Any reason for sudden correction?

It seems some of the guys who were reclassified as non-promoters (Exchange filing on 4th October) are dumping stock on the market. Higher trading and delivery volume on BSE in last few days after date of filing is something on which my proposition is based. It could take another week or so for their shares if entirely sold to be absorbed in the market.

1 Like

This includes a write up on Growel’s 101: https://www.indiaretailing.com/2019/12/24/shopping-centre/the-year-that-was-customer-centricity-key-to-shopping-mall-success/

1 Like

Retailers are invoking force majeure which will be an additional hit. But there has been constant promoter buying which provides some comfort.

1 Like

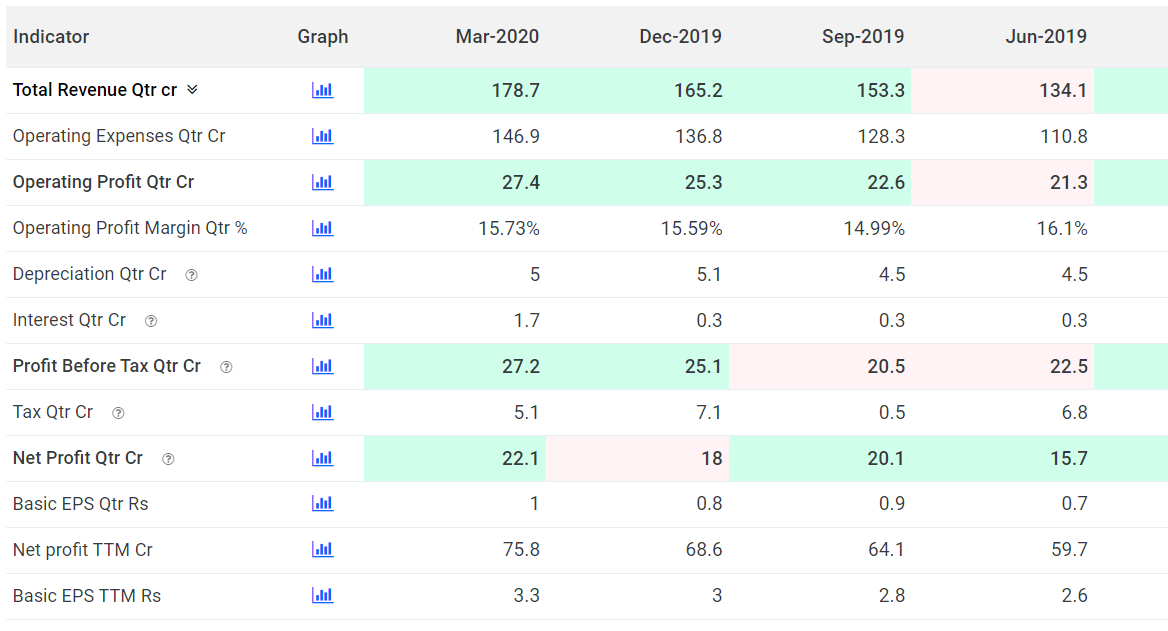

Good set of numbers for Q4 2020

Its chemical buis is really growing well

2021 may have very less revenue from mall buis.

But overall very good buis for long term

Disc…invested since 2 years

Volume is way too less. For a company thats having such good reviews,the main lacunae is such low volumes. Risk of having illiquid stock is there. Wonder why?

It’s Q1 that one has to wait for and the go-forward outlook, particularly for their chemical business. I think Grauer will report a loss in Q1, and mall biz will be washout for FY21 anyway.

I think they have been paid partial rent/reduced rent if not full or may be they have accepted a delay. You can’t understand it by profit and loss statement.

1 Like

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5f6712ee-62b2-4947-b082-06721216adf6.pdf.

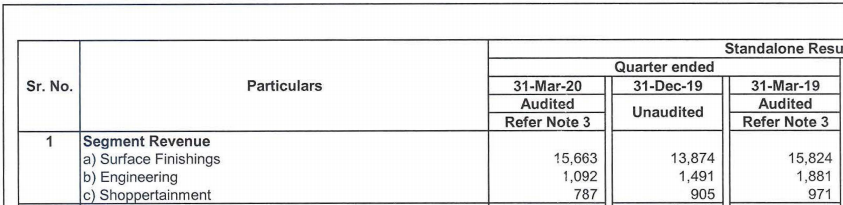

Surface finishing business has shown good profit. Over all result is good inspite of slown down in other two segments viz Engg & Rent from real esate.

3 Likes

AGM Recording of FY 20

3 Likes

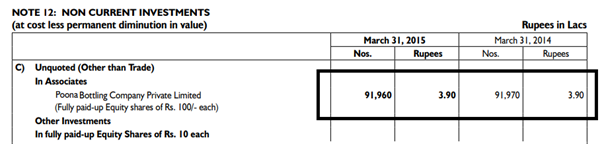

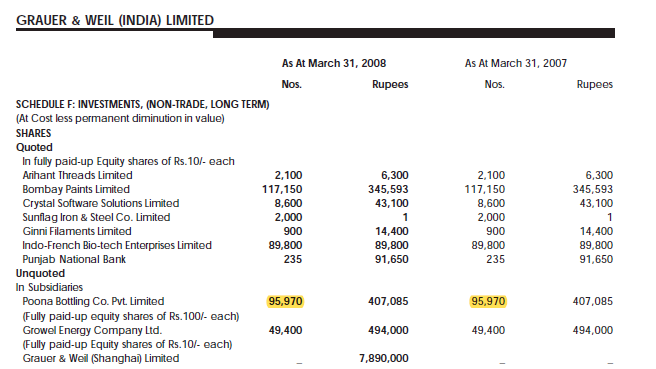

In the Q & A session at this AGM, someone asked a question on Poona Bottling Company (PBCL) but the management did not reply. From the latest Annual Report, I find that Grauer & Weil (G&W) has sold its 91,960 shares of PBCL and exited the company totally.

Though the AR does not clearly say so, it appears from Other Income and Cash Flow Statement that the sale has been done at PBCL’s Face Value of Rs.100 per share, fetching the company Rs.92 lacs and an accounting profit of Rs.88 lacs. But how much is PBCL really worth?

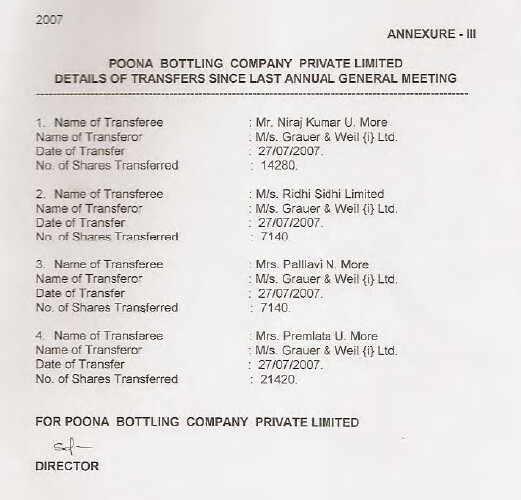

Back in the early 2000s, G&W held a 77.22% stake in PBCL. At that time, PBCL was a profit making company, had no debt and owned a large piece of land near Pune. The company planned to develop the land into an I.T. Park. But in FY2007, G&W sold 49,980 shares of PBCL @ Rs.83.40 per share, reducing its stake to 50.78% (in favor of whom is not known), valuing PBCL at Rs.1.50 crore.

In Oct-Dec 2009, PBCL acquired an 18.07% stake in G&W. And so, over the years as market cap of G&W has increased, PBCL has become more and more valuable. But strangely, as PBCL’s value has increased, G&W has quietly reduced its stake in the company, often without adequate compensation (or at least disclosures).

In FY2012, G&W sold 4,000 shares of PBCL “at market value”. Though G&W does not reveal the price at which the shares were sold, back-of-the-envelop calculations suggest the shares were sold for around Rs.22 lacs, valuing PBCL at Rs.10.40 crore. More importantly, the effect of this sale was that PBCL ceased to be a subsidiary of G&W with its stake coming down from 50.78% to 48.66% and became an Associate Company.

In FY2015, G&W further reduced its stake in PBCL from 48.66% to 30.89%.

However, Annual Report shows the number of shares held by G&W remained the same.

This implies PBCL made a fresh issue of shares to someone else. It is not clear to whom these shares were issued, at what price, who did the valuation and why G&W was giving up its stake without getting anything meaningful in return.

In FY2017, G&W reduced its stake in PBCL further to 18.27%, with the same modus operandi. At the 2017 AGM, I met Mr. Umesh More and enquired about what was happening with the company’s stake in PBCL and why it was being reduced. He said something about de-risking the main company which left me unconvinced. I asked him whether there was any plan to reduce the stake further to which he did not reply. A mail sent to the company at that time went unanswered.

In FY2021, G&W has exited the company completely, selling its remaining holding of 91,960 shares for just Rs.100 per share. PBCL has effectively disappeared from Grauer & Weil’s balance sheet. But it is safe to assume its value has increased substantially over the years. At the current market cap of Grauer & Weil of around Rs.1,400 crore, PBCL’s 18-odd percent stake in G&W itself is worth around Rs.250 crore. In addition, the large piece of land which the company can (or already has) commercially develop(ed) would be worth quite a lot.

Grauer & Weil’s minority shareholders seem to have missed out on their rightful gains.

Disclosure: Was a shareholder in the past but no positions currently. This is not a recommendation to buy or sell. My opinion may change if more information comes to light, please do your own analysis before taking any decision.

29 Likes

@Chandragupta

Excellent effort from your side. I was also suspecting something wrong about Ponna Bottling reduction in stake by Grauer and Weil in the company.

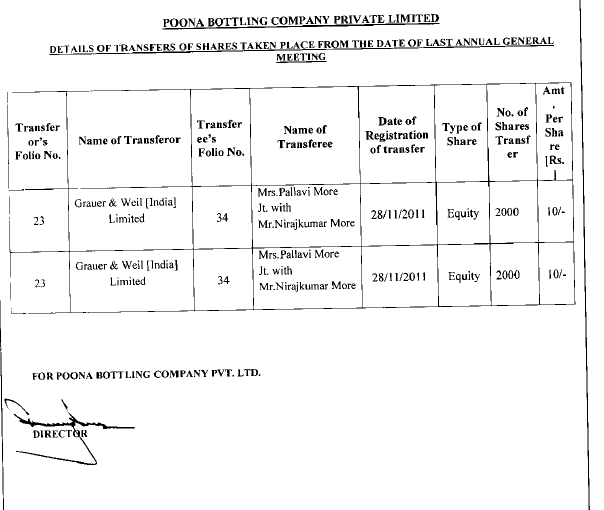

I downloaded documents from MCA website about Poona Bottling.

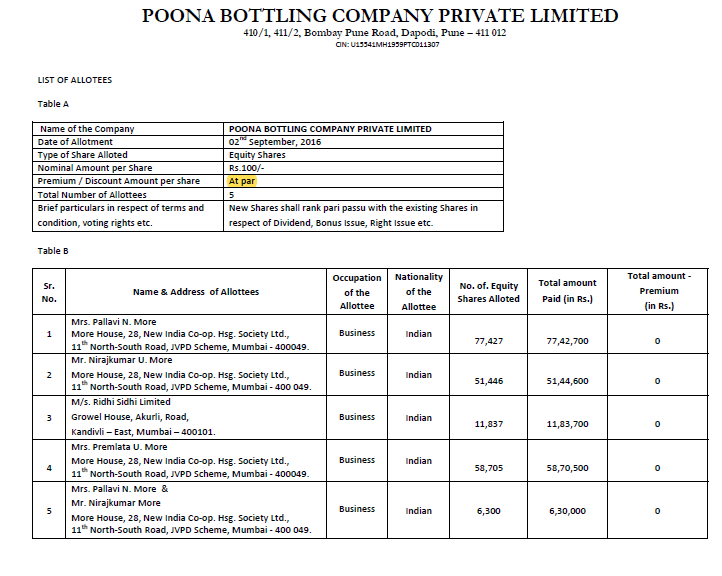

Find enclosed movement of shareholding over period, which I compiled in Excel sheet, snapshot of which I am enclosing.

Over the period, Gruaer and Weil Promoter family have systematically reduced stake (and exited in 2021) while subscribing in right issue in personal capacity. When the management of company is same, it might be worth exploring role of independent directors. When the promoter family find the investment worthwhile, why did Growel allowed its share of Rights to be lapsed which was subscribed by the promoter family of Growel?

You have already highlighted systematic decline in stake over period in your post, my attemt is to providie information of who purchased the stake divested/diluted by Growel?

As per the excel sheet, the oldest holding available is in FY2006 with around 77.2% stake of Growel (holding 145,950 shares of paid up value Rs 100 each) while More Family holding 43,050 shares (22.8% stake)

On 27 July 2007, Growel sold around 49,980 shares ( 26.4% of stake) which was purchased by More Family members.

What is surprising is Growel did not reported any change in the equity holding in Poona Bottling in FY2008 annual report and same was reported as sale during FY2007 as covered in your post.

In Nov 2011, further 4000 shares were sold to Promoter Family, (Pallavi More and Niraj More jointly purchased share from Growel) as per Poona Bottling Annual report.

Growel annual report in FY2012, does not provide any details of profit from sale this deal (the company purchased net investment as per Cashflow statement, hence we can not find out profit or loss on this sale deal). The notes to account in FY2012 annual report, does mention about sale of 4,000 shares of Poona Bottle by Growel. Also, related party details provide following information

Hence I assumed that 4000 shares were sold to Mrs Pallavi More at Rs 22 Lakhs providing per share value of Rs 550 per share. This assumption may not be correct but in view of limited information, this is best estimate of value in my opinion.

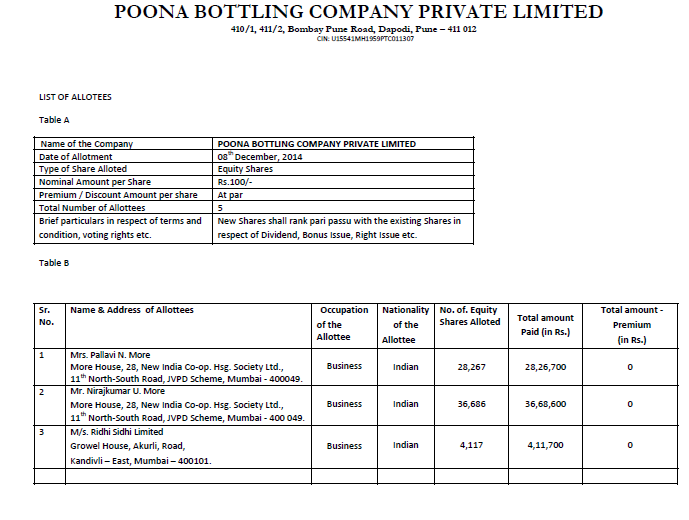

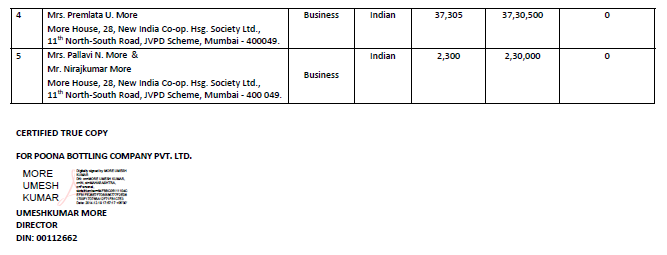

When we check MCA document for Poona Bottle, we come across allotment details of new shares at Par to following members in 2014.

In FY2015 AR of Growel, we find 10 share being sold by Growel.

Related party details provide information about sale value

If we assume that Rs 4,000 being consideration for 10 share sold by Growel in Poona Bottle, then share price would be Rs 400 per share. It may be noted, while when the promoter family is buying share at Rs 400 share form Growel, Growel management did not participate in right issue of Poona Bottle at Rs 100, par value, which was subscribed by the promoter family members.

I was not able to get Annual return of Poona Bottle for FY2016 hence does not have detail shareholding as on AGM date in 2016. However, I could download new share allotted in Rights by Poona Bottle in Feb 2016.

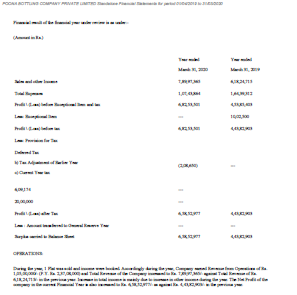

Find enclosed FY2020 annual report extract of Poona Bottle

So with given information, I am in complete agreement with you the management has systematically taken control of Poona Bottle over decades. 77% stake reduced to nil in the company which hold 18.92% stake in Grauer and Weil. While there are some assumption in my working and open to change my view in case proper explanation is provided, but with the limited information available in public domain, I sincerely feel that management of Growel (Particularly independent directors) have not taken proper care of minority shareholders interest in dealing with Poona Bottling divestment.

Disclosure: I hold very small quantity of Growel shares. I am not SEBI registered advisor. I am not recommending any investment related decision on the company. The reader shall consider his/her investment advisor and do proper due diligence before taking any investment action. This post have certain assumption which may not true. This was my effort more to understand how assets under control of the company can be systematically diverted from the company. I have not done any trade in last 30 days in the company.

19 Likes

I had attended the AGM of Grauer and Weil. The management did reply back on investor’s questions on selling of stake in Pune bottling plant (not sure if the reply was satisfactory). Key points of the AGM are given below (running notes while listening to AGM):

• Surface treatment chemicals – 1. Electronics 2. Metal finishing Metal finishing is a bigger business and electronics is a fraction of metal finishing. Decent market share in metal finishing business- AUtmotive – 40%, bathroom fittings, artificial jewellery, engineering items – 10 – 15% each. Aviation and defense yet to reach any significant level. With Make In india initiatives, might see more business. High margin business but low base. Paint product line and chemical product lines have some approvals.

• All our business – chemicals, paints, lubricants are B2B. Customers are industrial users in all the segment. Chemicals – large part of sale happens through dealers and distributions. Some supplies directly. Paints – direct sales. Lubricants – mix of direct and distributors. Engineering – direct sales.

• Most of customer segments are organized industry. Very less unorganized. Most competition comes from organized sector. Bottom end – unorganized is there but we don’t have much presence.

• Industrial product – linkage to GDP is significant. PLI scheme and growth – potential is healthy. In case of chemicals where we are market leaders – growth will tend to be as per GDP growth. In paints and lubricants, since our market share is not very large, we can grow at faster rate. Paint we have grown at 30 – 40% cagr. FY21 – growth slowed down in paint due to covid. Much larger growth in paints and oils.

• Share of business in paints and oils will also increase. ‘

• Moats in the business. All our product areas – technology – focus on technology oriented products. Technology continues to be a significant moat for us. Second advantage – market presence – dealer and distribution network. More than 50 plus offices in place. Large channel partners. Plus 200 plus technically trained contingent. 3 Strength areas have stood the company in good health. Use them as strength. Response to customer is also a strength for us. Having been in business for so many years, we have good relationship with customers.

• Cost increase – all segments have seen increases. Chemicals – cost increase happens relatively easier some lag. Lubricants and paints – difficult to pass price but happens sooner than later – absorb for some time and then pass on.

• Competition is there with MNCs and domestic company. Chemicals – only large competitors – Largest – autototech, Artech both global leaders – Paints – Akzo Nobel, Shalimar, Asian Paints, Berger. Same with lubricants – MNCs and OMCs. Strategy – we cover all the markets in chemicals, in case of paints and lubricants – follow strategy of picking niches and growing sub segment by sub segment. Selected segments where we can capitalize on strength. Chemical market share – 35%, paint business – sub segments where we are – 5 to 12 – 13%, Product lines in paints potential is 2000 crore higher than chemical business.

• Premiumization of products – cars, jewellery, bathroom products this leads to higher potential for electroplating. EV will use lesser chemicals than chemical components. But electronic components usage higher leading to higher electronic chemicals. Already working on product lines for electronic chemicals.

• Inorganic opportunities – surface finishing – very few and always on a the look out. Do have bandwidth and resources available. Nothing as of now. Drawn up ambitious mission in top 2 or global positional – long term missions. Missions which drive our thinking and our plans.

• Regulatory changes driving need for green products – increasing regulatory change taking place – demand for environmentally compliant products. Full range in chemicals. Cant say same for oils and paints.

• Engineering business growth in last year? Doing well this year as well. Also optimistic about future as well. Cyclical business. As capital goods demand comes up, business is good.

• Royalty payment? Linked to engineering business. Automation software from European collaborator. As business increase, it will increase

• Export growth? Export will continue to grow in near future. Introduction of REACH in Europe. Nos of suppliers are smaller. Only those are compliant with REACH are able to supply. Second opportunity is China Plus 1 policy which most global cos are following now. Helping us grow exports. Good opportunity there.

• Capacity utilization? 6 plants right now – ranges between 25 – 75%. Main plants in Dadra – paint and chemicals are operating at 75% CU. Plant which are at lower at CU are Jammu and one more. Western demand is more and thus need to create more capacity

• New plant for paint? 30,000 KL plant. Current capacity of same size. Double our capacity. In terms of sales turover. Paint business upto 600 crore sales. Require us to add more subsegments and already made significant investment and effort on the same. The moment they come up, we will start utilizing it. 80 – 90 crore investment in new plant.

• Margin and ROCE – paint business lower than chemical business. Chemical business is niche and market leaders there. Paint on industrial segment is lower margin and ROCE. Paint – also looking at decorative segments – institutional side and niche segments. Capital employed starts coming down. Margins will also improve. Slightly below industry average with EBITDA margin of 14% and ROCE of 15%. Growth mode we need to follow different strategy there.

• Mall occupancy is 92%. Despite covid situation, haven’t seen significant exits. Rentals have come down significantly. In all cases we have converted them to revenue sharing atleast till March, 2022. Common area maintenance recovery had some gaps. Big tenants agreed to pay for that in covid period.

• Business conducting fees pertains to mall revenue. Earned from retailers.

• Mall expansion – shared in the past to expand the mall in Kandivali. Due to covid, those plans have been shelved. When things improve, we might look for that.

• Technical center – Vasai Nalasopara area – 25 crore investment.

• Supplies and logistics problem – some supplies coming from China. We have worked on this strategy. Adding more sources as a strategy.

• Surplus cash lying with us? Growing existing business – chemicals growth may be GDP linked, lubricants and paint business is growing well. Engineering growing well too. When inorganic opportunity is there, we will invest there.

• Chembur land – shut down plant. Located midst of refineries of OMCs and thermal plant of Tata. Value not that high. Selling of the land or develop the land but not much high potential.

• Insurance claim related to Vapi factory? 15 crore claim part assessment completed – 8.8 crore received and some survey under consideration. Balance quantam should get settled soon.

• Pune bottling company – investment for several decades now. Unfortunately, never paid any dividend to the company. Sold business to Coca Cola 20 years back. No business plan as of now. Received buyback plant for sale of shares. Board looked at that offer. Investment we made buyback would give value of 23 times of cost. 4 lakh investments and 90 lakh plus value. No value or dividend perspective. Some assets there but share not reflecting value. As minority shareholders, cant reinforce asset monetization. Took call to divest the stake. Investment is not our core area of business and rather focus on manufacturing business. Land under development Pune Bottling – land with Mantri Builders but deal is under scrutiny. Also, some issues with RERA.

(Note: These are running notes while attending the AGM and might contain some factual inaccuracies as well; Disclosure: Just 1 share to attending AGM)

20 Likes

There is lot of information in this thread to digest and I am slowly reading each thread date by date.

As per now the business side seems fine and technical s too.

Need some solid views to enter.

Maybe anyone tracking recently can add valuable inputs with disclaimer.

Dis: added qty for tracking position

2 Likes

Just started tracking company, actually my grandfather had shares of this company and just now it has come to me so was checking. In general story seems good and valuation also very reasonable at current levels but treatment of minority shareholder in bottling plant seems very fishy and casts doubt on management integrity I feel…

2 Likes

Huge integrity and governance issues. Selling assets to related company at throw away prices. The reply to this question in AGM was more of evasionary and unsatisfactory.

2 Likes

Thank you Praveen. You saved me a lot of effort.