Not a complete answer but points from concall supporting these are

New products with higher margins will help lift the margin.

The cash conversion cycle were around 117 days & this high number(although its around 5yr average) was due to inventory buildup since they anticipated Covid related disruption & to shield themselves against these inventory were buildup.

This buildup inventory will sheath the companies raw material cost from the market cost.

They have been conservative of past prediction & this time too they are conservative, so I expect something around 22-25% bottom line growth if not less

I also thought New product with higher margins should lift the margin but management when I asked about FY23 margin (after raw material situation is improved), they still guided for 22% to 25% margin which is surprising. They did 26% margin in FY21 and with 20% cagr revenue growth, one would expect economics of scale/value added products, margin increasing beyond current level. They always overpromised in the past. May be they are under promising now and will over deliver in future… Let’s hope so

Just watched management interview on CNBC… dramatic change in the EBITA guidelines…

He said in yesterday’s conference call, he guided for 20% and there was lot of confusion. Now, he has guided for 25% EBITA and mentioned that new launches should make up for paracetamol production loss.

This is what everyone was thinking but now I am thinking was this just an oversight issue? or??

I mean yesterday, many investors asked the same question around 20% EBITA guidance

How should one read this? For the first time yesterday, I saw management not comforting investors. They were not excited about the future

I would have been fine with 25% EBITA for FY22 but too late. I have reduced my holdings because I was holding for 3 years & it was very big weightage wise

The management is very cautious as the situation is very dynamic and changing for key Raw Materials, so trust them, they will pass through this phase smoothly.

We shouldn’t be too much worried as excel analysts to the last point margin details here there for every quarter.

They have announced confidently 1000 Cr capex now for the next leg of growth with internal accruals.

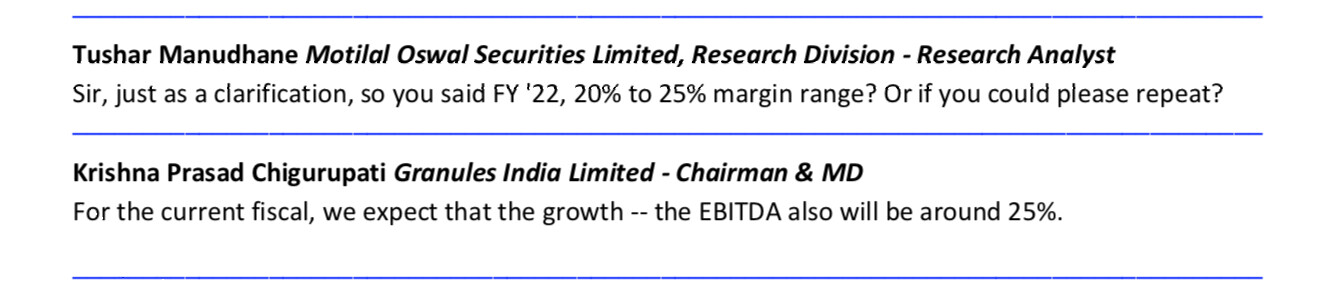

To clarify the confusion, Management do guide 20% EBIDTA for FY22 in concall. But on TV interview with CNBCTV18, they clarified the they incorrectly mentioned it as 20% and so only confusion happened and stated 25% is correct number. They updated these 20% in concall transcripts to 25% also

They corrected the EBITA numbers in concall transcripts. But I agree with your view. I was trying to understand how could margin drop to 20% with new product launches. I think story is still intact for next 3 to 5 years. With new PAP capacity coming up, the problem of sourcing raw material more or less should be fixed. Of course, challenging next 2 quarters. Valuation wise stock is still cheap. With good ROCE, consistent quarterly growth, and some free cash flow in FY23 and thereafter good chance of stock re-rating but seems we are not there yet.

A completely hands on MD does not make such errors in a con call. This is most likely an after thought and an attempt at damage control. In the past, Granules used to take around ten days to put up the transcript. In fact, in 1918 I had asked the then Investor Manager, why he takes so much time for such simple work and he gave a sob story about over work and time taken for approvals by management. This time it is a big surprise.

I think companies should stop giving so called “guidance”. What is its real purpose here? Is it to make analysts’ work easier? Setting expectation and managing share price? Let company management focus on growing their business profitably and let analysts figure out on their own where the company is headed in the long term.

As soon as results are announced, there is talk of “in-line”, “beat”, “miss”, “commentary”, “tone” etc, with consequent rise and fall of share price. Of course, some will look to benefit from volatility. But the obsession with quarterly numbers is counter productive for investors in general. Just ask the veterans!

Some research reports are just out in public domain. Management guided for 18-22% PAT growth for FY22 but 2 brokerage houses have pencilled in 2-3% PAT growth only.

Secondly in general, the pre-result expectations flashed in media are way different from the brokerage reports numbers published periodically. Plus some sections of the media claim ‘beat’ while some claim ‘miss’ based on consensus estimates or if it is paid news.

An investor needs to be able to individually decide on an investment if he aims to be successful.

Management guidance helps and in Granules case they’ve walked the talk atleast in the last 3 years.

There were mentions about the set up of 3 mega Bulk Drug Parks in India by GOI in 2020 AR. Does anyone know if any progress has happened on this?

The latest reports I can find are these

Granules bought 7 ANDA last quarters. I did not hear much discussion around it in the Q4 con call. Hence I asked few questions to the investor relation team, and I received the following answer:

1- How much amounts are spent on these acquisitions? (Ans- $ 1million)

2- What is the benefit of buying instead of filing for these ANDA? (Ans- We need not waste our R&D resources.)

3- Are these ANDAs approved? (Ans- This is strategic will not be in a position to give out)

I read somewhere (I could not find a source) one ANDA application will cost in between $0.5 -$1 million. Considering Granules paid $1 million to acquire all ANDA, they have got them at a good price. I think they might have bought it from other API manufacturers, which might not be as backwards integrated as Granules is.

Point3- Although the investor relation person chooses not to answer it, Granules have said in Q4 con call that they plan to launch it in the next couple of quarters. This suggests to me that these ANDA are approved, and once Granules complete tech transfer, they are ready to launch it.

Among several products that Granules India manufactures, how many of them are patented by Granules itself?

Also , what are the future growth rates of the markets of those products - both domestic and internationally ?

No patents. They only manufacture generics which anyone can manufacture and their edge is on how sustainably they procure raw materials, maintain quality and keep their costs low

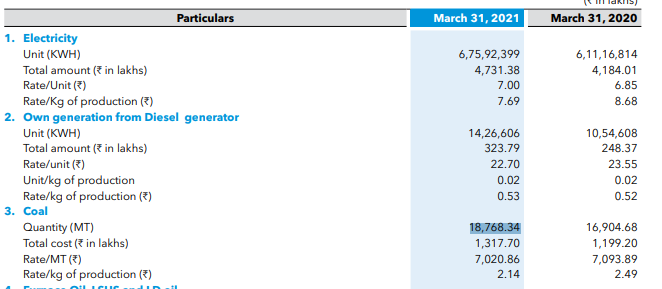

When going through AR-FY21, I found granules consuming 18,768.34 Metric Ton of coal in this year. Anyone knows why they need coal? and why they need huge amount?