The increase in raw material price of PAP will have significant negative impact on the margins of the company in the short term mainly due to fixed price contracts.

This is admitted by the Promoter in the above interview with cnbc.

Anyone has a exact data on how much fixed price contracts are and in terms of % what will be the impact.

3 Likes

not correct. She said they can pass on the increased prices to most of the strategic customers but there is a limit

4 Likes

Please listen exactly at 5.51 min of the video where she confirmed that there are blip for next couple of months.

This means it is better to wait for some time and look at the counter after the prices stabilise

1 Like

This is correct. I was referring “fixed price contract” sentence. Even though she said they would meet the guidance, some blips in the next one or 2 quarters

2 Likes

Any kind of shortages or disruptions usually end up benefitting large companies, although they make noises to the contrary. In fact when Trump put the dreaded USFDA on leash and pushed them to expedite clearances of long pending ANDAs, the resultant increased competition eroded profit margins and the entire pharma sector went down for three years. It is the covid disruption, which has put the life back.

5 Likes

we have lost around 20% since this post. There can be debates around different opinions but market has its own way of responding to developments. In this case, when management came up with an excuse just before Q3 numbers, markets gave a thumb down to such indicator.

Management went ahead with similar indication once again appearing on business channel & flashing another excuse for most probably inferior Q4 numbers.

As a shareholder, I am not interested in listening transportation issues / price hike of ingredients affecting the turnover / margins rather I am interested in efficient management of such issues so that business remains robust and continues to grow rewarding various stakeholders.

Once again I keep fingers crossed in hope that management develops a module where business grows as per plans delivers projected trajectory.

4 Likes

Yes I completely agree.

Few years back there were rumours that no succession plans.

Still it is difficult for the new generation to compete with its peers.

I good decision for the shareholders and long term investors would have been PE faints like Carlyle taking some stake.

But this is completely ruled out by management.

Hence the broader market has not shown interest in the stock.

This is my personal view after track it this company for more than 3 years.

Disc. Not invested.

2 Likes

I did post detailed SHP analysis after an hour of work and a gentleman failed to understand & chose to flag it as SPAM. Our moderators may be flooded with such requests …chose to remove it without having a look on the matter posted.

If details posted by me doesn’t add value … I will stop posting them here… Thanks all

but the post gets multiple likes before some gentleman exercises his wisdom to flag as spam

16 Likes

5Y Performance:

1Year Performance

6 Month Performance

Based on logic going on in thread above

5Y Performance: Granules => Good Management

1Year Performance Granules => Very Good Management

6 Month Performance Granules => Very Bad Management

I don’t think we draw conclusions on management based on just on one two Qtr.

We draw it based on

I would like RoE to be more but it predominantly manufacturing company and largest in it’s areas with no FDA / Quality issues, consistent delivery for 10 years.

Disclosure: Invested for more than 5 years enjoying CAGR of 22%+ .

11 Likes

Consensus EPS estimates for Granules has been moving up for FY22 and now stands at 24.8. On average granules has traded at 16x PER (range is 10-24x). So based on this the stock should be trading at 24.8 x 16 =400

Source:GIA Stocks

5 Likes

Results are out…

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=a9bb7fc7-8188-4d11-abfe-370e6b46b57f

Year end EPS of 22.05 compared to previous years 13.19.

1 Like

Qoq drop was due to Key Starting Material (KSM) shortages…situation expected to improve from Q2FY22.

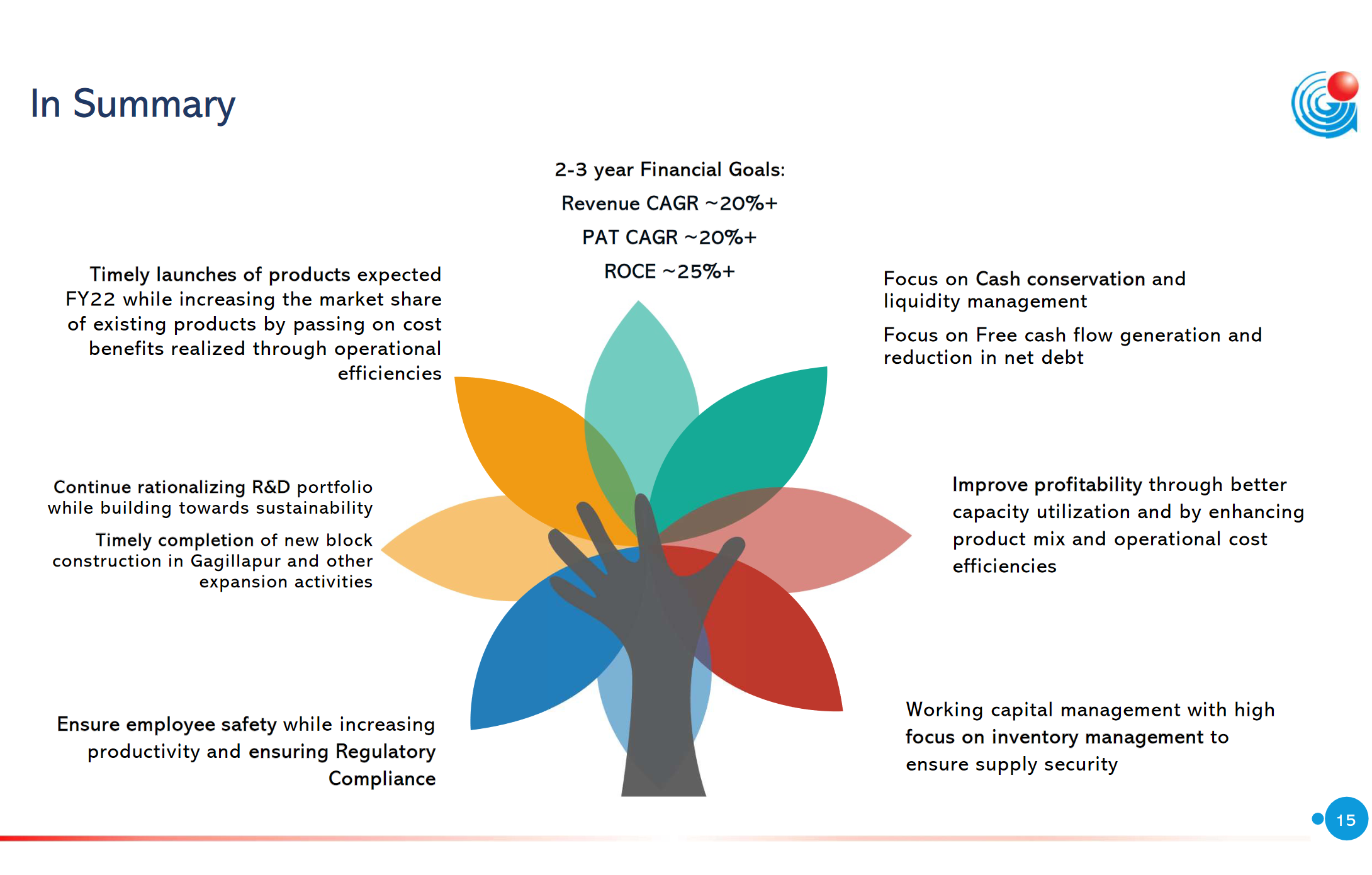

Guidance of 20% Revenues and Profit growth over next 2-3 years with 25% roce.

2 Likes

Could not find the guidance part any where in presentation. Can you please point towards the direction or paste a screenshot?

Cost of material consumed is at 48% in this quarter which is same as previous QTR. I was expecting increase in raw material cost as indicated by management last time.

Recently Para Ameno phenol prices have gone up significantly. Need to check how it will impact Q1 and thereafter.

But overall very good performance in FY21. ROCE > 25%… Free cash flow +ve but impacted because of increase in inventory (as per management last time this is being done to launch new product)

Look forward to conference call

3 Likes

Earning Presentation

1 Like

Good numbers yoy. Dividend was a positive surprise, guidance remains positive and not too ambitious.

I’m surprised to hear from some market guys that they were expecting topline of 900-930 Cr and bottom line of 140-145 cr. The result is a clear beat vs the broker reports issued after Dec quarter on their FY21 estimates.

Subject to concall, the results re-iterate that the stock deserves to be priced much higher.

1 Like

Conference call summary…

• Para Amino Phenol prices (Key starting raw material) have increased 250% because of factory shutdown of one of the major supplier in China. Prices of Acetic Anhydride also increased 50%

• China Supplier is planning to shift facility to a new place. Expect restarting of operations by Q3

• Lot of PAP capacities coming in India but it will take some time (at least next 2 quarters) for raw material prices to stabilize

• FY21 EBITA 26%. EBITA guidance of 20% in FY22 was bit shocker because of PAP shortage situation. However, management has guided for 20% net profit increase in FY22.

• Lot of question around this guidance as with 20% EBITA, revenue will need to be around 5000 CR (from 3268 CR in FY21) to meet the 20% net profit guidance

• Management couldn’t clarify the calculation and requested to take this offline.

• Challenging next 2 quarters and situation should improve from Q3.

• FY23 EBITA guidance 23% to 25%

• Tone was down. May be because of Covid situation around. Their CFO couldn’t attend the

call as he is suffering from Covid

12 Likes

Even with 20% PAT/ EPS growth with 20%+ RoE/ ROCE, the stock deserves to trade north of 400.

The minimum EPS for fy22 should be 25-26 atleast as base case. A lower-side PE of 16 translates to a price of 400.

Not to mention that stock price move is driven by sentiments

1 Like

But how 20% eps growth is possible with 20% ebita in FY22?