent of the nickel, and 0 percent of the graphite required to meet current demand for electric vehicles. Meanwhile, more than 80 percent of critical minerals are processed by one country, China.

At the same time, it isn’t feasible or desirable to build everything domestically. Our objective is not autarky—it’s resilience and security in our supply chains.

Now, building our domestic capacity is the starting point. But the effort extends beyond our borders. And this brings me to the second step in our strategy: working with our partners to ensure they are building capacity, resilience, and inclusiveness, too.

Now, our cooperation with partners is not limited to clean energy.

For example, we’re working with partners—in Europe, the Republic of Korea, Japan, Taiwan, and India—to coordinate our approaches to semiconductor incentives.

Fundamentally, we have to—and we intend to—dispel the notion that America’s most important partnerships are only with established economies. Not just by saying it, but by proving it. Proving it with India—on everything from hydrogen to semiconductors. Proving it with Angola—on carbon-free solar power. Proving it with Indonesia—on its Just Energy Transition Partnership. Proving it with Brazil—on climate-friendly growth.

We know the problems we need to solve today: Creating diversified and resilient supply chains. Mobilizing public and private investment for a just clean energy transition and sustainable economic growth. Creating good jobs along the way, family-supporting jobs. Ensuring trust, safety, and openness in our digital infrastructure. Stopping a race-to-the-bottom in corporate taxation. Enhancing protections for labor and the environment. Tackling corruption. That is a different set of fundamental priorities than simply bringing down tariffs.

3 Likes

Explains the US Banking crisis in very simple and layman terms.

3 Likes

4 Likes

From McKinsey Quarterly:

Hydrogen as a climate solution is generating a lot of excitement right now. Approximately $10 billion worth of hydrogen projects are being announced each month, based on activity over the past six months. Policy packages such as the recent Inflation Reduction Act in the United States and the Green Deal Industrial Plan in Europe support hydrogen production and use. According to McKinsey research, demand is projected to grow four- to sixfold by 2050. Hydrogen has the potential to cut annual global emissions by up to 20 percent by 2050.

Today, most hydrogen is produced with fossil fuels. This type is commonly known as grey hydrogen, which is used mostly for oil and gas refining and ammonia production as an input to fertilizer. To maximize hydrogen’s potential as a decarbonization tool, clean hydrogen production must be scaled up. One variety of clean hydrogen is known as green hydrogen, which can be made with renewables instead of fossil fuels. Another variety, often called blue hydrogen, can be produced with fossil fuels combined with measures to significantly lower emissions, such as carbon capture, utilization, and storage. Clean hydrogen has the potential to decarbonize industries including aviation, fertilizer, long-haul trucking, maritime shipping, refining, and steel.

Total planned production for clean hydrogen by 2030 stands at 38 million metric tons annually—a figure that has more than quadrupled since 2020—but there is a long way to go to meet future demand. According to McKinsey analysis, demand for clean hydrogen could grow to between 400 million and 600 million metric tons a year by 2050.

To scale clean hydrogen, three things must happen. First, production costs need to come down so that hydrogen can compete on price with other fuels. One way to keep costs down is by producing hydrogen in locations with abundant, cheaper renewable energy—where the wind blows or the sun shines. While renewables development has accelerated in recent years, a lack of available land could become an issue for the deployment of renewables and could limit location options for green-hydrogen producers. Constructing plants for both renewable generation and green-hydrogen production has become more expensive recently because of increased material and labor costs and constrained supply chains.

Second, building up infrastructure, particularly for transportation of hydrogen, will be key. The most efficient way to transport hydrogen is through pipelines, but these largely need to be built or repurposed from current gas infrastructure. Investment is critical in this and other areas across the value chain, including electrolyzer capacity (electrolyzers use electricity to produce green hydrogen) and hydrogen refueling stations for hydrogen-powered trucks.

Third, more investments will be needed to help advance this solution. Our work with the Hydrogen Council, a CEO-led group with members from more than 140 companies, has shown that achieving a pathway to net zero would require $700 billion in investments by 2030. Despite the recent momentum, McKinsey research last year showed a $460 billion investment gap. Additionally, many announced projects still need to clear key hurdles before they can scale. Producers of clean hydrogen, for example, are looking to address the commercial side of investment risk by solidifying future demand, often in the form of purchase agreements.

A set of actions can help accelerate the hydrogen opportunity, to realize its decarbonization potential and the growth opportunity for businesses. Progress will likely require collaboration among policy makers, industries, and investors. Policy makers can continue supporting the hydrogen economy through measures such as production tax credits or by setting uptake targets. These actions should help boost private investors’ confidence in the future markets for hydrogen and hydrogen-based products. Industry can increase capacities, such as by ramping up production of electrolyzers, and build partnerships through the value chain. Investors can help industry by structuring and financing new ventures, as well as by developing standards for how hydrogen projects can be assessed and how risks can be managed.

As the energy transition unfolds, hydrogen will increasingly be a consideration for both businesses and governments. While the challenges to scaling hydrogen are real, so are the opportunities.

Green energy business: The next moves for leaders | McKinsey

4 Likes

Agassi’s & Phil Knight’s Ghostwriter on writing other people’s memoirs.

Warning: Nothing to do with investing or business.

1 Like

Li Lu talk at the Columbia University great talk https://www.youtube.com/watch?v=-jF5au0-JiY&ab_channel=ChaseChimichurri

Summary of What I Learned

-

To be a successful investor you have to think like an Investigator Journalist

-

You have to work very very hard, read a lot, a lot.

-

Think Like an owner of a business

-

Have a checklist and if you have a checklist add this question in your checklist

What I am missing about the company?

8 Likes

Transformers 101 (Woh AI/ML wala, not electrical step down/step up ![]() )

)

Not too technical, not too oversimplified.

2 Likes

Interesting talk; some points I noted –

What determines a country’s success

- Peter Zeihan says that what determines a country’s success is geography their demographics and their energy their ability to produce energy

- Olsen is more likely to attribute a country’s success to its quality of Institutions and

- Balaji is more likely to attribute a country’s success to its IQ into its talent and its technology advancement

- It is certainly possible to squander good geography and if one wants the best proof of that I think geopolitical thinkers have expected Brazil to become a world power any decade now for the last 120 years and it perpetually underperforms because of dysfunctional institutions

- In the 1960s when France was still an optimistic forward-looking economically growing country Charles de Gaulle said IQ is the oil of France

China

- China can almost feed itself China produces over 90 percent of the wheat rice and corn it consumes as well as over 85 percent of the meat it consumes it is a bit less independent on the production of soybeans but soybeans can be substituted for other crops

- China is about 0.08 hectares of arable land per person this is to be fair six times less than the United States which has 0.48 but it’s not that far away from say the European Union which has 0.22 hectares per person really

- China plus Russia are an alternate economic base and that’s why they’re even flirting with interesting ideas like replacing the US dollar

- There’s a reason that in modern China they actually have less of an intellectual justification of disruptive capitalism or technological progress than the United States does yet because the rates of growth were higher in living memory most Chinese who are positively predisposed towards the future – they think the future is going to keep getting better and better technology and progress

Demise of dollar

- I think the dollar has performed very well actually compared to all other Western currencies so my view would be within the Western Alliance and within the Western system the United States will continue to grow in relative importance

- Even if it declines as the premier world currency I think it will be a strong currency for like a very long time

- My key disagreement with some of my say more more libertarian or crypto inclined friends because they think that if you crash the world Empire the currency goes away and I’m like nah you know it’s much more gradual

AI

- Peter Thiel famously said that crypto is libertarian AI is communist

- I think that AI is a communist as in it improves planned economies and planned economies of scale; that doesn’t necessarily mean that it must end in say like a state-controlled economy

- AI will push towards greater economic centralization

- What automation usually is is not that our tools become smarter it’s like we figure out how to do something that previously required intelligence and now can be done by a system that’s not very smart

- You actually have to slightly de-automate to reduce energy usage

Upcoming research interests

- Chinese nuclear industry: understanding about one of the most important questions of the near future is the Chinese nuclear industry. It remains to be seen whether it can fulfill the extremely ambitious plan set by the Chinese government to build 500 nuclear reactors; it is the kind of scale where those reactors are going to become cheaper and more reliable over a decade or two and make China a much less fossil fuel dependent

- Banking crisis: I think is not over I think we’re seeing like a slow motion burn that will require deep reforms of the U.S financial system for now let’s say the government has been successful in slowing it down but not stopping I feel the dominoes still are slowly ticking on each other and another relevant dive will actually be on

- Artificial intelligence: we have done extensive research onto the future

- Battery production: I’m already fairly convinced that solar energy is – in the absence of nuclear – an energy Revolution that decreases daytime energy costs. The only question is will the advances in Battery Technology keep up or will we see a world where you know during the daytime our power is powered by solar and at night we burn natural gas

6 Likes

Report on India’s renewable energy deployment.

-

Indian government to generate 50% of the installed capacity for electricity generation to be from renewable sources by year 2030

-

Only 5 states have been able to achieve their target for developing their renewable energy sources.

-

Dicoms are managed by the state government and vote and voter politics, causing subsidized electricity to be provided to end customers which causes a financial burden on discoms and invariably on power generators. Though the government is taking steps to mitigate these issues.

the report contains a much more detailed description of the above points many interesting facts and figures

IndiaRenewableEneryDeployment.pdf (224.4 KB)

3 Likes

5 Likes