A fantastic talk by Prof Bakshi

A gem of presentation from kuntalshah.

Amazing presentation but I was not convinced by numbers chosen to explain Ergodicity. It is +50% and -40%. This will always lead to wipe out even if there are equal proobablity of both happening.

If something is down 40%, it needs to up by 66.67%(vs 50% in example) to get back to the same level.

Or if something is up 50%, it needs to go down by just 33.33%(vs 40% in example) to fall back to same level.

https://www.newconstructs.com/education-close-the-loopholes-how-our-dcf-works/

Interesting read on The Power of the Implied Growth Appreciation Period (GAP) or Reverse DCF

Hi

A recent interview of Peter Lynch.

https://www.fidelity.com/viewpoints/investing-ideas/peter-lynch-investment-strategy-q-a

Rgds

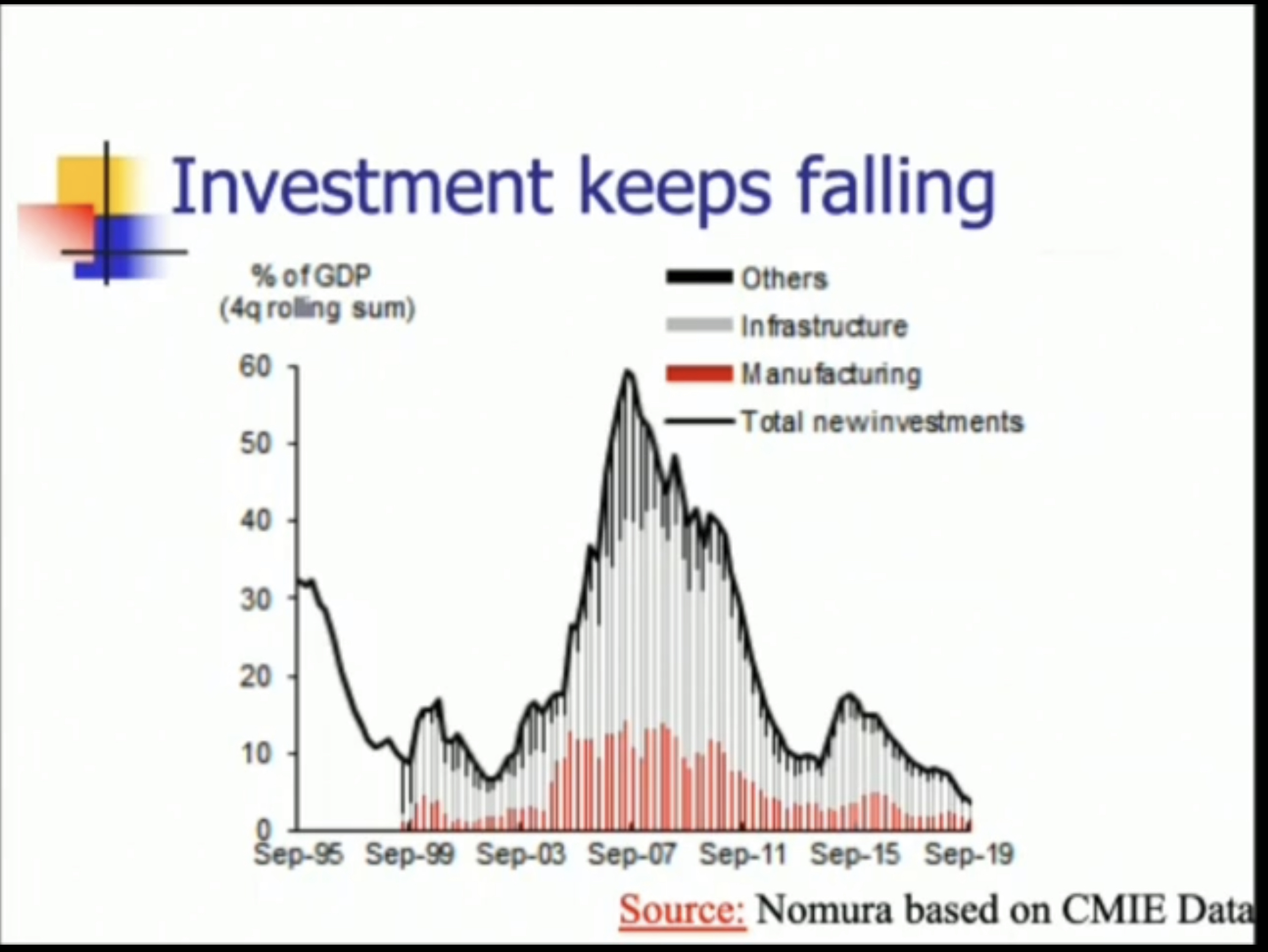

Nice video from Mr Rajan and counter argument from Mr Subramanian.

One graph I find is interesting from Mr Rajan talk is about investment.

In 2005-2010 big players like Anil Ambani/Essel (and real estate player across the board) were expanding aggressively. I wonder who has the balance sheet and demand to take up hugh investment again.

Maybe I am Ian Cassel fan or maybe I invest in micro and small caps, or maybe something in his writings resonates, but I keep on sharing him.

An interesting article on Reliance Retail being the next Reliance Jio - RIL’s e-commerce push: Will Reliance Retail be the next Jio?

George soro’s lectures Trascripts

Regards

The article Akash Prakash referencing in this article is attached below.

THE-BIG-CALL-BUBBLE-IN-QUALITY.pdf (3.1 MB)

Excellent read, thanks for sharing. What I have observed is, from time to time, there are new darlings of Mr. Market. And the general tendency is to buy those darling stocks at whatever price by ignoring valuations.

For much of this decade, these darlings were companies from fmcg and pharma sector. One simple search on google about pharma companies with timeframe from 2010 to 2016 will tell you how much market loved them. Many analysts touted how pharma companies deserve high valuations and justified by whatever excuses. Same is the case for fmcg companies now, market loves to justify their astronomical valuations. But if one looks at most of these same fmcg companies, they traded in the pe of low 20s for much of 2000-2009 period. Even in the 90s when their pe was high, they had earnings growth to back that up, so taking growth into account they still were trading reasonably unlike now. If one is buying such stocks at present valuations especially for long term say 10-15 years, what is the gurantee that market will not rerate these stocks, once again, in these coming years ?

The combined profit of HUL and Nestle is about Rs 7,600 crore and their current market cap is about Rs 6 lakh crore. For that money, you are getting the entire steel, metal and cement sectors, whose combined profit is Rs 70,000 crore plus,

My thoughts on the evolution of an investor over time and why it is important to keep learning and evolving.

World has gone mad and the system is broken : Ray Dalio

What Howard Marks has to say on buying high quality stocks at any valuation hoping that earnings would take care of the valuation.

What an object lesson! What an epiphany! Buy the stocks of the best companies in

America at prices that assume nothing can go wrong? Or buy the bonds of unloved

companies at prices that overstate the risk of default, and from which the surprises are

likely to be on the upside? Having seen fortunes lost investing in the best, it seemed much

smarter to buy the worst at too-low prices.

“… the biggest beneficiaries of the cut in corporate tax rates are companies with a combination of high ROCE + high reinvestment rate + high tax rate. Firms which will NOT benefit much from the tax rate cut are those which either do not have avenues for capital reinvestment, or which have low pricing power (and hence will have to sacrifice the gains from the tax cut), or which have low ROCE, or those that are not cash generative…” ~ Saurabh Mukherjea (Marcellus)

Interesting data -

- 80% of the returns from the Sensex are generated in the two years following General Elections

- 41% and 27% CAGR are the average one year and two year post-election returns of the Sensex; in contrast, the Sensex’s 1984-2019 return is 15% CAGR

- No correlation between GDP growth & Sensex returns

Source: https://www.youtube.com/watch?v=JVevwv9tGy0&feature=youtu.be

Good Checklists

I know that everyone in this room is exceedingly intelligent and youíve all worked hard

to get where you are. You are the brightest of the bright. And yet, thereís one thing you

should remember if you remember nothing else from my talk: You have almost no

chance of being a great investor. You have a really, really low probability, like 2% or

less. And Iím adjusting for the fact that you all have high IQs and are hard workers and

will have an MBA from one of the top business schools in the country soon. If this

audience was just a random sample of the population at large, the likelihood of anyone

here becoming a great investor later on would be even less, like 1/50th of 1% or

something. You all have a lot of advantages over Joe Investor, and yet you have almost

no chance of standing out from the crowd over a long period of time.

And the reason is that it doesnít much matter what your IQ is, or how many books or

magazines or newspapers you have read, or how much experience you have, or will have

later in your career. These are things that many people have and yet almost none of them

end up compounding at 20% or 25% over their careers.

Trait #1 is the ability to buy stocks while others are panicking and sell stocks while others

are euphoric. Everyone thinks they can do this, but then when October 19, 1987 comes

around and the market is crashing all around you, almost no one has the stomach to buy.

When the year 1999 comes around and the market is going up almost every day, you

canít bring yourself to sell because if you do, you may fall behind your peers. The vast

majority of the people who manage money have MBAs and high IQs and have read a lot

of books. By late 1999, all these people knew with great certainty that stocks were

overvalued, and yet they couldnít bring themselves to take money off the table because of

the ìinstitutional imperative,î as Buffett calls it.