Shared by Mr Samir Arora on twitter

7 Likes

After watching this, I feel like liquidating all my Maruti Suzuki Shares and load up further on FMCG stocks.

Disruption today, 5 or 10 or 15 yrs down the line…that’s immaterial. What is material though is - Its time to think. For sure.

Thanks for posting the video @ad9

3 Likes

Auto companies are sitting ducks anyways. But next level of disruption will also happen to all energy companies including oil and electric utilities as solar PV costs drop.

Market is already discounting some these disruptions and a lot of investors are debating that valuation gap between quality(financials and FMCG) and old economy stocks is unsustainable. But if one factors in these disruptions valuation gaps start making lot of sense.

2 Likes

Here is an article from 1994 from the Forbes Magazine archives. It describes the bond market crash that happened in 1994, when the US FED raised short term interest rates by approx 2% (200 bps).

What happened?

- There was about 2.5% spread between long and short term bonds. Short term yields at about 3.5% and 10 year bond yield at about 6.2%

- Financial institutions and speculators took on leverage to take advantage of this spread

- i.e. they borrowed short and invested in long term bonds. Leverage amplified their gains.

- They made massive profits as long as the short term rates stayed low

- The US economy growth rate gave a positive surprise and there was an anticipation of inflation by the US Fed.

- Hence they decided to raise short term rates. The spread lowered.

- As a result levered long term bond holders began selling their holdings

- This lead to the drop in long term bond prices and other bond holders also had to liquidate their holdings or put up additional cash (margin calls)

- Many firms and traders suffered massive losses.

- Kidder Peabody shut shop.

- Bear Stearns and Lehman Brothers suffered massive losses.

- Askin Asset Management (a hedge fund) collapsed.

4 Likes

If u hear basant’s new investment philosophy he has done a u turn on his old thesis… Don’t u think…

He now say big is beautiful… Faang stocks hv proved it!! ![]()

Old interview of Great Peter L. Bernstein

1 Like

https://www.akrecapital.com/the-art-of-not-selling/

Taking a step back, our investment philosophy involves concentrating our capital in a small number of what we believe to be growing and competitively advantaged businesses. These kinds of businesses are rare and are only periodically available for purchase at attractive valuations. With that in mind, we do our best to hold on for the long term, so that our capital may compound as the businesses grow.

Holding on means resisting the temptations to sell — and there are many. We tune out politics and macroeconomics. To the surprise of many, neither valuation nor price targets play a role in our sell

decisions.

To be clear, there may be times when we believe it is appropriate to sell. In these instances, it is typically because of an adverse change in the business itself.

2 Likes

Great learning and good points to follow if one is obsessed with Quant one must watch

https://www.cfainstitute.org/en/research/multimedia/2018/algorithmic-trading-introduction-nuts-bolts

also fundamentals of value creation are good articles to read by Rishi Gosalia

https://www.gurufocus.com/news/153695/fundamentals-of-value-creation

https://www.gurufocus.com/news/156159/fundamentals-of-value-creation--part-ii

1 Like

Yeah…a lot of rational and intelligent people underestimate this.

In my personal experience, this one trait is the most imp one for long term success in the Mkts. Optimism trumps all other traits.

However, optimism without knowledge can be Fatal…obviously!!!

1 Like

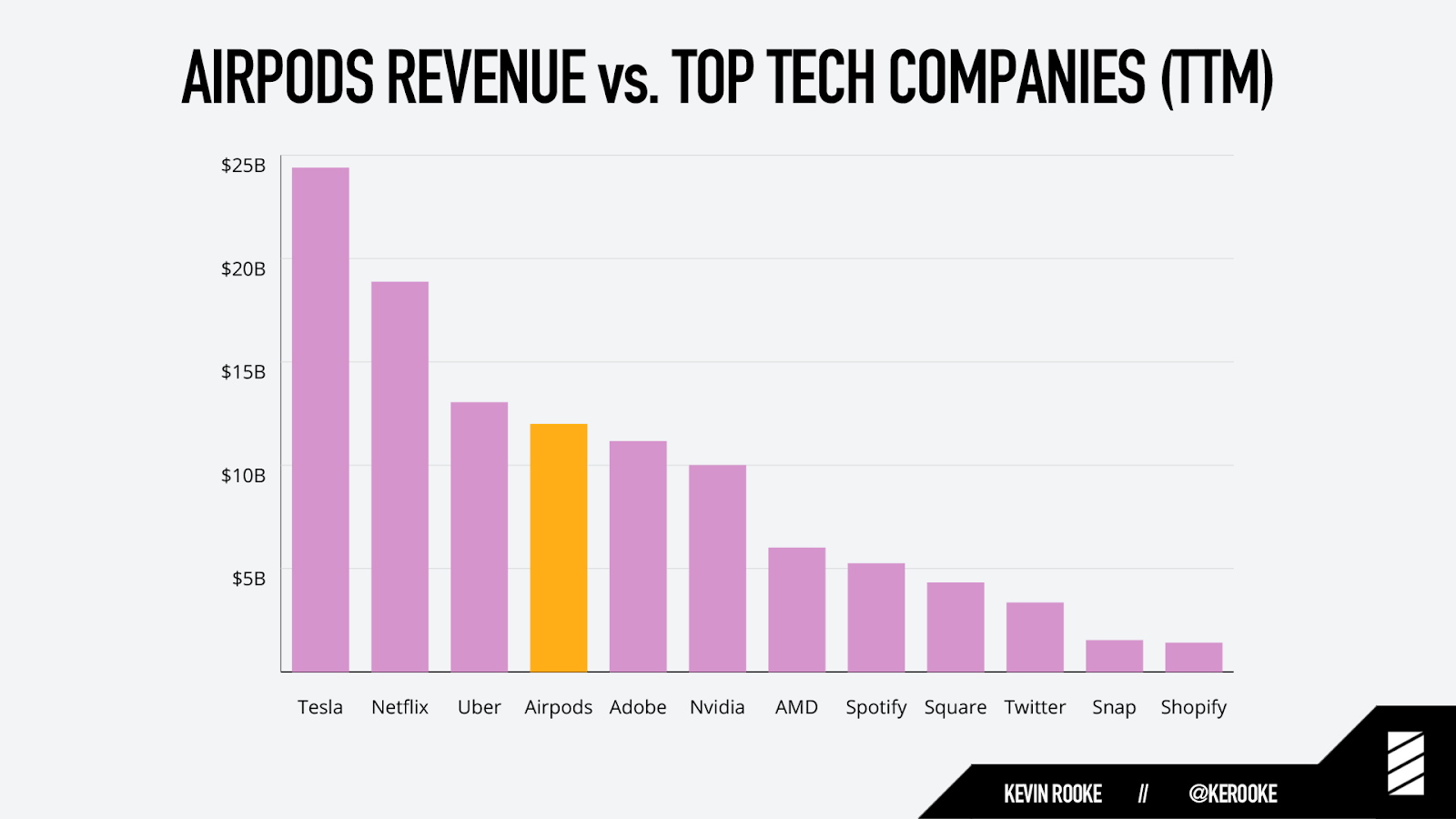

The estimated revenue from airpods (actual numbers are not released) is more than the revenue of most tech companies.

https://www.kevinrooke.com/post/apple-airpods-iphone-accessory-or-the-next-big-thing

1 Like

What better article to read than 2002 news article on business today.

Some interesting views

- HDFc bank is expensive and ICICI/SBI better bets

2.GOI looking to divest oil companies : joy:

3.Contrarians were right then also (Though FMCG was contra bet then)

eg:Marico is attractive due to low valuations. It trades at seven-to-eight times earnings perhaps because of its dependence on a single brand (Parachute) and the commodity nature of its portfolio.

http://archives.digitaltoday.in/businesstoday/20020414/cover2.html

8 Likes

Interesting…

So HDFC traded at 25 PE in 2002 also. No not very expensive currently at 24-25 forward PE, considering the fact that it have proven consistency for two decades, PSU banks are in shambles giving up market share, HDFC bank earns a lot more through fees now compared to 2002.

Marico from 7 PE to 40 PE. Despite all +ves that is some serious re-rating.

2 Likes

It’s the longevity that is important to the core. An apt article.

2 Likes

He is saying if the Stage 1 growth period is long enough, high P/E is justified. But people underestimate the Stage 1 growth period and so (wrongly) think stocks are expensive.

Of course, we know that if we use a high growth rate for a long period with a low discount rate, excel sheet will give us an astronomical value. But this logic is flawed.

Using the correct discounting factor is at the heart of DCF methodology. The discount rate is a result of several variables, the most important of which is the degree of certainty of those cash flows. Higher the certainty, lower the rate and lower the certainty, higher the rate. Even for an HDFC Bank or an Asian Paints , the 15th year cash flow has less certainty than the 3rd year cash flow, simply due to the intervention of time. I cannot use the same rate to discount a 20-year Stage 1 period that I use for a 3-year Stage 1 period and compare the two. Even risk free assets like G-Secs carry higher coupons for longer tenures than for shorter tenures.

6 Likes

What really is a bet? How does one make decisions under uncertainty and with imperfect information?

In his latest memo, Howard Marks weaves his own life story to discuss the process of thinking in bets, parses the world of gambling, and draws parallels between investing and games of chance.

4 Likes

In fact, the lack of predictability means that what remains is truly valuable. Which is, to judge quality businesses on the basis of long track record, and hold large and diversified portfolios so that the negative effects of company and sector-specific events can be evened out.

https://www.valueresearchonline.com/stories/47706/inputs-and-outputs

The transcripts of some of the famous speeches and great talks are organized here by James Clear. This is work in progress and the list is continuously being updated. Just to highlight, talks by Charlie Munger, Steve Jobs, Richard Feynman, Jeff Bezos are part of this compilation and they are really great. I just copy paste the content to MS word and then email the document to my Kindle id and read it on Kindle quite often.

15 Likes