Is Gravita entering into unrelated business of manufacturing commodities . Their primary business in metal recycling but this company is into manufacturing copper products. Even though it will help the company in copper recycling what will the % ?

1 Like

Copper is one of the promising commodities, and even Adani has entered this. And after the acquisition, 1000 Cr in revenue comes on the books. See the Margin level on the business

6 Likes

I was trying to understand the financials of Gravita India, can anyone shed some light on why CFO / EBIDTA for them for the past 10 years is a meagre 24%?

1 Like

I think in coming days, all recycle companies going to face tough time as the availability of cheap scrape is limited and logistics cost are sky rocketing due to middle east war. Keep watching this sector for correction and good entry price.

- Shipping Disruptions: With the Red Sea corridor effectively restricted and vessels rerouting via the Cape of Good Hope, Gravita is likely seeing an increase in transit times by 15–20 days for scrap arriving from Europe and the Americas. This affects the “Mundra” facility significantly, as it serves as a primary hub for imported scrap.

- Logistics Costs: Freight rates have spiked due to the maritime blockade. While Gravita often passes these costs to customers, the suddenness of the March 2026 escalation may lead to temporary margin compression on existing contracts.

- Lead Stability/Weakness: Lead has hit multi-week lows (~$1,880–$1,940/T). Since lead is Gravita’s primary revenue driver, lower LME prices can reduce the absolute EBITDA per tonne, even if margins remain percentage-stable due to their back-to-back hedging strategy.

- Balance sheet impact:

-

Inventories: Higher in value; risk of write‑downs if prices correct sharply later.

Receivables: Larger absolute numbers; higher credit risk if customers are stressed.

-

5 Likes

I don’t think the red sea corridor is restricted, Ships are passing thru.

IMV looking at price action there is something wrong that we will get to know after Q4

1-The scrap prob is still not resolved

2-Still awaiting for approval of new plant which is ready to run

3-Margin may take hit due to ongoing war

Above 3 concerns are their from my side, the way stock is behaving technically there is something we dont know , but long term wise its at great valuations

4 Likes

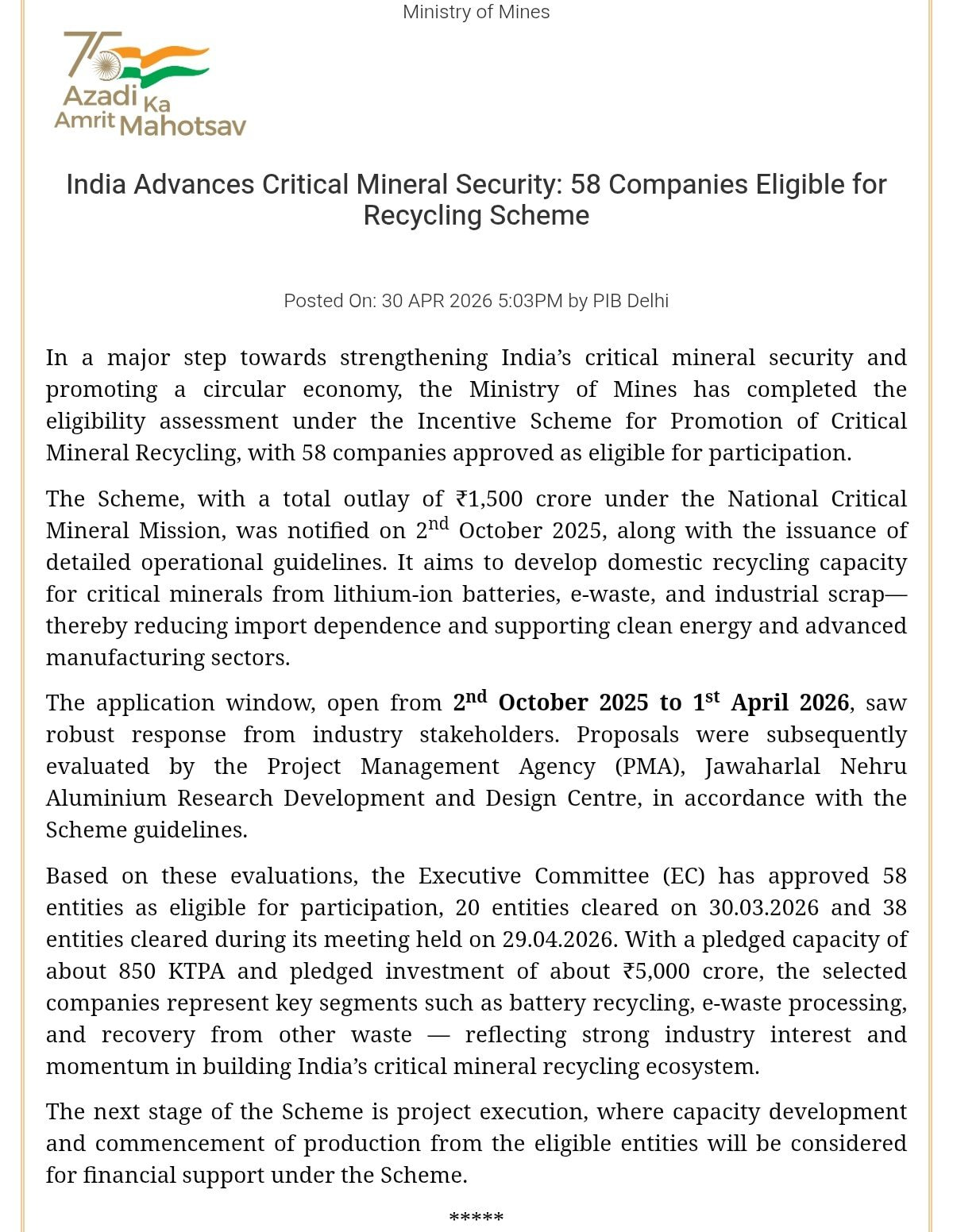

Name of 58 companies announced by the govt or it will be announce on later date?

Recently, Gravita did a capex on lithium ion battery recyling. Though it is a pilot project and may not yield revenue for next 3-4 years as per management’s commentary still that India-EU FTA in recent time unlocks growth opportunity for gravita in battery recycling sector

1 Like

In con call - honest management accepted and communicated to investor that Q1 and Q2 of FY26-27 will not be good as they are facing logistics issue due to west asia war. Scrap prices gone high and product price is not going up due to logistics cost. Recent expansion will have negative impact on bottom line due to depreciation and reverse operating leverage issue. Hoping, good opportunity will be available around July 2026 to buy at reasonable valuation

6 Likes

Q4 FY 26 concall summary

RMIL Acquisition (Rs. 560 cr, 99.44% stake)

• 31,200 MT copper capacity in Gujarat; 50% utilised today, targeting 60-65% by FY27

• End-markets: defence, coinage, ammunition, electrical; 40% exports

• Copper is now formally Engine 2 — not just optionality

Copper Recycling Plant

• 29,400 MTPA Phase 1; Rs. 160 cr capex; live in 12 months

• Primary offtake goes to RMIL as captive feedstock; surplus sold externally

The Core Economics

• RMIL EBITDA/MT today: Rs. 45,000 (buying scrap externally)

• Post captive supply: Rs. 65,000-70,000/MT — ~45% uplift

• Structural, not cyclical. 20%+ ROCE consolidated guided

Li-Ion Battery Recycling

• Mundra 6,000 MT pilot = black mass only (Phase 1)

• Phase 2 refining/extraction: yet to come

• Zero revenue baked into FY29 guidance — anything here is pure upside.

Lead, Rubber, Steel

• Lead capacity revised up: 700k to 800k MT by FY29

• Rubber 30k MT live in H1 FY27 at Rs. 7-8/kg EBITDA

• Steel: 2-3 years away, not a near-term factor

Volume Guidance FY27

• Overall: 20-25% growth + some catch-up for FY26 misses

• Copper: 40-50% growth — the standout

EPR

• FY26 lead miss (~15% vs guidance) driven by EPR credit fraud + 18% GST arbitrage favouring unorganised players + weak global lead prices

• RCM on battery scrap pending at next GST Council; NITI Aayog already on record

• RCM passage =kills the grey market cost advantage; major volume formalisation event for Gravita.

Capex

• Revised from Rs. 1,200 cr to Rs. 1,700 cr through FY29

• Rs. 700 cr earmarked for copper; Rs. 600/700/400 cr phased over FY27/28/29

• Fully funded via internal accruals; debt only for working capital

Within copper capex: Rs. 200-300 cr for VAP (margin lift) + Rs. 400-500 cr for base recycling (volume/revenue lift)

Working Capital and Hedging

• WC days: 90 in FY26 (inventory buildup), 85-90 in FY27

• Peak WC debt could hit Rs. 800-900 cr vs Rs. 118 cr net debt today

• Lead, copper, plastic hedged on MCX; aluminium pending approval — volumes capped till then

Debt

• Gross debt Rs. 736 cr ; net debt ~Rs. 100 cr

• March spike due to RMIL closing, not a recurring burden

• FY27 interest: Rs. 4-5 cr/quarter only; Rs. 77 cr other income from QIP cash in liquid funds offsets significantly

(Used AI to summarise the content)

7 Likes

I personally view the EPR implementation, BWR norms, EV shift, BESS implementation as catalysts to the growth trajectory of the company. RMIL and with it copper recycling and value added products would further give it wings.

Some may judge Gravita to be late in Li Battery recycling setup, but the management has adequately guided that until there is an economy of scale, it will not be profitable. So their trial setup at a small scale is a good step to proof test the process.

The challenges due to the SLOCs affected by the conflict in West Asia, continue to persist and may slow the growth, however, the formalisation of waste collection in India itself is a silver lining.

Another plausible scenario that may work in favour is the elevated metal prices, that is norm in post war periods, due to the reconstruction effort and infra demand. Copper demand is already rising and is likely to revise price upwards.

Near term price correction in Gravita may offer good opportunity to enter with a long term horizon.

8 Likes

Gravita has acquired 99.44%* stake in Rashtriya Metal Industries

Limited (RMIL) for Rs. 561.84 crore, a dedicated facility in Sarigram, Gujarat with a

capacity of 31,200 MTPA. viz a viz

Pondy oxide Installed Capacity - 36,000 MTPA - LME Grade A Copper Cathode to be implemented in two phases of 18,000 MTPA each.

� Technology -Integrated Pyro-refining and Electro-refining facility

� Location - Thervoykandigai, Tamil Nadu, India

� Project Cost - Approximately Rs. 200 Crores

Disparity in value of RMIL and new proposed project of pondy oxide.

561 cr for capacity 31200 mtpa vs 200 cr for 36000 mtpa.

4 Likes

I highlighted this few days ago.

5 Likes

Good notes courtesy SOIC on Gravita management meeting-Gravita - Management meet notes - by SOIC Finance

2 Likes