Stanley Druckenmiller - “The risk-reward for equity is maybe as bad as I’ve seen it in my career.”

1 Like

Mr. Raghuram Rajan clearing the air on what happens when government borrows directly from the RBI.

2 Likes

4 Likes

FY21 To Be A Washout Year For Indian Corporates: Kenneth Andrade

1 Like

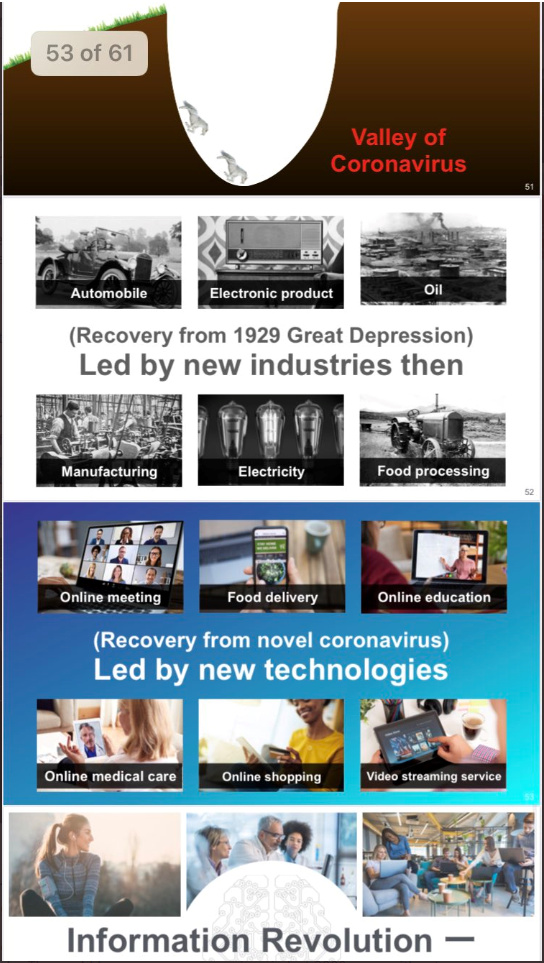

There is nothing remarkable about new technology shown, except adding word ‘Online’, how can that simply make recovery? Softbank may be a bit soft in the head…

You buy the same amount of groceries whether online or offline, the supply chain is more efficient, Amazon competes on that (more automation etc.), which means overall less money for intermediaries (read: human workers).

There has to be something extra, which adds more to the demand. I do not go to shops because online provides me more choice and convenience, do not even mind paying (little) more. This is the value-addition case. (Cheaper cars, better than horses etc.)

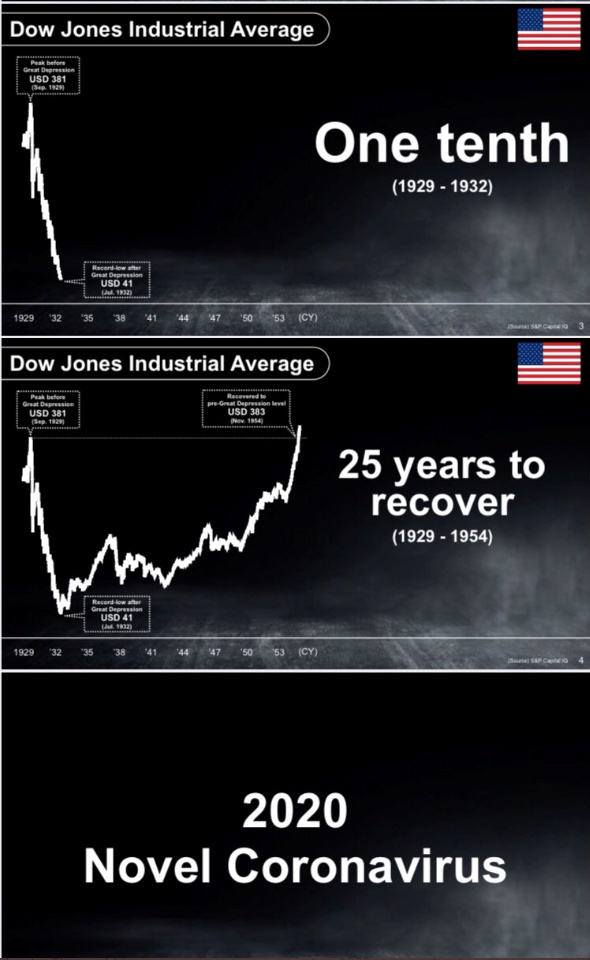

Good comparison to the Great depression, we seem to be doing some of the same wrong things which lead to the depression becoming Great (long and deep). There was the “Liquidationism” which said the best way to reallocate resources efficiently is to allow businesses to go bankrupt and be liquidated. Here we are deploying the IBC aggressively, without considering overall impact on the business cycle/confidence.

Then there is the great need to balance the budget which seems to be the most basic reason why it took so long and waited till the demand/spending of WW2 to fundamentally change the curve of depression to a recovery.

This is exactly the defensive budgeting we see the govt doing. It helps the top wealth-holders only, their holdings are not diluted, and the biggest/best can always borrow, but there is no demand growth in this and so overall recovery will be muted/lethargic. Conservative leaning policies can be destructive to wealth creation (‘gold-standard’ being an example). Money supply is one obvious biggest push required, but our banking system is too conservative to allow a big push in this direction. We seem to be trying to keep rating agencies happy (which again only helps a select few in international borrowings/deal-making, Adani, Reliance, to name a few).

RBI is too conservative forever keeping its eye on the inflation targets, US Federal Reserve publicly apologized for not being aggressive in the liquidity/money supply to save businesses and accepted blame for the Great depression. But promised never to allow that to happen again, praising economic studies which pointed out this problem.

1 Like

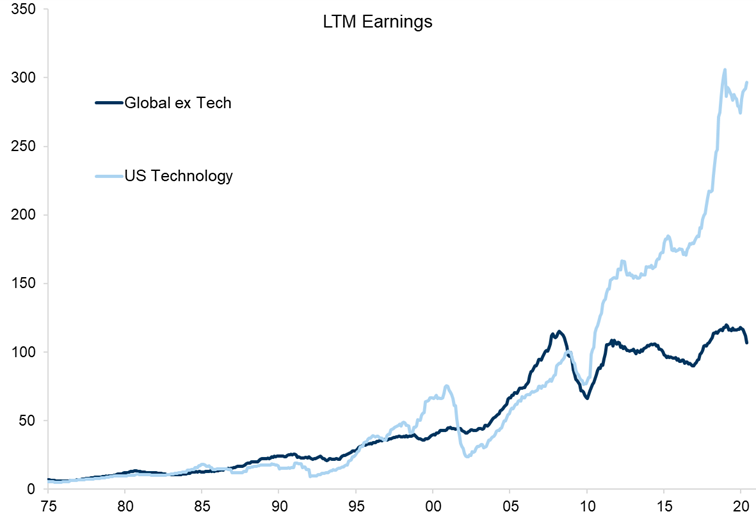

Social capital 2019 annual report. Speaks a lot about breaking big tech giants into smaller ones to end the monopoly.

Ramesh Damani In Conversation With Rupal Bhansali of Ariel Investments, USA.

Very good perspective from Rupal on FAANG stocks, Telecom, where she finds value and her view on Indian stocks etc…Liked her thought process.

BTW, she has written a book titled “Non-consensus investing”.

9 Likes

1 Like

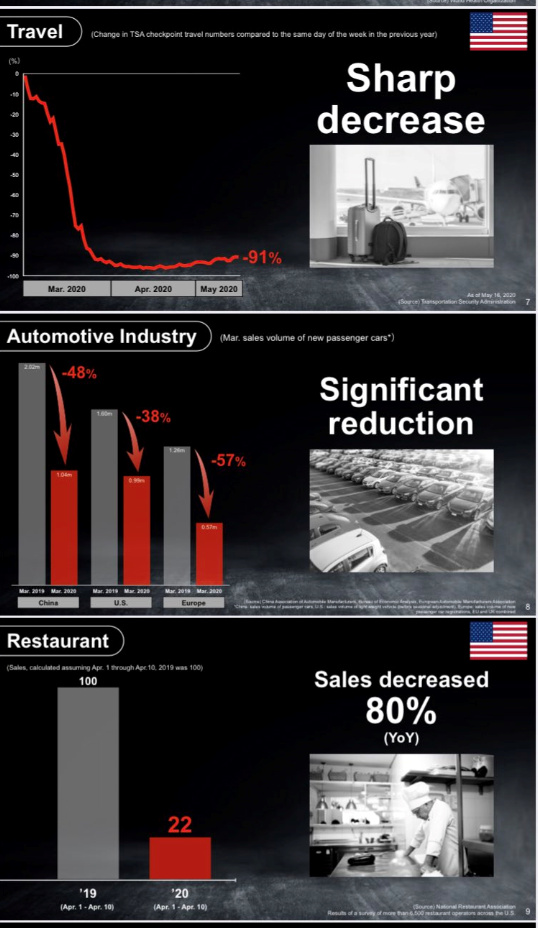

What are the chances your company will survive Covid-19?

Podcast with Aswath Damodaran by Forbes India

He is shedding light on valuing companies during the pandemic and what this means for markets like India. This should be interesting to folks who think deeply about valuation.

3 Likes

2 Likes

1 Like

great videos on investing

4 Likes

How To Value Businesses During COVID? | Aswath Damodaran

1 Like

In present age of social media and info overload - this is good article to read -

https://medium.com/accelerated-intelligence/while-everyone-is-distracted-by-social-media-successful-people-double-down-on-a-totally-underrated-5a86701e9a27

2 Likes

A “must read” memo from Howard Marks of Oaktree Capital.

8 Likes

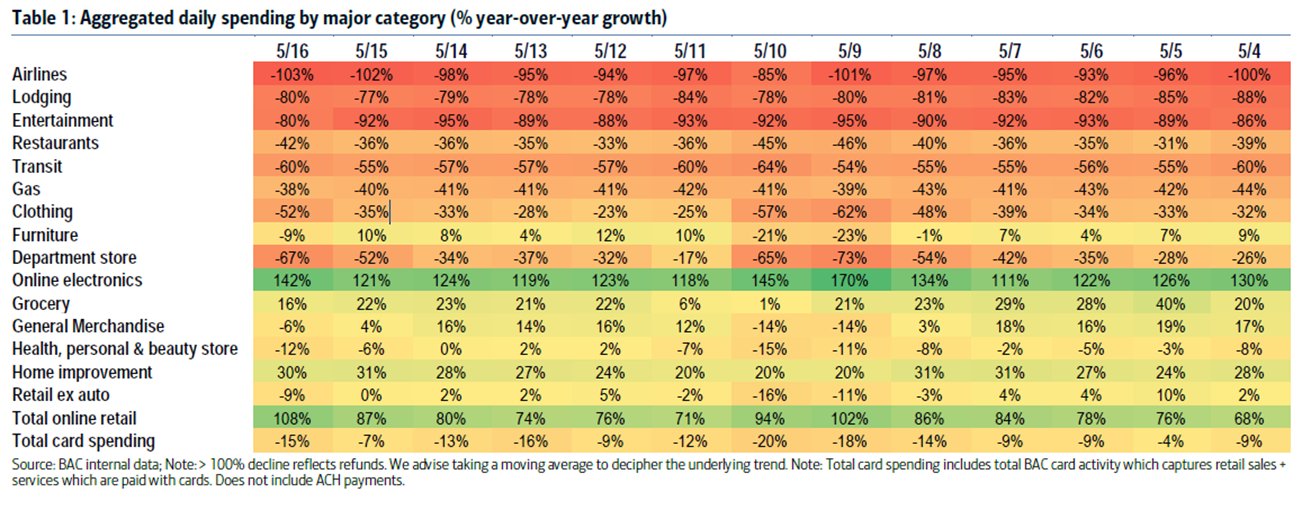

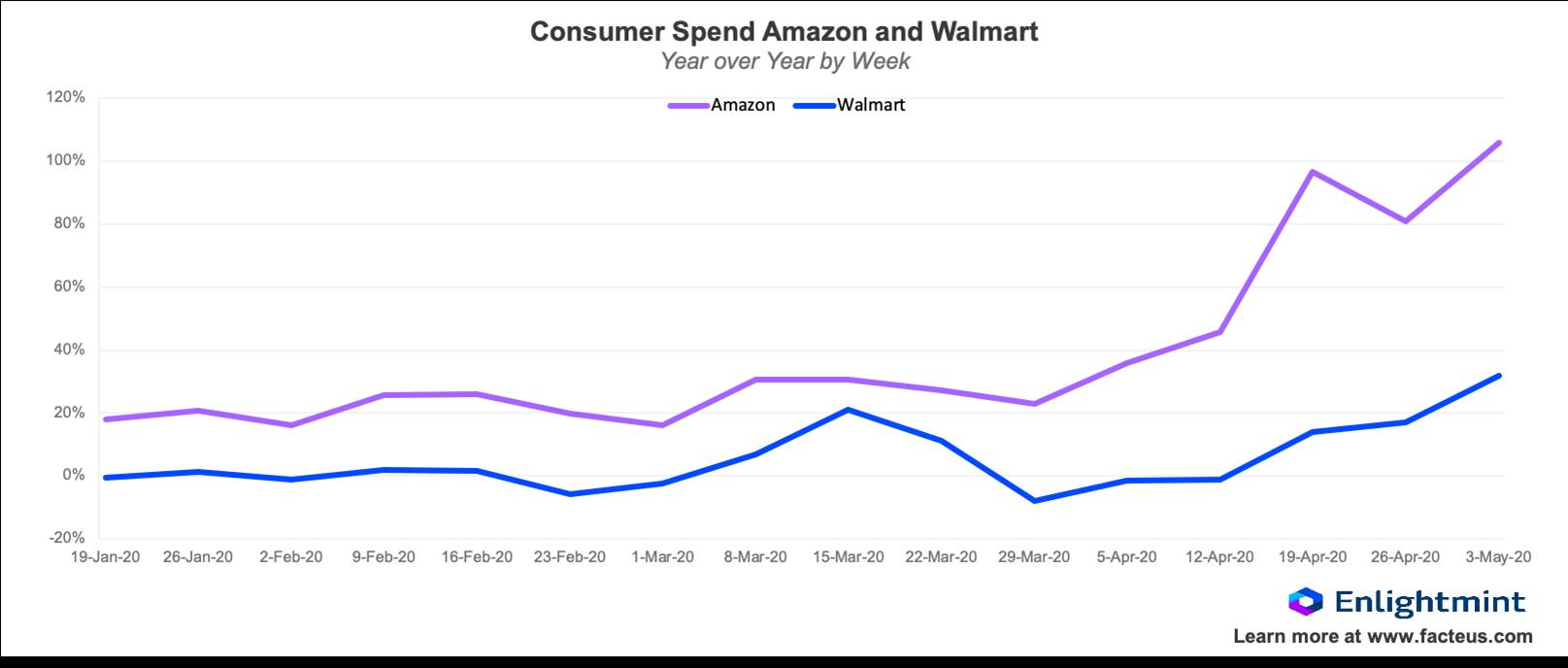

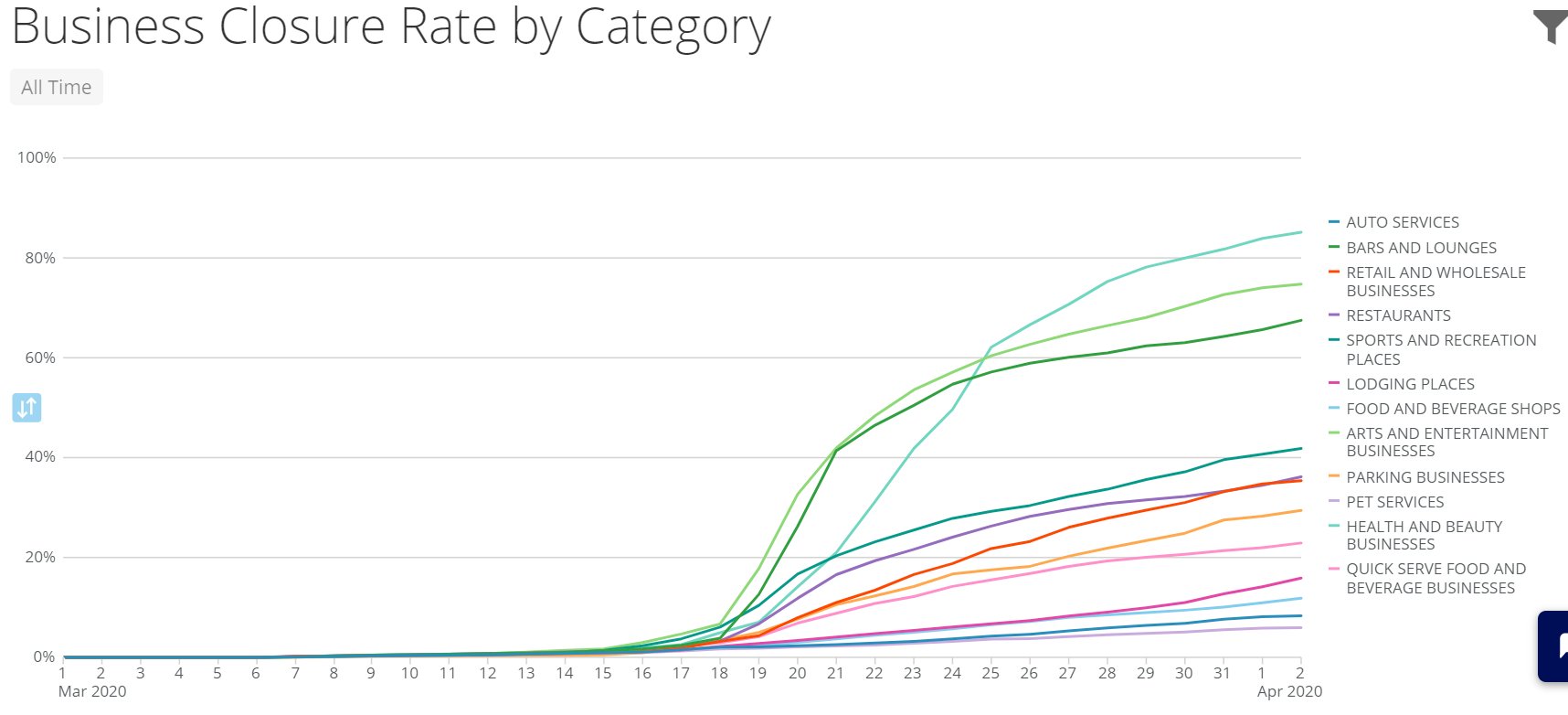

A great repository of data on various aspects of Covid:

1 Like

This is such a nice interview about Indian market cycles. I have tried to summarize my key highlights below:

- The last decade belonged to leveraged consumers which is probably why retail loan financiers did so well (Bajaj finance, Capital First) along with consumer oriented stocks (durables, FMCG, etc.).

- This is similar to what happened in 2000-2010s which belonged to the leveraged corporates (aka power, real estate, industrials) and corporate facing financials (ICICI, Axis, SBI). At that time, valuations went haywire for economy facing companies (real-estate, power, industrials, etc.).

When we will be looking back at this period after a decade, will we also compare the consumer valuations of 2010s with industrial valuations of 2000s? This also explains so much euphoria behind anything related to consumers (video 1, video 2 from PPFAS).

High compounding of returns happen when future (not past) growth rates are high and it is accompanied by a re-rating. We have to search for the next potential bubble (which is very hard to predict), and generally companies which led the last bubble do not lead the next one (eg: ACC in 1992, Infy in 2000, L&T in 2008, Sun Pharma in 2014, Bajaj finance in 2020). All these companies reached their all-time highs again (Sun still has to do!) but much later.

7 Likes