Hi all, this is my first post, so please excuse my errors. Would love to hear your feedback. For this post I have tried to arrange management commentary in a coherent manner. Most of the points have been sourced directly form Concall transripts, AR etc.

## Short Note:

- GPT Infra is a railway focused infrastructure company, with core capabilities in EPC [mainly varied type of railway bridges] and Sleepers [the slabs used between tracks]. Railways present a large market size opportunity driven by Indian Government’s MASSIVE capex plan for Indian Railways ().

- Operates in two primary segments – Infrastructure [EPC], which is a construction contracts forgovernment agencies, primarily railways, wherein we build bridges and ROBs and coreinfrastructure for railways primarily, also some PWDs and government agencies like MoRTH andothers. That is about 75% of our topline, 25% of the topline comes from manufacture of railway concrete sleepers.

## Other interesting points as per mamangement

1. Healthy order book

* Has an estimated order book of ~1850 cr with an avg execution of 24-30 months as of Mar 2017

* Targets to add 1500Cr orders in FY18 [rough est of booked ~500cr by June 2017]

* Order book estimated to be 2200 Cr; Year end projected at 2600cr [Opening 1850 - FY18 execution of 725cr + 1500 est new order wins]

2. Stable to improving margin

- In India both the businesses [Infrastructure ~80% of order book and India Sleepers business 16% or order book] are almost at the same level; India is about 13%-13.5%. Internationally [African sleeper business], the African businesses [~4% of order book] are between 25% to 30%, at EBITDA level.

- All our contracts, whether it is concrete sleepers or whether it is EPC construction, have a price variation formula. So it does not get affected by the increase or the decrease in the cement andthe steel prices as such because there might be (+/-1) month lag but it does not get effected interms of the margins. In terms of achieving a margin target for the year of 15%, I think it isquite achievable because as we grow the business in terms of volume the overhead do not goproportionately. We should be able to achieve or we have an internal target to do a margin, sofar in the north of 15%. I think 15% is the target we should be able to achieve for the year.

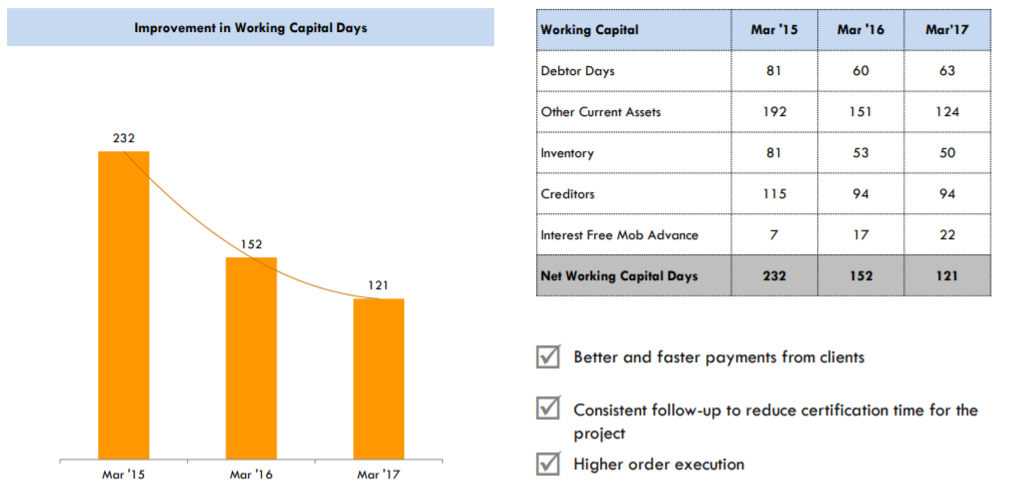

3. Improving working capital cycle

- Working capital cycle from 232 days as on 31st March, 2015, 152 days as on 31stMarch 2016 to 121 days as on31st March 2017 following a quicker payments inflow.

- These contracts have been accompanied by better payment terms, marked bymobilization advances and shorterreceivable cycles.

4. No major capex required

- Most of the major CAPEX for the two factories of almost

25 crore has already been incurred,the balance would be incremental CAPEX to fund some of the newer contracts which wouldnot be anything major, it would be almost10 crore to `12 crore a year maybe, nothing major.

5. No Major change in debt expected

- We would like to maintainhealthy debt to equity ratio so we don’t want to over leverage ourselves too much as we aregrowing the business 30%-35% every year.

-

200 crore is the short-term debt and10-12 crore is the long-term debt. We expect the debtto move up may be by 5% to 10%, we don’t expect the debt to move up too much because a lotof the cash flow which was stuck in terms of the working capital cycle is getting freed up sothat will enable us to grow the business further.

6. Low competitive intensity

- The competitive scenario is there obviously. I would not say that there is no competition interms of the railway orders, but the we are bidding in terms of the bridges, especially between

100 to200 crore, there the competition is not too intense so we see may be 3 to 4 bids generally not more than that and in terms of the margins we have a hurdle rate of 14% [13.5% mentioned later] so we don’t bid for contracts below that. I think we have been able to achieve our numbers historically also. There are lots of opportunities in the market and I think that we will be able to maintain our margins at 14%.

7. Potential to bid for 1000cr projects FY20 onwards

- …average ticket size of our orders have improved from 40cr a few years ago to more than 100cr today, translating into project economiesand increased profitability.

- It would be pertinent to communicate that during the course of the yearunder review, the Company received its largest ever construction order of 217cr in its name. This project comprises construction of bridges on the Mathura-Jhansi third line for Rail Vikas NigamLimited and is to be completed within 36 months. On completion of thisproject, the company will be able to bidfor projects in the range of H1,000 crin its independent capacity from 2020onwards.

- Strengthening the business: I am pleased to report that the companystrengthened its business beyond whatmay be evident in the financials of2016-17.Even as the company’s revenues mayhave only been marginally higher thanin the previous year, the direction ofthe company continues to be positive.Besides, the projects are larger, themargins hurdle rate higher and eachof these projects, when complete, willmake it possible for the company toaddress even larger projects.

8. Management does not see any major execution risk

- Ashish Shah: So, the problem then remains in which project now? Would I be right in saying that the entire orderbook now is executable? There is no project which is stuck or non-moving or anything like that?Atul Tantia: Sir, there is no project that will be stuck. The only hindrance was the Manipur, which has beenresolved by March before the new elections happen

##The BIG opportunity in Railways

-

Indian Railway has embarked upon a massive 8.56 trillion, with the CAPEX plan for 2015 to 2019, which is 90% more than in the combined CAPEX done in the previous 15 years. The budget 2017 has allocated

1.31 trillion to Indian Railways in 2017-2018, the largest ever allocation increase of14,000 crore over the last fiscal year. There is a hugefocus on better safety through building in rail over bridges, ending unmanned crossing, etc. IndianRailways is targeting to eliminate all unmanned level crossings from broad-gauge lines by 2020 -

The estimated fund requirement for building ROBs and RUBs is

40,000 crore. Further, the fundrequirements for bridge rehabilitation is estimated to be over3,000 crore. Additionally, thegovernment has announced commissioning of the 3,500 km railway line in 2017-2018, up from2,800 km in 2016-2017. All of these are areas of large opportunity for us in terms of ourinfrastructure business. -

DFC is an additional growth area for us, both in terms of sleeper manufacturing as well as bridgeworks. Project award for DFC has been rapidly progressing over the last 12 months. Thegovernment has also announced to spend around `3.3 trillion to set up 3 new arms of the DFCcorridors. The 5,500 km long new corridor would supplement the existing plans to lay 3,300 kmtwo DFCs

##Quick/Rough Valuation

Disclosure:

- I have a very small investment, and plan to increase over time.

- I have used last 1-1.5 year call trancripts