Granules India Limited Received Approval from the Health Canada for Acetaminophen Extended-Release Tablets. This is their second approval in Canada… Good for revenue diversification.

They have not mentioned size of the market, but they launched same product in the US in 2019, so this shall not be difficult for them to launch in Canada.

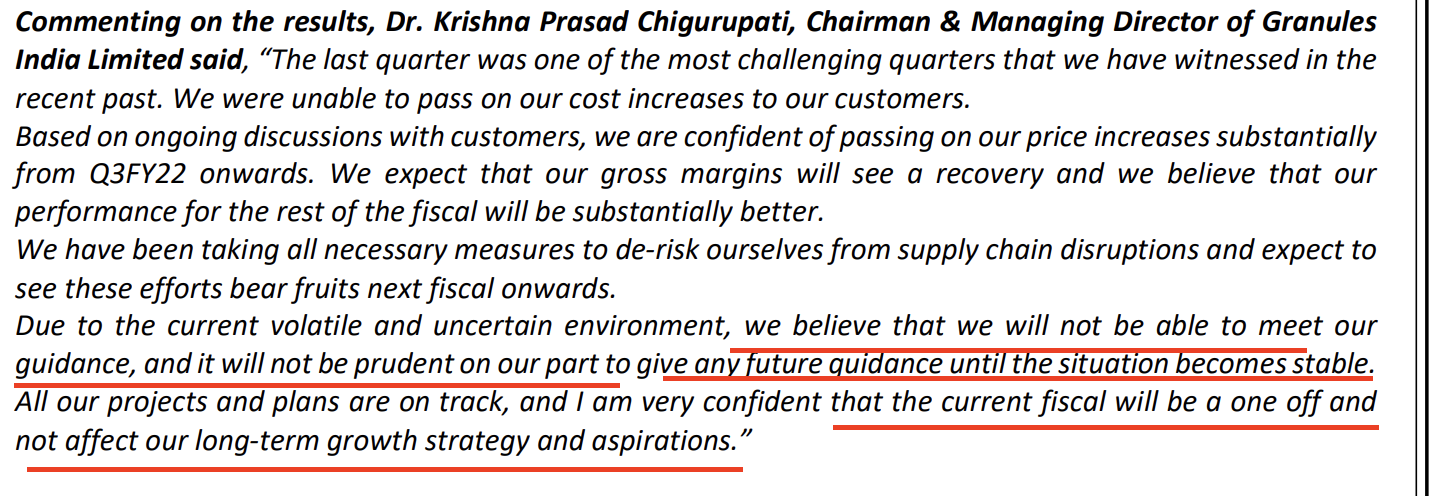

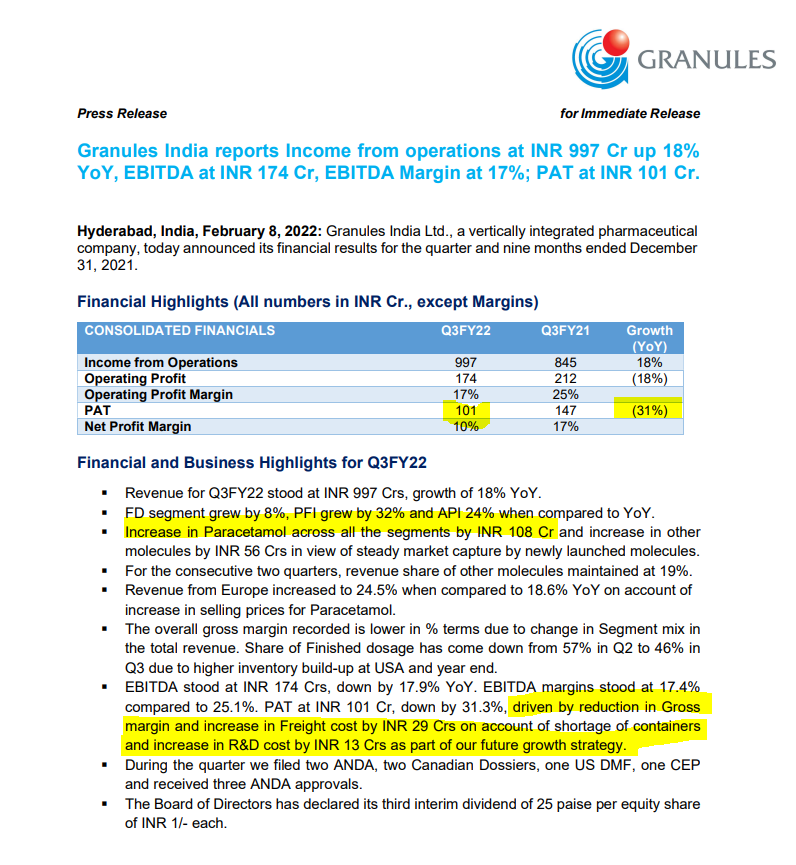

Finally management has stopped providing any guidance. Just few quarters back, they were excited and giving CAGR for next two years for 20-25% and in just two quarters the excitement has disappeared.

This article is not directly related to Granules but relevant to API industry. It cities there is increased investor interest in the segment from international investor.

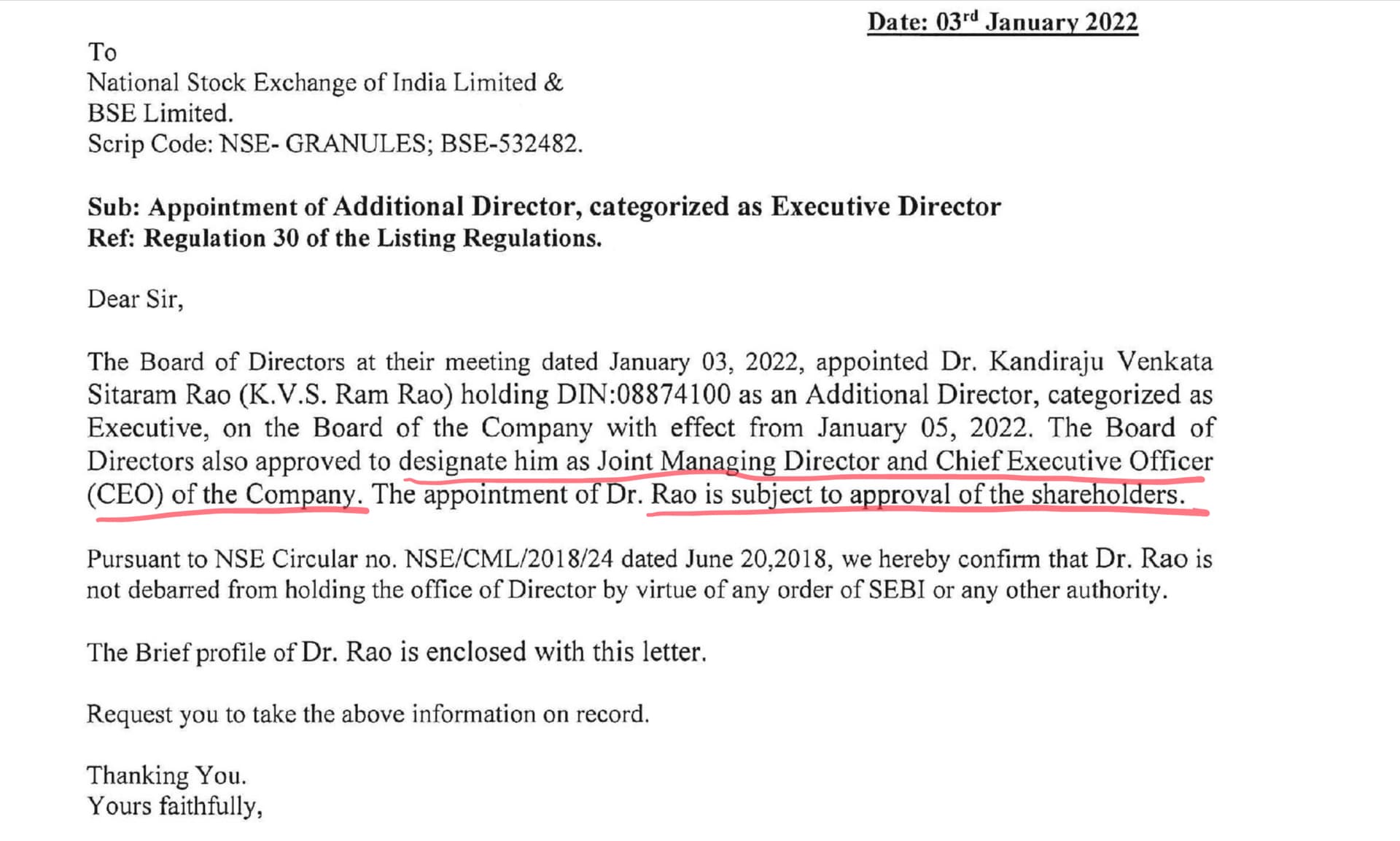

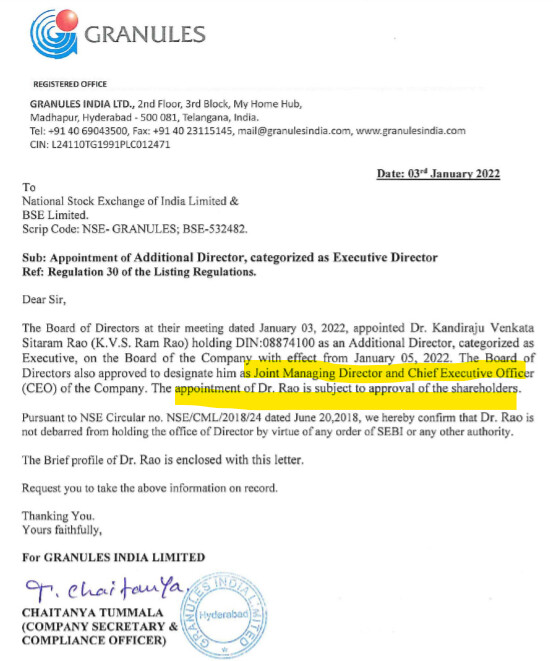

I could not get his full profile or Linkedin profile but looks like he was with PI industries and Jubiliant Life sciences.

By hiring him as a CEO, is the company going towards a professional leadership transition? The Chairman’s daughter is currently looking after US operations.

Press Release Granules Pharmaceuticals, Inc. Receives ANDA Approval for Potassium Chloride for Oral Solution USP, 20 mEq

Hyderabad, 28 January 2022: Granules India Limited announced today that the US Food & Drug Administration (US FDA) has approved the Abbreviated New Drug Application (ANDA) filed by Granules Pharmaceuticals, Inc. (GPI), a wholly-owned foreign subsidiary of Granules India Limited, for Potassium Chloride for Oral Solution USP, 20 mEq. Potassium chloride is used to prevent or to treat low blood levels of potassium (hypokalemia). It is bioequivalent to the reference listed drug product, Potassium Chloride for Oral Solution, 20 mEq, of Pharma Research Software Solution, LLC. The product would be available for the US market shortly.

Commenting on the approval Ms. Priyanka Chigurupati, Executive Director, GPI, said “We are pleased to receive the approval of the product and will surely be a valuable addition to our growing product portfolio in the US market.”

Granules now have a total of 49 ANDA approvals from US FDA (47 Final approvals and 2 tentative approvals).The current annual U.S. market for Potassium Chloride for Oral Solution USP, 20 mEq is approximately $44 million, according to MAT Nov 2021, IQVIA/IMS Health.

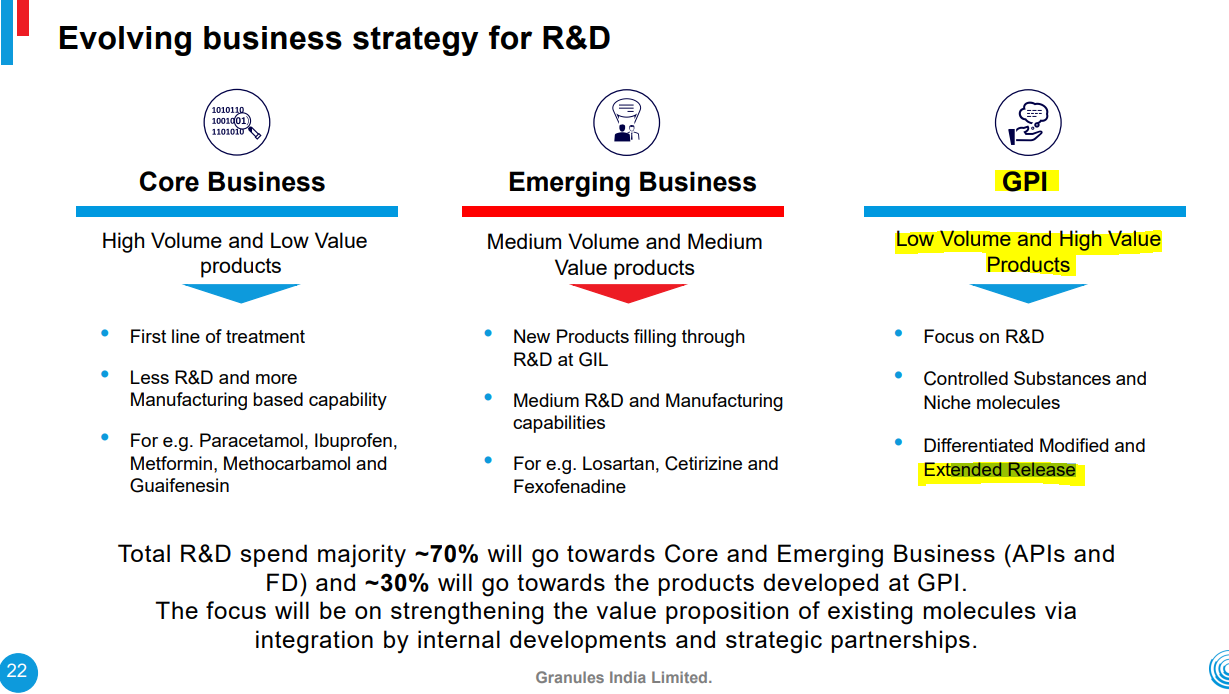

Granules 2.0

- Thinking of sustainability in all things we do.

- Use raw material available in India and backward integration, reducing China dependencies.

- Focus on R&D,

○ Borden our offering. This will result in a higher number of filing

○ Most of the activities focus on non-core molecules.

○ Avg run rate is around 40 cr. YTD 109 cr. Fy22 around 140 cr.

- Outlook is brighter than ever before. We will share a key roadmap of our transformation.

Other:

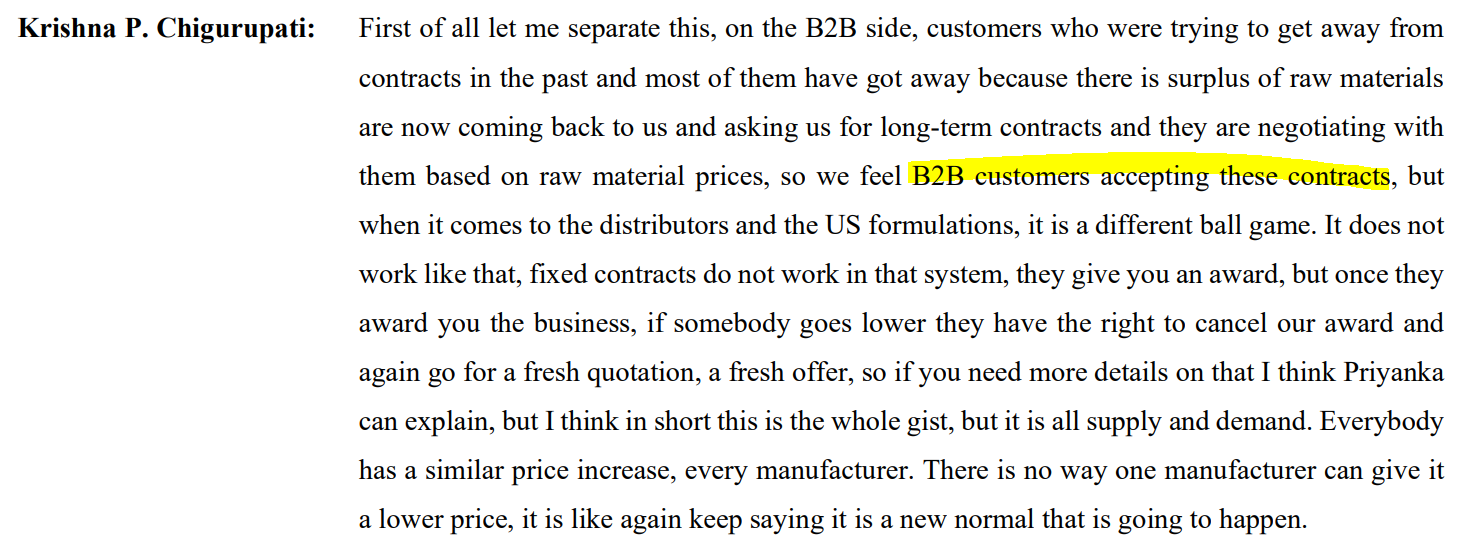

- Able to pass to significant price hike starting this quarter.

- Debt increased due to higher inventory for FD.

- FD percentage has gone down (profitable).

○ Rationalisation of inventory at customer end. Expecting improvements.

○ B2B not aware of inventory customers holds. Wait and see over a number of quarters.

- Prices of RM are still going on for paracetamol.

○ We were hoping that one Indian manufacturer will start. Indian manufacture has some quality issues. Chinese’s have not increased production. The good news is the Chinese’s manufacturers has started the plant, and it will take another three months before we start getting their products.

- I can see QOQ improvements but cannot quantify them.

- Ibuprofen API- Prices have come down, but volumes are down due to Covid.

○ Surplus capacity.

○ Some very cheaper alternative in US. Tough time for API manufacturers but we are well protected.

- Capex- 325. This year around 400cr.

- Assuming no fourth way or any- Things should normalise 2 quarts. (Para RM down, IBU sales up).

○ We shall strive to achieve 50% GM in a couple of quartres.

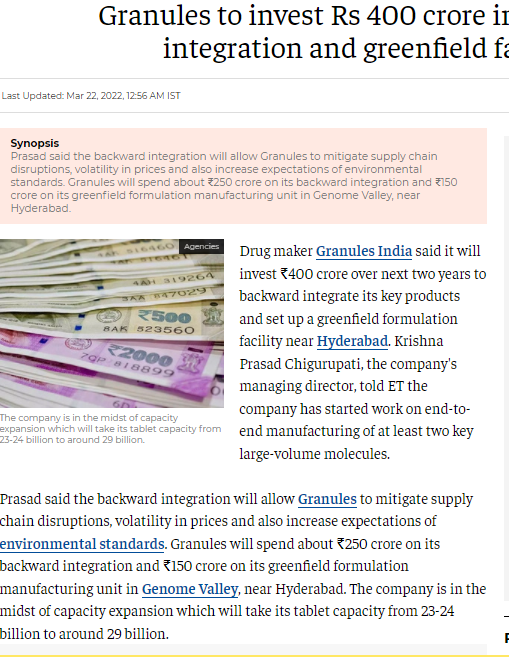

- Vizag. Spending 90 cr on HPI. This will be a focus on this area.

- Paracetamol - 50% of capacity utilisation.

5 Years roadmap

• Fully integration sustainable company and highest level compliance.

• Zero carbon neutral company.

• This shall give us a better sustainable margin.

MUPS Block

• All-most done. Doing qualification/validations at the moment

• Two products are approved. Will transfer to these blocks.

• Files 3 products already. Next year planning to 8/9 filing in next year.

• Towards the end of Q1, we shall start commercial production.

• Revenue contribution to start from Q2/Q3 .

• Basic Chemical to FD all the way.

Backward Integration

• For key products.

• Using new technologies and using RM India.

• This is for most of our existing products including PAP, Ibu

• It will take around 2 years to reflect.

• We will have a near-zero dependence on China.

Thanks for capturing the points nicely. Though the management says, it will be able to pass on some cost increase for the raw materials, there is a competition owing to commodity nature. Looks like, management wants to focus on FD owing to its better margin. I wonder where the capex spending will be leveraged on when Paracetamol Capacity util is only 50%

In 2017/18 when Oil prices rose sharply, Granules suffered increase in RM. They said they will pass on increased RM to clients with a lag effects of 6 to 9 and the infact passed it on. During that time FD contribution was much less and there was not much D2C (direct to consumer sales) which are around 40% of their sales Fy21.

In Q3, they have completed one of the major capex plan for MUPS block, which they have been doing for last few years. I guess they spent around 350-400cr on that. This capex is not earning any revenue and the contribution of it so far (and next 3/4 quarters) will be depreciation. So once it becomes operational, then we shall see real benefit in term of profitability.

So in 3-4 quarters shall be much better placed to face the situation and improved profitability IMO.