Ramesh Shiva, after spending 20 years of his professional career in the hotel and related industries, ventured into entrepreneurship with his wife Vidya Ramesh in late 2011, establishing Grand Continent Hotels in India with an initial unit of 54 keys he was Management Trainee at the Oberoi Hotels group to the CEO position at Sabari Hotels, a regional chain of hotels in South India he is also a Graduate from Institute of Hotel Management, Chennai in 1993

GCH employes asset light model, leasing properties for 10 to 15 years and operates through franchising partnerships with renowned Indian brands like Royal Orchid Hotels (Regenta) and Sarovar Hotels (Golden Tulip), where franchisors are responsible for sales and marketing

Started 1st hotel unit under the GCH brand and subsequently transitioned to a franchise model, utilizing established hotel brand names for marketing and sales

In the Franchisee Model, the company selectively expands by partnering with franchisees when favorable deals arise, allowing for growth without the heavy capital expenditure of owning each property. Leasing properties long-term reduces capital requirements, while the company retains the right to exit leases, minimizing risks. Franchisees benefit from the franchisor’s established marketing channels, sales support, and national brand recognition, helping them reduce advertising costs and attract a wider customer base. The franchisor also provides operational support and a proven business model, which lowers risks and improves success rates for franchisees. An example of this model is Royal Orchid Hotels, which operates over 100 properties across 70+ locations in India, offering premium stays and catering to midscale travelers through its Regenta Inn brand.

In the Own Model, the company directly owns and operates its hotels, giving it full control over branding, operations, and guest experience. This model requires significant capital investment in acquiring and developing properties but offers long-term ownership benefits. The company keeps all revenue generated from the hotels, which can result in higher profitability. An example of this model is Sarovar Hotels and Resorts, which operates 120+ properties across 75 locations, offering upscale stays under the Golden Tulip brand and midscale options under Tulip Inn. This model enables the company to maintain strong brand identity and consistency across its properties.

State it operates in: Karnataka, Tamil Nadu, Goa, AP, Telengana

It operates under asset light model where it takes the lease from Hotel/Assset owner for 15 years and runs the same

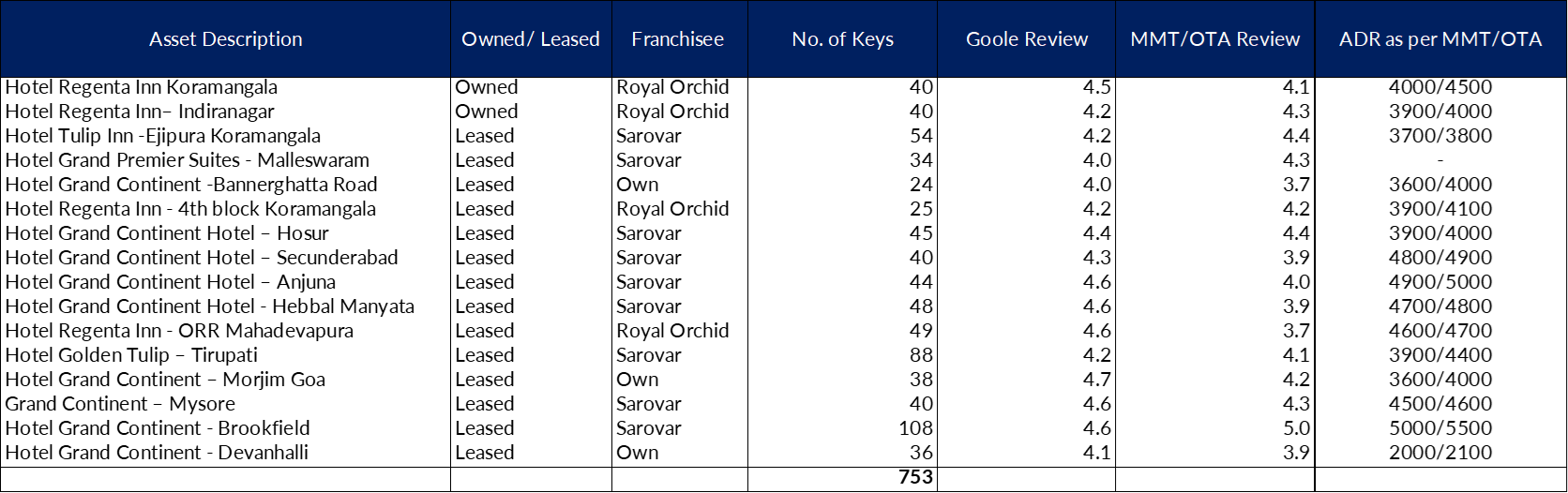

Grand Continent Hotel (GCH) is a Bangalore-based company that was founded in 2011, specializes in managing and operating 3-star hotels in prime locations. The Company started by solely operating and managing flags owned by Sarovar Hotels/Louvre (Tulip Inn) and Royal Orchid (Regenta Inn) – these brands market their own inventory respectively. Pays marketing fees to sarovar hotels at 3.5- 4% of top-line. Gradually, it started implementing its own brand Grand Continent Hotels wherein the entire inventory will be under the GCH brand and will be marketed by GCH itself. It primarily operates on an asset-light model i.e., either the asset is leased for long term (15 years) or built by a JV partner and the entire operation and management is undertaken by GCH. As of September 2024, they had ~753 keys and expect to increase to ~1500 keys by FY6. Any future additions would be made through lease arrangement model.

'The faster turnaround allows GCH to capitalize on peak demand cycles ahead of competitors, ensuring higher occupancy and revenue growth.GCH operates multiple hotels across Bangalore’s prime commercial and IT corridors, including Koramangala, Indiranagar, Bannerghatta Road, Hebbal Manyata, Brookfield, and Devnahalli, ensuring access to business hubs, tech parks, and corporate offices

Now the company has slowly and steadily started to go and penetrate their own brand name under the name Grand Continental hotels

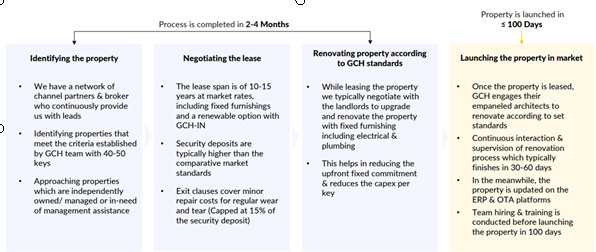

The company follows asset light approach for opening the hotels: The Asset Light Model allows for rapid property deployment, with hotels operational within 3 to 6 months post Letter of Intent, which is faster than the Ownership Asset Model. In this structure, landowners manage the construction of fixed assets, while GCH handles movable assets such as mattresses, linens, and minibars. This approach enables GCH to expand quickly while maintaining a high-quality guest experience without heavy capital investment. The model involves lower capital expenditure per room (₹6-6.5 lakhs) and a quick payback period of less than 24 months, resulting in higher Return on Capital Employed (ROCE). Since GCH does not own the real estate, fluctuations in property values do not affect profitability. Additionally, exiting properties is simpler and more cost-effective, with an exit clause that covers minor repair costs, capped at 15% of the security deposit. The company aims to scale up to 5000+ keys within the next five years, reinforcing its presence across multiple high-demand locations

From the DRHP: We plan to continue focusing on our core strength of developing upper-midscale and midscale hospitality assets and to

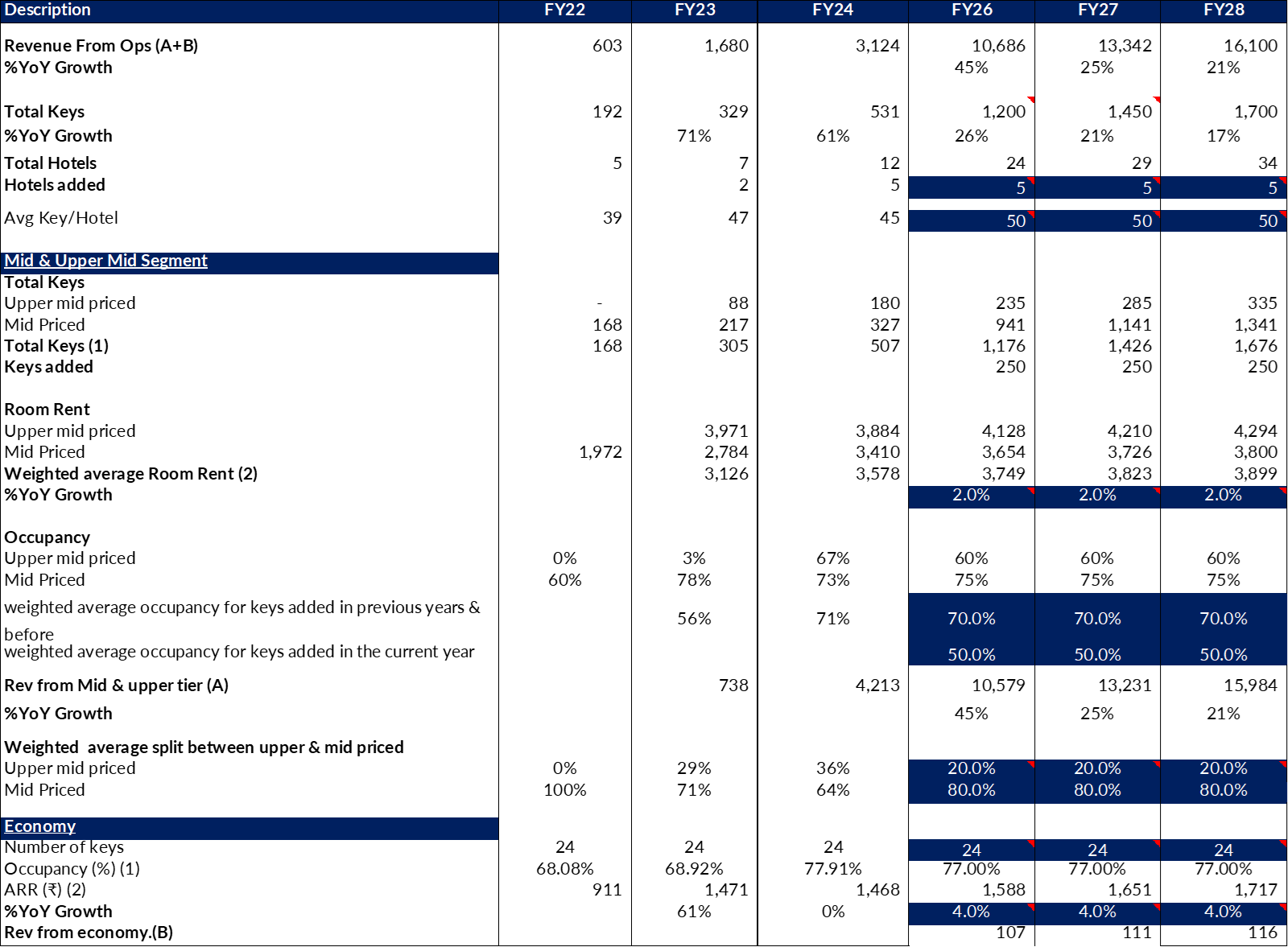

increase the number of keys across our hospitality assets by an estimated 1,500 keys, from 753 keys as at September 30, 2024

to approximately 2000+ keys in FY2026

Over the past 13 years, expertise in managing and operating hotels has been developed. As of September 30, 2024, a portfolio of 16 operational hotels with 753 rooms has been established. Additionally, one hotel was mobilized in October 2024, and another is set to open by November 2024, bringing the total to 18 hotels and approximately 850 rooms. MOUs/LOIs have been signed for 5 more properties in the upper mid-priced and mid-priced categories, adding around 346 rooms to the portfolio.

Identification to starting of the Asset:

Valuations Assumptions:

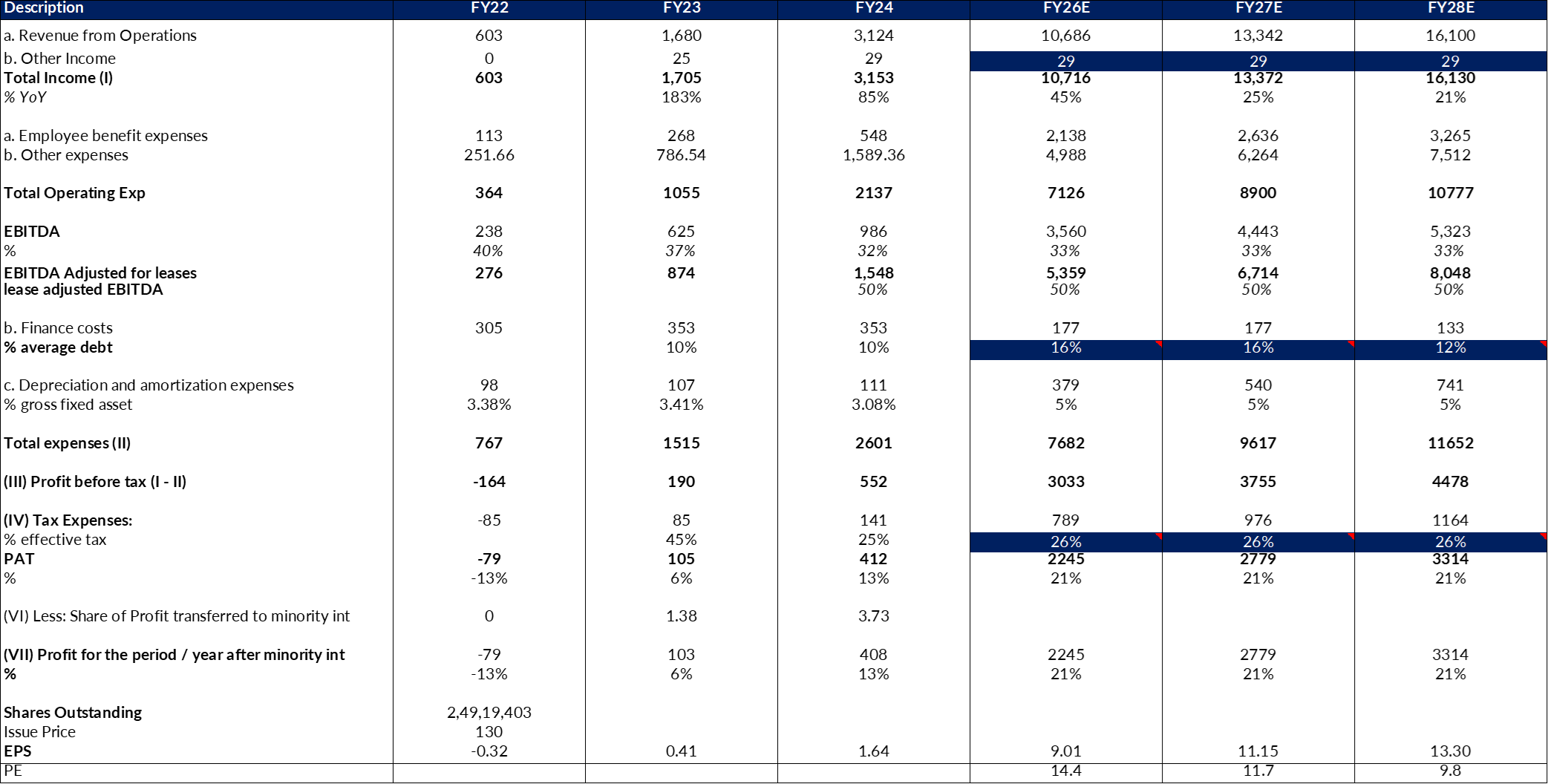

Profit and Loss Statement Assumption:

At current valautions the company is trading at 14x FY28 Which is on tad higher side, How ever the EV/EBITDA Trades at on SD -1 To it’s peers offering a good valuation comfort

One thing that was very attracted me here is Quality of hotels and Location and how much the promoter and team puts thought into the same

Have Stayed in the hotels in Banglore and the vicinity of their Whole PF in Banglore is one of the finest for corporate employees

Only Risk that I see here:

-

The entity is going internationally to expand their operation I’m highly usnure of the reason for the same since the company is already doing well in India and has good pipeline in India why will be a very good question?

-

The company has been expanding pretty aggresively in terms of its room inventories Generally have seen the value is created immesily here but there will also be sort of Pre-Opex of the hotels which multiple people seems to ignore I think that might not lead to Linear Results QoQ basis but that’s the fun of Venture type bets in listed companies :)

-

I don’t have any doubt on the execution of Ramesh Shiva Since they way he has scaled up in last 3-4 years is commedable but the same was on back of the depressed lease market the Rentals were depressed so we don’t know at what margins are the new leases getting entered so the margins might not coninute going ahead at this high level, Something to look out for too

Disclaimer: Holding Signifcant of the company from near the IPO price, No buy or sell recomendation, sharing Just for informational purposes