Offer Price = Rs.1600 crores

The question in your mind: What do I get by paying up 1600 crores?

Well, what you get is a business generating 70 crores of free cash flow every year, needing no capital investment to grow, operates at 25% EBIT margins and generating a return on capital greater than 90% even when it is an operating at a capacity utilization of only 50%.

Before you start thinking about the valuation, let me add a mall worth Rs 1100 crores as an additional incentive.

That’s not all. The company will have cash of 130 crores by end of FY 18.

Feel the dopamine rush yet?

Well,let’s get down to business.

The company we are talking about is Grauer and Weil Limited (established 1957), dealing in surface treatment chemicals, industrial paints, engineering services and lubricants. Led by the father son duo of Umesh and Nirajkumar More, this family run company has done wonders over the last couple of decades.

Let us talk about each of the divisions:

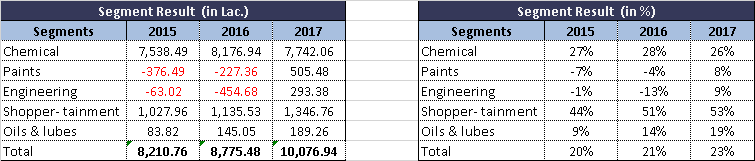

Chemicals-

Grauer is the market leader in the segment of surface treatment chemicals, intermediates and specialty electroplating chemicals and has manufacturing facilities in Dadra, Vapi & Jammu. The operations of the company are fully backward integrated making it very difficult for any new players to enter this segment. (Strong entry barriers, this is evidenced by the fact that there are only 3 players in the country in this business making it an effective oligopoly).

The revenues from this business are 300 crores (FY17), EBIT is 77 crores ( margins exceeding 25% ) and capital employed only 85 crores. (ROCE of 90%). The most important point amidst all these figures is that this is at a capacity utilization of only 45-50%,thus company could effectively double its revenues without incremental capital investment.

The market size in India is 750 crores (giving Grauer a 40% market share), which is growing at 8-10% (in line with nominal GDP). As for breakup between price and volume growth, price hikes are roughly 5-6% per annum. The domestic market is largely saturated. With regards to exports, this being a service oriented industry, the company would need to establish service centres in every country it wishes to enter.

Aviation business (read attached Business India article for further details) will be small in terms of revenues, but a high margin business since these are specialised components.

Competitors include Atotech and Artek Ltd (this company is spearheaded by Goenka family who were erstwhile partners of Grauer and Weil Ltd). Grauer is one of only four companies in the world which have the capability to provide such service (as claimed by the management).

This is thus one of the few businesses possessing high asset turnover and high margins.

The total investments in plant and machinery are only Rs 42 crores, on which company generates Rs 300 crores of revenue.

Paints-

In 2008, promoters merged Bombay Paints Limited with Grauer, which is now a 65 crore business. The company has shifted focus from conventional industrial paints to specialised paints which cater to pipeline coating, underground/underwater pipeline coatings, and so on. There is significant revenue growth potential in this segment and long term operating margins should be between 10-15% (as guided by the management).

The company has shifted operations from Chembur to Dadra (Capex of Rs 8-10 crores).

Capacity at Dadra plant is close to 8700 KL per annum and company plans to operate at 50% capacity utilisation in FY18.This business has now broken even, and management is confident of reaching 200 crores of revenue in the next 3 years. It is the first chemical and paints to receive certification from Rolls Royce and is in process of validation for Boeing for supply of specialized coatings. Rolls Royce has also approved Grow Space Aqueous cleaner.

This business has underperformed so far, behaving more as a capital guzzler as capital employed is Rs 90 crores and operating profits in FY 17 was only Rs 3 crores.

Engineering-

The engineering division offers turnkey solutions for effluent treatment. GWIL has a plant of Alandi, near of Pune that manufactures all types of equipment’s used in surface finishing and allied industries.

Revenue in FY 17 was 32 crores and operating profits were 3 crores. This is an offshoot of the chemicals business and is lumpy in nature. Aviation will be a focus area where significant growth is possible.

This business though not very big, has the advantage of being extremely capital efficient as capital employed is only 9 crores.

Lubricants-

Grauer has ventured into manufacturing specialized lubricants and oils at two plants – one in Vapi and Baroti (Himachal Pradesh) producing industrial lubricants such as rust preventives, cutting oils, hydraulic oils, heart treatment oils etc.

The current size of the business is only 10 crores, operating profits of 2 crores and capital employed of 3.5 crores. The management expects to see good growth going forward.

Real Estate-

The company owns and operates a mall going by the name of Growel’s 101 in Kandivali, Mumbai. The mall has 4,30,000 square feet( 10 acres) of retail development with 90% occupancy. Revenues this year should be in the range of 32 – 35 crores (almost entirely cash profits since unrecovered common area maintainence is only 0.5 crores-As per AS 17 disclosure, operating profits are 13-14 crores due to depreciation on mall building).

Personal visits to the mall have revealed a mall that has been built very well( though utilisation of space could have been done much better in terms of the structure of the mall)

Anchor tenats include PVR(a cinema hall is a must for a successful mall), Croma and central. Others include Mcdonalds and starbucks.

Average rental in mall is Rs 87 per sq ft (exclusive of CAM and property taxes). This includes both fixed rentals and revenue sharing contracts with most lessees.

Now coming to an interesting development- Grauer has utilised FSI of 1.16 as against the currently permitted 1.33 (ex TDR) and 1.85 (Including TDR). This is now expected to go up to 3.5-4 with the announcement of new DC rules, thereby creating an opportunity to further develop 10 lakh square feet. Yes, you read that correct.

Management is cognizant of these expected changes, and has prepared complete business plan for multi use development and has been in discussion with various developers and PE players.

They are most likely planning to develop a hotel or commercial complex where the JV partner would bring in substantial portion of cash investment required and Grauer would contribute land as equity component.

In the nearby area, a little bit of scuttle has revealed that Kalpataru has launched a project with a commanding price of 13,000-15,000 per square foot.

This means that post development, the entire developed complex would sit at 14,00,000 square feet. Do calculate market value of this at 13000 per sq ft. I leave you to draw your own conclusions regarding this

Is that all you might ask?

Well, one final thing. The company has a 99 year lease on 2 acres of prime Chembur land which currently houses only the R & D centre. This can be developed at the appropriate time ( Just as an indicator, current market value would be around 200 crores )

Valuation ( purely my estimates, subject to error)

Chemicals-1500 crores (Great business with low growth (reminds me of See’s candies).

Could be valued at a PE of 25x, considering extraordinary ROCE and sustainable earnings power)

Engineering-50 crores (Considering minimal capital requirements of the business, should trade at a high multiple of earnings. The business should enjoy robust growth over the next few years and hence would probably trade at a high multiple)

Paints This is the business where maximum capital has been deployed and is as yet unproven. Should be valued at slight premium to book value 120 crores

Lubricants Small business, has a large headway of growth in the future,low capital requirements 30 crores

Real Estate Currently rental yields are low and mall is slated to generate about 32-35 crores per annum. The annual growth will be in the range of 7-8%,at cost of capital of 13-14% for this business, valuation should be 32/(14-7)% 450 crores

Cash By FY18 end 130 crores

Total 2280 crores

Please note that this does not take into account a single rupee of upside from the new DC rules, which as discussed above will be substantial.

The promoters come across as conservative capital allocators who are looking at steadily growing the company in the right manner. They have consciously repaid most of the outstanding debt in the last few years and have avoided any value destructive acquisitions. They remain focused on value creation instead of empire building (a favourite for most Indian promoters).

Risk Factors:

Key man risk: As with a lot of promoter run companies, even Grauer faces a key man risk in the event of any misfortune befalling the More family.

Product obsolescence: I will be the first person to admit that my understanding of the business technicals is fuzzy at best and hence will leave you to take a call on this

This is my understanding of the business, could definitely be wrong. In that case, I would request all the distinguished investors to correct me. Would definitely love someone to play devil’s advocate and point out all the apparent flaws in this thesis

Disclosure-Invested